The passing of a loved one is an emotionally taxing period, often compounded by a daunting list of administrative tasks. Among the most critical, yet frequently misunderstood, responsibilities is the management of the deceased’s financial liabilities—specifically, their credit card accounts. In the modern financial landscape, credit cards are ubiquitous, and the protocol for handling them after a death involves a specific set of legal and financial maneuvers.

Navigating this process requires a clear understanding of personal finance laws, the role of the estate, and the difference between various types of account ownership. Failure to handle these accounts correctly can lead to complications ranging from unintentional fraud to the unnecessary depletion of an inheritance. This guide explores the lifecycle of a credit card after its holder passes away, providing a roadmap for executors and family members to settle these debts professionally and efficiently.

The Immediate Actions: Notifying Creditors and Freezing Accounts

When a cardholder dies, the credit card does not simply “expire” or disappear. The account remains active in the eyes of the issuer until they are formally notified. Taking swift action is essential to prevent unauthorized charges, stop the accumulation of interest, and protect the estate from identity theft.

Identifying the Active Accounts

The first step for an executor or a close family member is to identify every open credit account. This isn’t always as simple as checking a wallet. You should review the deceased’s mail, bank statements, and digital records for recurring billing cycles. However, the most reliable method is to pull a credit report. While you cannot “apply” for credit in their name, an executor with the proper legal authority (such as Letters Testamentary) can request a copy of the deceased’s credit report to ensure no account is overlooked.

Contacting the Issuers and Credit Bureaus

Once the accounts are identified, the credit card issuers must be notified immediately. Most major banks have a dedicated “deceased notification” department. During this initial call, you should request that the account be frozen to all new charges. Simultaneously, you must notify the three major credit bureaus: Equifax, Experian, and TransUnion. You should request that a “Deceased Notice” be placed on the credit file. This prevents any new lines of credit from being opened in the deceased’s name, a common tactic used by identity thieves who monitor obituary columns.

Preventing Posthumous Identity Theft

It is a grim reality that deceased individuals are prime targets for digital security breaches. Beyond freezing the cards, the executor must ensure that all recurring subscriptions—streaming services, gym memberships, or software licenses—are canceled. If these continue to bill a frozen or closed account, they can trigger late fees and complications during the probate process. Professional management of these digital “financial footprints” is a hallmark of a well-handled estate.

Understanding Liability: Who is Responsible for the Debt?

The most common concern for survivors is whether they are personally responsible for the deceased’s credit card balances. In the realm of personal finance, the general rule is that debt belongs to the person who contracted it. However, there are significant nuances based on account structure and state law.

The Role of the Estate and Probate

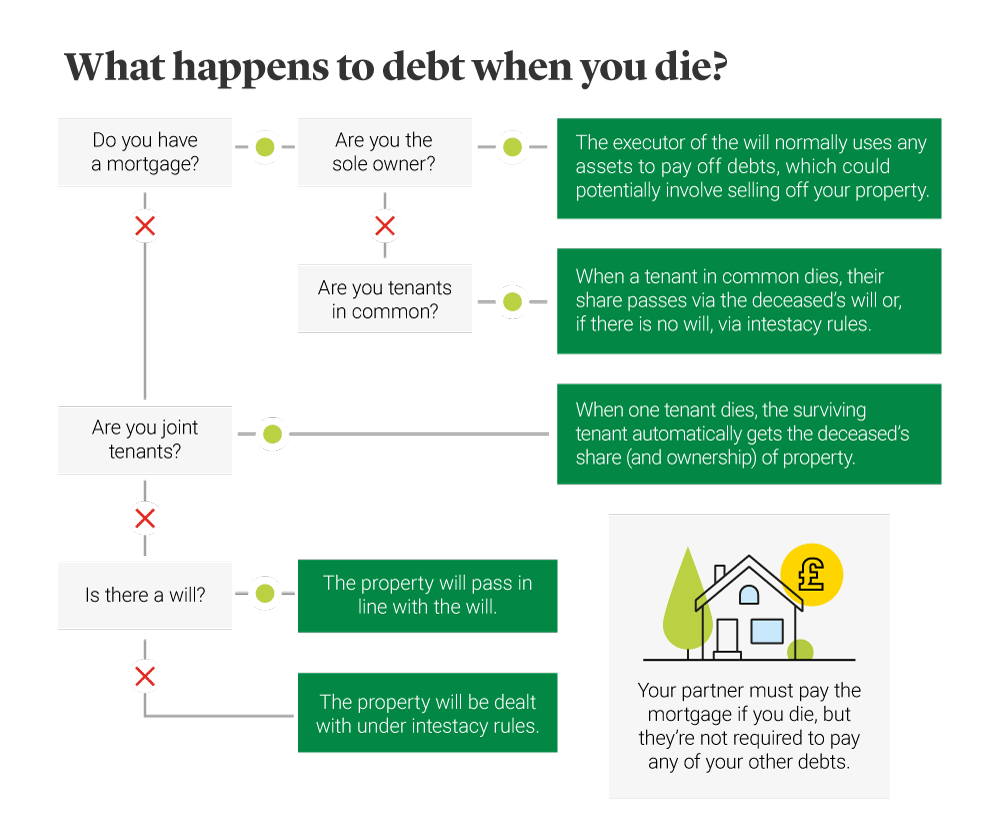

Under standard financial law, credit card debt is considered “unsecured debt.” When a person dies, their assets (cash, property, investments) form an “estate.” The executor is responsible for using these assets to pay off valid debts through a process called probate. Credit card companies are considered creditors of the estate. If there is enough money in the estate, the debt is paid off before any heirs receive their inheritance. If the estate is “insolvent”—meaning there are more debts than assets—the credit card debt often goes unpaid and is eventually written off by the creditor.

Individual vs. Joint Accounts

Liability hinges on how the account was opened. If the credit card was in the deceased’s name alone, family members are generally not responsible for the balance. However, if the account was a “Joint Account” where both parties applied and were vetted based on their combined creditworthiness, the surviving joint owner is 100% responsible for the remaining balance. This is a common point of confusion; many couples assume that if one spouse dies, the debt is halved or forgiven, which is not the case for joint accounts.

Community Property States

In the United States, your geographic location significantly impacts financial liability. In “Community Property” states (such as California, Texas, and Arizona), debts incurred by one spouse during the marriage are often considered the equal responsibility of both spouses, regardless of whose name is on the credit card. In these jurisdictions, a surviving spouse may find themselves legally obligated to settle a credit card bill they never even knew existed. Consulting with a financial advisor or estate attorney in these states is crucial to protecting personal assets.

Authorized Users vs. Co-Signers: Navigating the Differences

A frequent source of legal and financial friction arises from “authorized users.” Many people add children or spouses to their accounts to help them build credit or for convenience, but the legal standing of an authorized user is vastly different from that of a co-signer.

The Immediate Termination of Authorized User Privileges

An authorized user has the permission to use a credit card but is not legally responsible for the debt. The moment the primary cardholder dies, the legal authority for the authorized user to use that card terminates. Continuing to use the card after the primary holder’s death—even for funeral expenses or estate matters—can be classified as fraud or “unauthorized use of a credit facility.” As a matter of financial discipline, authorized users should stop using the card immediately upon the death of the primary holder and destroy their physical copy of the card.

Liability for Co-signers and Joint Cardholders

Unlike an authorized user, a co-signer has a fiduciary obligation to the debt. While co-signed credit cards are becoming rarer in the consumer market, they still exist in some niche financial products. If you co-signed for a credit card, the creditor will look directly to you for payment once the primary holder is deceased. From a personal finance perspective, this highlights the risk of co-signing; your credit score and liquidity remain tied to the account regardless of the other party’s status.

Dealing with Credit Card Rewards, Points, and Benefits

Credit cards today are more than just payment tools; they are repositories of value in the form of travel miles, cashback, and reward points. These are assets of the estate and should be managed with the same scrutiny as a bank account.

Can You Transfer Points or Miles?

The “fine print” in most credit card agreements typically states that rewards points are the property of the bank, not the cardholder, and that they expire upon the death of the holder. However, the reality is often more flexible. Many major issuers (like American Express or Chase) have policies that allow for the transfer of points to a beneficiary or the redemption of points for a statement credit to help offset the final balance. The key is to ask before the account is officially closed. Once an account is purged from the system, the points are usually lost forever.

Redeeming Benefits Before Account Closure

If the deceased had a significant balance of points, the executor should negotiate with the rewards department. Some airlines and hotel chains allow for “compassionate transfers” of miles to a family member’s account if provided with a death certificate. In terms of maximizing the estate’s value, redeeming these points for cashback to pay down the card’s own balance is often the most efficient financial move.

Practical Steps for the Executor: Closing the Chapter

The final stage of managing a deceased person’s credit cards involves the formal settlement of accounts. This requires meticulous record-keeping and a professional approach to interacting with financial institutions.

Organizing the Paperwork

To move from “freezing” an account to “closing” or “settling” it, you will need several copies of the certified death certificate. Most banks will not accept photocopies. Additionally, if you are the executor, you will need your “Letters Testamentary” or “Letters of Administration” issued by the probate court. These documents prove to the bank that you have the legal authority to act on behalf of the estate.

Negotiating Settlements with Issuers

If the estate has limited funds, the executor may need to negotiate with credit card companies. Since credit card debt is unsecured, it sits lower on the priority list than funeral expenses, taxes, and secured debts like mortgages. If there isn’t enough money to go around, the executor can often negotiate a “cents-on-the-dollar” settlement. Professionalism is key here; inform the creditors of the estate’s insolvency and provide documentation. Most banks would rather accept a partial payment than nothing at all through a protracted legal battle.

Conclusion

Managing the credit cards of the deceased is a vital component of modern estate settlement. By acting quickly to notify bureaus, understanding the nuances of liability, and handling rewards points as legitimate assets, you can ensure the financial legacy of your loved one is handled with dignity. For those currently planning their own estates, this highlights the importance of keeping an organized record of accounts and understanding how your debt might impact those you leave behind. In the world of personal finance, clarity is the greatest gift you can leave your survivors.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.