For many homeowners and prospective investors, the word “recession” triggers a specific visceral reaction: a mental image of the 2008 financial crisis. During that era, the housing market didn’t just stumble; it collapsed, leading to a global economic meltdown. However, as we look at the contemporary financial landscape, it is crucial to separate the trauma of the Great Recession from the historical reality of how real estate behaves during economic downturns.

Understanding the relationship between home prices and recessions is a cornerstone of sound personal finance and strategic investing. While a recession—defined broadly as two consecutive quarters of declining Gross Domestic Product (GDP)—signals a cooling economy, it does not inherently guarantee a fire sale on residential real property. In fact, history suggests that housing is often more resilient than the stock market during periods of contraction.

Historical Perspectives: Why Every Recession is Unique

To understand what might happen to home prices in a future recession, we must first look at the track record of past economic cycles. The correlation between a shrinking economy and falling home prices is not as direct as one might assume.

The 2008 Anomaly

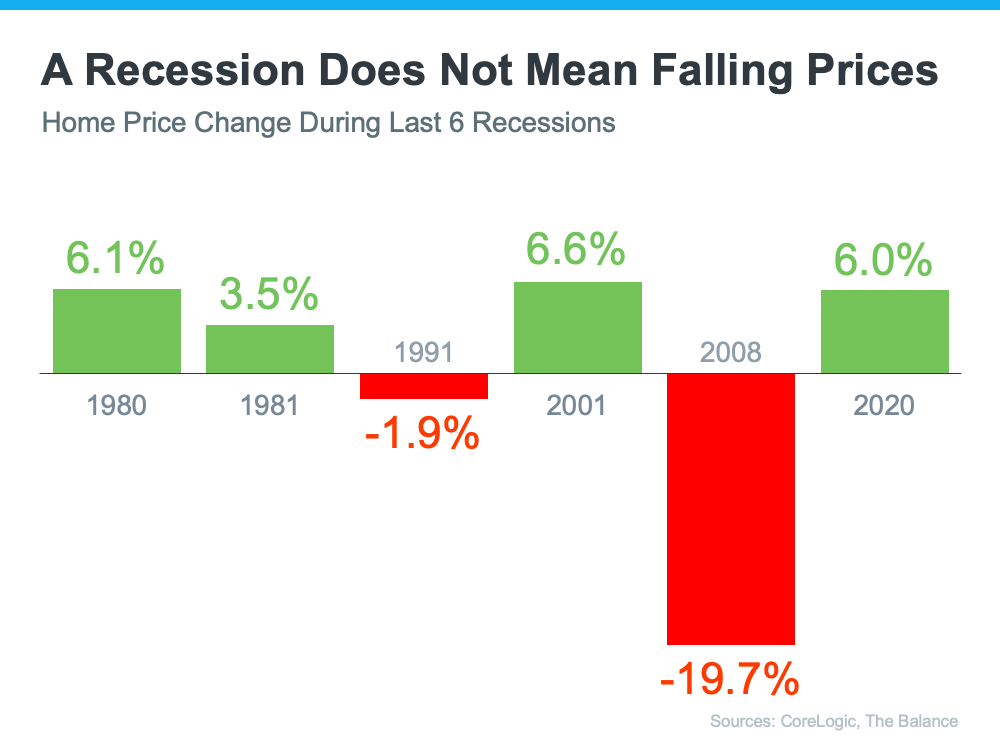

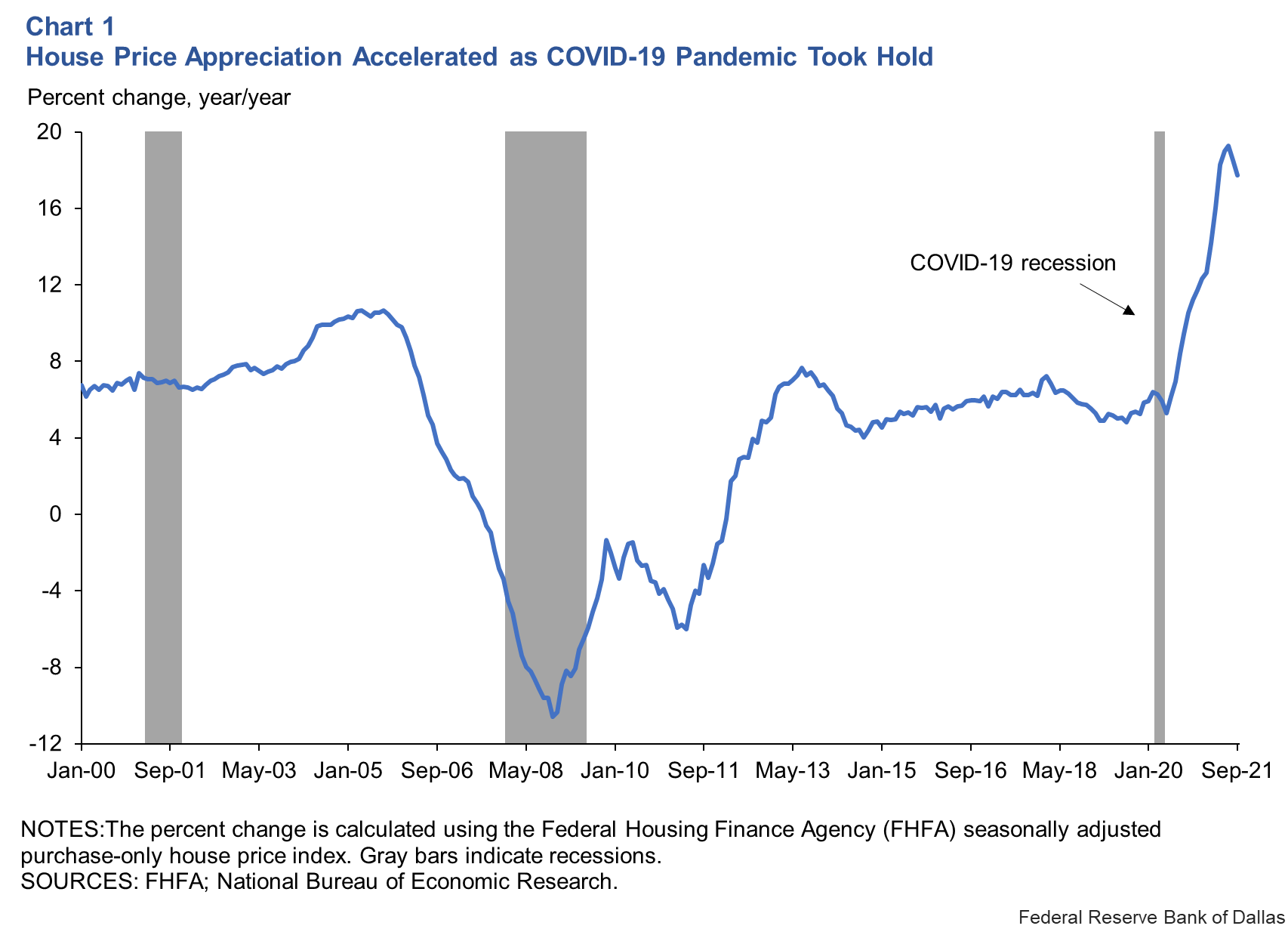

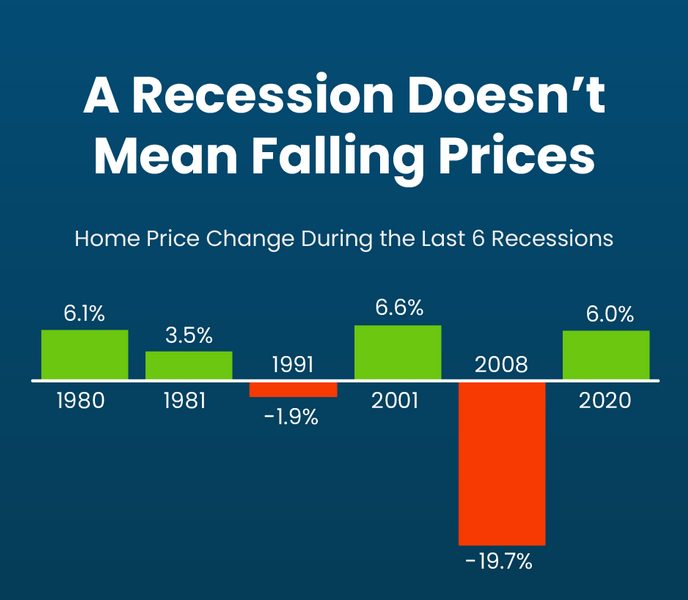

The Great Recession of 2008 is the primary reason the public associates recessions with falling home prices. During this period, home values in the United States plummeted by nearly 33% on average. However, the 2008 crisis was unique because it was caused by the housing market. Subprime lending, predatory mortgage practices, and an oversupply of inventory created a bubble that was destined to burst. In this specific case, the housing market was the engine of the recession, not a victim of it.

Previous Recessions and Price Resilience

If we look at the four recessions prior to 2008, a different pattern emerges. In the recessions of 1980, 1981, 1991, and 2001, home prices actually remained stable or continued to appreciate. For example, during the “Dot-com” crash of 2001, while the NASDAQ was losing a significant portion of its value, home prices in the U.S. grew by roughly 6.6%. This highlights a critical lesson in personal finance: real estate is often viewed as a “safe haven” asset when the equity markets become too volatile.

The Pandemic Contraction

The brief but sharp recession of 2020 caused by the COVID-19 pandemic provided another counter-intuitive example. Instead of prices dropping due to economic uncertainty, they skyrocketed. This was driven by a combination of record-low interest rates, a shift toward remote work, and a chronic undersupply of homes. This underscores the fact that housing prices are driven more by the laws of supply and demand than by the general state of the GDP.

The Role of Interest Rates and the Federal Reserve

In the world of business finance, the Federal Reserve is the primary architect of the economic environment. Their influence on interest rates is perhaps the most significant factor in determining home price movement during a recession.

The Stimulus Effect

Typically, when a recession begins, the Federal Reserve lowers the federal funds rate to stimulate economic activity. This downward pressure on rates usually trickles down to mortgage lenders. When mortgage rates drop, the cost of borrowing decreases, which increases the purchasing power of buyers. For instance, a buyer might be able to afford a $500,000 home at a 3% interest rate, but only a $400,000 home at a 6% rate. This increased affordability often keeps demand high enough to prevent home prices from cratering.

Inflation and Real Assets

During periods of economic instability, inflation can sometimes accompany a recession (a phenomenon known as stagflation). In such scenarios, real estate serves as a powerful hedge. Because property is a physical asset with intrinsic utility, its value tends to track with inflation over the long term. For investors, holding real estate during a recession can be a way to preserve capital when the purchasing power of the dollar is in decline.

The “Locked-In” Effect

A modern phenomenon that influences prices during a recession is the “locked-in” effect. Many current homeowners secured mortgage rates between 2% and 4% during the early 2020s. If a recession occurs and rates remain higher than those lows, these homeowners are unlikely to sell their properties, as doing so would require them to trade a low-interest loan for a much more expensive one. This creates a “supply floor,” where very few homes hit the market, keeping prices elevated even if buyer demand softens.

Supply, Demand, and the Foreclosure Myth

One of the most common fears during a recession is a wave of foreclosures that will flood the market with cheap inventory. While job losses during a recession can lead to increased mortgage delinquencies, several factors currently mitigate this risk compared to previous decades.

High Home Equity Buffers

Today’s homeowners possess record levels of home equity. Unlike in 2008, when many buyers had 0% down payments and “underwater” mortgages (owing more than the home was worth), modern lending standards have been much stricter. If a homeowner faces financial hardship today, they are more likely to sell the home at a profit or break even rather than face foreclosure, simply because the value of the home has grown so significantly in recent years.

The Chronic Housing Shortage

The fundamental driver of home prices is the balance between how many people want homes and how many homes are available. Since the 2008 crash, the U.S. has significantly under-built new housing. We are currently facing a deficit of millions of housing units. In a recession, builders often slow down production even further due to high costs of capital. This lack of new supply acts as a structural support for prices; even if demand drops by 20%, if supply is already 30% below what is needed, prices will likely remain firm.

Employment and the “Wealth Effect”

The severity of home price fluctuations is often tied to the unemployment rate. If a recession is mild and the labor market remains relatively tight, most people will continue to pay their mortgages. Real estate is an illiquid asset; unlike a stock, you cannot sell a house with the click of a button. This friction in the market prevents the “panic selling” that characterizes other asset classes, leading to “price stickiness” where sellers would rather wait out the recession than accept a low-ball offer.

Investment Strategies: Navigating a Recessionary Market

From a money-management perspective, a recession shouldn’t necessarily be a time to flee the real estate market, but rather a time to refine one’s investment strategy.

Identifying “Recession-Proof” Markets

Not all real estate is created equal. During a downturn, luxury markets often see the most significant price corrections because they rely on discretionary wealth. Conversely, “bread and butter” housing—entry-level homes in areas with diverse employment bases—tends to hold its value. Investors looking for stability should focus on regions with “sticky” industries like healthcare, education, and government services.

The Opportunity in Cash Flow

For the income-focused investor, a recession can actually be an advantageous time to acquire rental properties. While home prices may stagnate, the demand for rentals often increases as people postpone buying or are forced out of homeownership. If you can acquire a property with a long-term view, the temporary fluctuations in market value matter less than the consistent monthly yield.

Financing Challenges for Investors

While a recession might bring lower interest rates, it also brings tighter lending standards. Banks become more risk-averse, often requiring higher credit scores and larger down payments. For those looking to capitalize on a recession, maintaining high liquidity and a strong credit profile before the downturn hits is essential. In the world of finance, “cash is king” during a recession, allowing savvy investors to move quickly when opportunities arise.

Conclusion: The Long-Term View

In summary, what happens to home prices in a recession is rarely a straightforward collapse. While the 2008 experience remains a dominant memory, it was an outlier caused by systemic flaws in the housing market itself. In most economic contractions, home prices are remarkably durable, supported by falling interest rates, limited supply, and the intrinsic value of shelter.

For the individual focused on personal finance, the best approach to a recession is not to fear a total loss of home value, but to prepare for a period of stagnation. Real estate remains a long-term play. By understanding the macroeconomic levers of interest rates, supply dynamics, and equity buffers, homeowners and investors can navigate recessionary waters with confidence, recognizing that the temporary ebb and flow of the economy is merely a chapter in the longer story of wealth building through property.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.