In the landscape of personal finance, medical debt is an outlier. Unlike a car loan or a mortgage, which are planned financial commitments, medical expenses often arrive unannounced, the result of a sudden illness or an emergency room visit. However, despite the involuntary nature of the debt, the financial systems governing it are rigid.

When a medical bill goes unpaid, it triggers a cascade of events that can compromise your creditworthiness, drain your savings through legal actions, and impact your long-term wealth-building potential. Understanding the timeline and the mechanics of medical debt is essential for anyone looking to protect their financial health.

The Initial Cycle: From Due Date to Internal Collections

The moment a medical procedure is completed, the billing cycle begins. Most patients assume the process is automated between the provider and the insurance company, but this is where the first financial pitfalls occur. If a bill remains unpaid after the initial 30 to 90 days, the provider’s internal billing department moves into an “active collection” phase.

The Grace Period and the Risk of Billing Errors

Most hospitals and private practices offer a “grace period.” During the first 30 to 60 days, the debt is considered “current” but “outstanding.” This is the most critical window for personal finance management. It is during this time that you must verify the “Explanation of Benefits” (EOB) from your insurer against the provider’s itemized bill.

Statistically, a significant percentage of medical bills contain errors—ranging from duplicate charges to incorrect billing codes (upcoding). Ignoring a bill because it looks “wrong” is a common financial mistake. Unpaid errors turn into valid debts in the eyes of the law if they are not contested during this initial window.

Late Fees and Internal Interest Accrual

While many people believe medical debt is interest-free, this is a misconception that depends entirely on the provider’s policy and state law. Some large healthcare systems begin accruing late fees or internal interest once a bill passes the 90-day mark. While these fees might seem small individually, they compound the total debt-to-income ratio, making the eventual payoff more difficult and eating into your monthly discretionary income.

The Transition to Third-Party Debt Buyers

If the bill remains unpaid for 120 to 180 days, the healthcare provider typically “writes off” the debt as a loss and sells it to a third-party collection agency. From a business finance perspective, the hospital is recouping pennies on the dollar to clear their books. For you, the consumer, this marks a shift from dealing with a healthcare provider to dealing with a financial entity whose sole purpose is debt recovery.

The Credit Impact: How Medical Debt Erodes Your Score

For years, medical debt was the leading cause of bankruptcy in the United States and a primary reason for plummeting credit scores. However, recent changes in how credit bureaus handle medical data have provided some relief. Despite these changes, the impact of an unpaid medical bill remains a significant threat to your FICO score.

The 180-Day Credit Reporting Delay

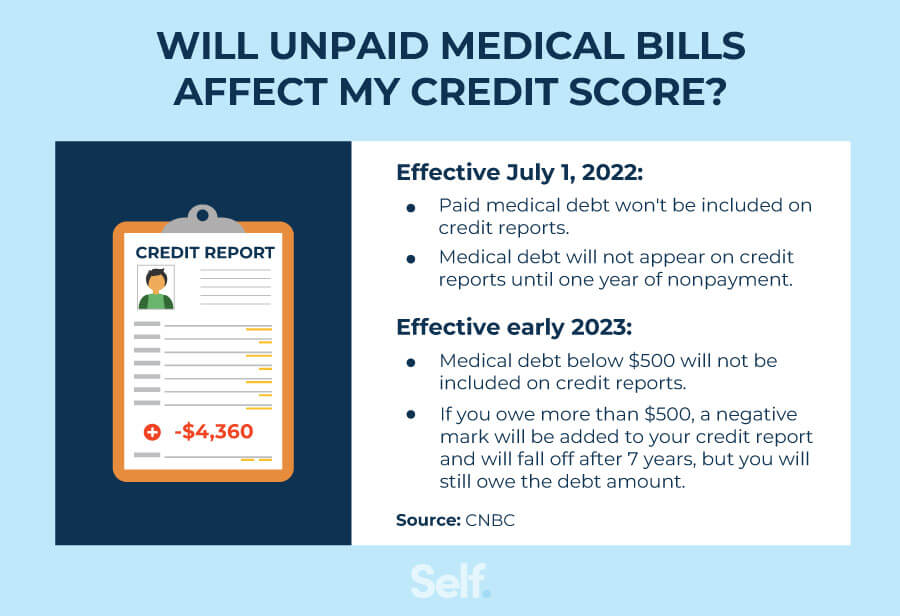

Under current consumer protection standards, the three major credit bureaus—Equifax, Experian, and TransUnion—must wait 180 days (six months) before an unpaid medical debt can appear on your credit report. This window is designed to allow time for insurance disputes to settle. Once that 180-day window closes, if the debt is over a certain threshold, it will appear as a “collection account,” which can cause a score to drop by 50 to 100 points overnight.

The $500 Rule and Paid Debt Removal

As of 2023, there have been landmark shifts in the “Money” sector regarding medical debt reporting. First, medical debts that have been paid in full are no longer allowed to remain on credit reports; they must be removed immediately. Second, the credit bureaus no longer report medical collection debt that is under $500.

While this is a win for those with small balances, it creates a false sense of security for those with significant surgical or emergency bills. If your debt is $501 or more, the full weight of the collection will hit your report, affecting your ability to secure low-interest rates on future loans, mortgages, or credit cards.

Impact on Future Borrowing Power

A credit report tarnished by medical collections signals “risk” to lenders. Even if your income is high, a collection account suggests a lack of financial management or an inability to handle unexpected costs. This can lead to higher APRs on auto loans or even the denial of a mortgage application. In the world of personal finance, the cost of an unpaid $2,000 medical bill is much higher than $2,000—it is the sum of the extra interest you will pay on every other loan for the next seven years.

The Legal Escalation: Lawsuits, Garnishments, and Liens

When a debt collector realizes that credit reporting isn’t enough to compel payment, they may turn to the legal system. This is where the consequences move from “digital marks on a report” to “physical loss of assets.”

The Summons and Default Judgments

If a collection agency owns your medical debt, they have the right to sue you in civil court. Many consumers ignore these court summons, assuming it is a bluff. This is a catastrophic financial error. Ignoring a summons leads to a “default judgment.” This means the court automatically rules in favor of the collector, granting them a variety of legal tools to extract the money from you.

Wage Garnishment and Bank Levies

With a judgment in hand, a collector can move to garnish your wages. Depending on state laws, a certain percentage of your take-home pay (often up to 25%) can be diverted directly from your employer to the creditor before you ever see your paycheck.

Alternatively, the creditor may secure a “bank levy,” which allows them to freeze your checking or savings accounts and seize the funds to satisfy the debt. This can leave you unable to pay for essential living expenses like rent or groceries, creating a secondary financial crisis.

Liens on Real Estate

In some jurisdictions, a judgment for medical debt can result in a lien being placed on your property. While the creditor might not force the sale of your home immediately, the lien ensures that when you do sell or refinance the property, the debt (plus accumulated interest and legal fees) is paid out of your equity first. This directly strips away your generational wealth and home equity.

Proactive Financial Strategies: Navigating the Debt

The best way to handle medical bills is to treat them as a negotiable business transaction rather than an unavoidable tax. There are several financial maneuvers you can use to prevent the escalations mentioned above.

Utilizing “Charity Care” and the 501(r) Provision

Non-profit hospitals are required by federal law (under the Affordable Care Act’s 501(r) provision) to have Financial Assistance Policies, often called “Charity Care.” If your income is below a certain threshold (often up to 200–400% of the Federal Poverty Level), you may qualify to have your entire bill wiped out or significantly reduced. This is a “Money” hack that many are unaware of; hospitals are not required to advertise it aggressively, but they must provide it if you ask.

Negotiating the “Self-Pay” Rate

If you do not qualify for Charity Care, your next move is to negotiate the “allowable amount.” Hospitals have different price lists: the high “sticker price,” the negotiated insurance rate, and the “self-pay” rate. If you are paying out of pocket, you can often negotiate the bill down to the “Medicare rate” or the “usual and customary” rate. Offering a lump-sum payment of 40% to 50% of the total bill is often accepted because it provides the hospital with immediate liquidity without the cost of collections.

Structured Payment Plans vs. Medical Credit Cards

Many providers offer interest-free payment plans. This is always a superior financial choice compared to putting a medical bill on a standard credit card or a specialized medical credit card (like CareCredit). Standard credit cards carry high APRs, and specialized medical cards often feature “deferred interest”—if you don’t pay the full balance within a promotional period, you are hit with backdated interest at rates exceeding 25%. Always opt for the provider’s internal payment plan first to keep your debt-to-income ratio manageable.

Conclusion: Protecting Your Financial Future

Unpaid medical bills are more than a nuisance; they are a threat to your financial autonomy. From the initial billing cycle to the potential for legal garnishment, the journey of an unpaid bill is designed to extract value from the consumer through pressure and penalty.

However, by understanding how credit bureaus report debt, recognizing the power of the legal system, and utilizing negotiation tactics like Charity Care, you can mitigate these risks. In the realm of personal finance, being proactive is the only way to ensure that a medical emergency today doesn’t become a financial catastrophe tomorrow. Treating medical debt with the same strategic rigor as an investment or a mortgage is the key to maintaining a healthy balance sheet and long-term financial security.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.