While many professionals spend their careers focused on the magic number of 65—the traditional gateway to retirement and Medicare—financial planning requires looking at the “what ifs” that occur before that milestone. A 401(k) is often an individual’s largest financial asset outside of their home. However, because it is a tax-advantaged account governed by federal law, the way it is handled upon your death is more complex than a standard savings account.

Understanding what happens to your 401(k) if you pass away prematurely is not just about morbid curiosity; it is a critical component of wealth preservation and ensuring your loved ones are provided for without unnecessary legal or tax burdens.

The Immediate Protocol: How Retirement Assets Are Handled Upon Death

When an account holder dies, a 401(k) does not simply vanish or automatically default to the state. Instead, it follows a specific legal hierarchy established by the Employee Retirement Income Security Act (ERISA) and the specific terms of the employer’s plan. Unlike assets held in a will, a 401(k) is a “contractual” asset, meaning it generally bypasses the probate process if a beneficiary is correctly named.

The Power of the Named Beneficiary

The single most important document regarding your 401(k) is your beneficiary designation form. This form carries more legal weight than a last will and testament. If your will says your 401(k) should go to your sibling, but your beneficiary form lists an ex-spouse, the financial institution is legally obligated to pay the ex-spouse.

Upon notification of death—usually via a death certificate—the plan administrator will freeze the account to prevent further trading or contributions. They then identify the named beneficiaries. These individuals are contacted and provided with the necessary paperwork to claim the assets. This process is designed to be efficient, but it relies entirely on the accuracy of the records you leave behind.

What Happens If No Beneficiary Is Listed?

If you die without naming a beneficiary, or if your named beneficiary predeceased you, the situation becomes significantly more complicated. Most plan documents have a “default” sequence. Usually, the assets go to a surviving spouse. If there is no spouse, the assets may be paid to your estate.

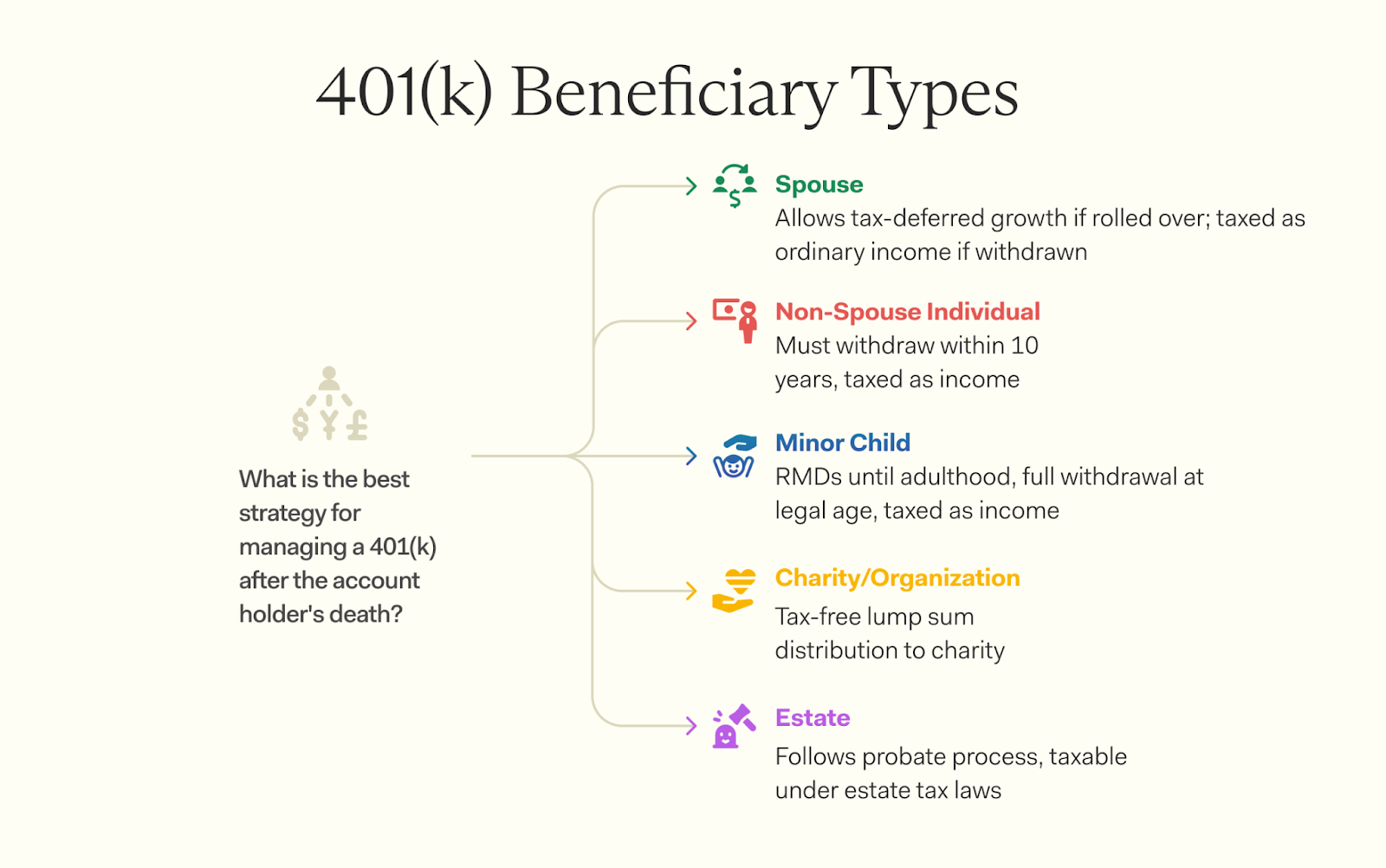

When assets flow into an estate rather than directly to a person, they must go through probate. Probate is a public, often lengthy, and sometimes expensive legal process where a court oversees the distribution of your assets. Furthermore, an estate cannot “own” a 401(k) in the same way a person can, often forcing a lump-sum distribution that triggers an immediate and heavy tax bill, significantly shrinking the legacy you intended to leave behind.

Distribution Rules for Different Types of Beneficiaries

The rules for how a beneficiary can access 401(k) funds changed dramatically with the passage of the SECURE Act in 2019 and the subsequent SECURE 2.0 Act. The options available to your heirs depend largely on their relationship to you.

Spousal Beneficiaries: The Most Flexible Options

Under federal law, if you are married, your spouse is automatically the primary beneficiary of your 401(k) unless they signed a written waiver. Spouses have the greatest amount of flexibility when inheriting these accounts.

A surviving spouse generally has three main choices:

- Spousal Rollover: They can roll the assets into their own existing IRA or 401(k). Once rolled over, the money is treated as if it were always theirs. They don’t have to take distributions until they reach their own Required Minimum Distribution (RMD) age.

- Inherited IRA: They can move the funds into an “Inherited IRA” (also known as a Beneficiary IRA). This allows them to take distributions based on their own life expectancy.

- Lump-Sum Distribution: They can take the entire balance in cash. While this provides immediate liquidity, it is usually the least efficient option because the entire amount is taxed as ordinary income in the year it is received.

Non-Spousal Beneficiaries: Navigating the 10-Year Rule

If you leave your 401(k) to a child, a sibling, or a friend, they fall under a stricter set of rules. For most non-spouse beneficiaries, the “Stretch IRA”—which allowed heirs to take small distributions over their entire lives—has been eliminated.

Most non-spouse beneficiaries are now subject to the 10-Year Rule. This means they must withdraw the entire balance of the inherited 401(k) by December 31 of the tenth year following the year of the original owner’s death. While they don’t necessarily have to take a specific amount each year (unless the original owner had already started RMDs), the total balance must be empty by the end of that decade. This can push beneficiaries into higher tax brackets if they inherit a large sum during their peak earning years.

The Impact of the SECURE Act and SECURE 2.0

The SECURE Act introduced a specific category called “Eligible Designated Beneficiaries” (EDBs). These individuals are exempt from the 10-year rule and can still “stretch” distributions. EDBs include:

- Surviving spouses.

- Minor children of the account holder (until they reach the age of majority, at which point the 10-year clock starts).

- Disabled or chronically ill individuals.

- Individuals not more than 10 years younger than the deceased.

Tax Implications and Financial Strategies for Inherited 401(k)s

It is a common misconception that inherited 401(k) money is “tax-free” like a life insurance payout. Because 401(k) contributions are typically made with pre-tax dollars, the IRS has yet to collect its share. When a beneficiary receives this money, it is generally treated as taxable income.

Understanding Ordinary Income Tax vs. Penalties

The good news is that the 10% early withdrawal penalty (which usually applies to those under age 59½) is waived for beneficiaries. If you die at age 45 and your beneficiary is 40, they can take the money without paying that specific penalty.

However, they must still pay ordinary income tax. If a beneficiary inherits a $500,000 401(k) and withdraws it all at once, they could easily see 30% to 40% of that total go to federal and state taxes. This is why financial advisors often recommend spreading withdrawals over the allowed 10-year window to minimize the annual tax hit.

The Importance of the Lump-Sum vs. Stretched Distribution

For a beneficiary who is struggling with debt or facing an emergency, a lump sum might seem attractive. However, from a wealth-building perspective, it is often the most damaging move. By keeping the money within an Inherited IRA (the typical vehicle for a 401(k) rollover), the assets can continue to grow tax-deferred. A beneficiary who manages an inherited 401(k) wisely can potentially turn a modest inheritance into a life-changing sum by allowing the remaining balance to compound over that 10-year period.

Proactive Steps: Securing Your Legacy Before the Unthinkable

Death before age 65 is an eventuality no one wants to plan for, but failing to do so leaves your family in a position of “financial triage.” Taking a few administrative steps today can prevent years of legal headaches for your heirs.

Regular Beneficiary Audits

The most common mistake in personal finance is “set it and forget it.” Many people name a beneficiary when they start a job in their 20s and never update it. Major life events—marriage, divorce, the birth of a child, or the death of a parent—should immediately trigger a review of your 401(k) beneficiaries.

Furthermore, you should always name contingent beneficiaries. If your primary beneficiary (e.g., your spouse) dies at the same time as you or shortly before, the contingent beneficiary ensures the money still avoids probate and goes exactly where you intended.

Integrating Your 401(k) into a Broader Estate Plan

For those with significant assets, simply naming a beneficiary might not be enough. You may want to consider whether a Trust should be named as the beneficiary of your 401(k). This is a complex strategy that requires a specialized attorney, but it can provide more control over how the money is spent (for example, ensuring a spendthrift child doesn’t blow the entire account in one year).

Finally, communication is vital. Ensure your loved ones know where your accounts are held and who the plan administrator is. In the digital age, many accounts are lost simply because the family didn’t know they existed. By aligning your 401(k) designations with your overall financial goals, you ensure that your hard-earned savings serve as a lasting support system for your family, regardless of when you pass away.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.