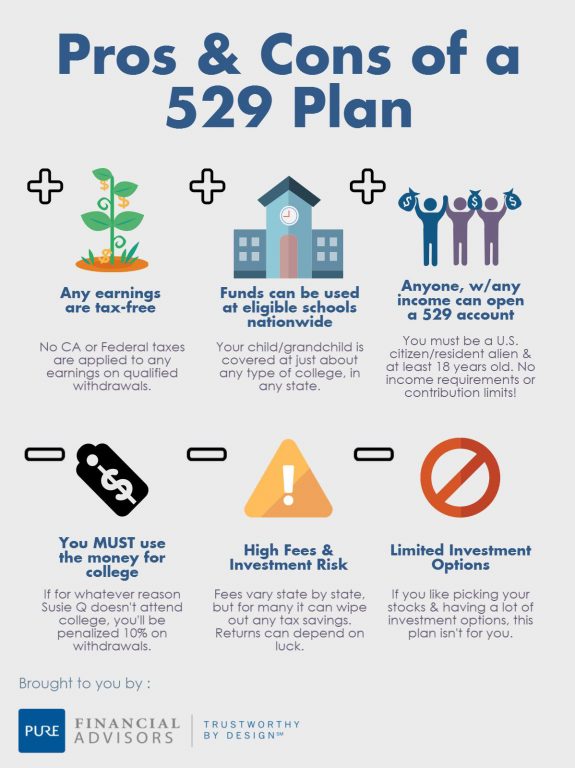

For many parents and guardians, opening a 529 college savings plan is a cornerstone of responsible financial planning. The promise of tax-free growth and tax-free withdrawals for qualified educational expenses makes it one of the most powerful tools in the personal finance arsenal. However, life rarely follows a linear path. A child might receive a full-ride scholarship, decide to pursue a path other than traditional higher education, or the account might simply be overfunded due to diligent saving and strong market performance.

The question then arises: What happens to that money? There is a common misconception that funds in a 529 plan are “use it or lose it.” In reality, the 529 plan is remarkably flexible. While there are tax implications for using the money on non-educational expenses, several strategic pivots allow you to retain the value of your investment without incurring heavy penalties.

The Tax Consequences of Non-Qualified Withdrawals

Before exploring the alternatives, it is essential to understand the “worst-case scenario.” If you decide to simply withdraw the money for a purpose that does not meet the IRS definition of a qualified higher education expense—such as buying a car or a home—the withdrawal is considered “non-qualified.”

The Principal vs. Earnings Distinction

A 529 plan consists of two parts: your original contributions (the principal) and the investment growth (the earnings). Because your contributions were made with after-tax dollars, you can always withdraw the principal portion of the account tax-free and penalty-free at any time. The penalties only apply to the earnings.

Taxes and the 10% Penalty

When you make a non-qualified withdrawal, the earnings portion is subject to ordinary federal income tax at your current tax rate. Furthermore, the IRS imposes a 10% federal tax penalty on those earnings. Depending on your state, you may also be required to pay state income taxes and potentially “recapture” any state tax deductions or credits you received when you initially made the contributions. While this is not ideal, it is rarely the “financial catastrophe” some fear, as the bulk of the account is often the principal you already paid taxes on.

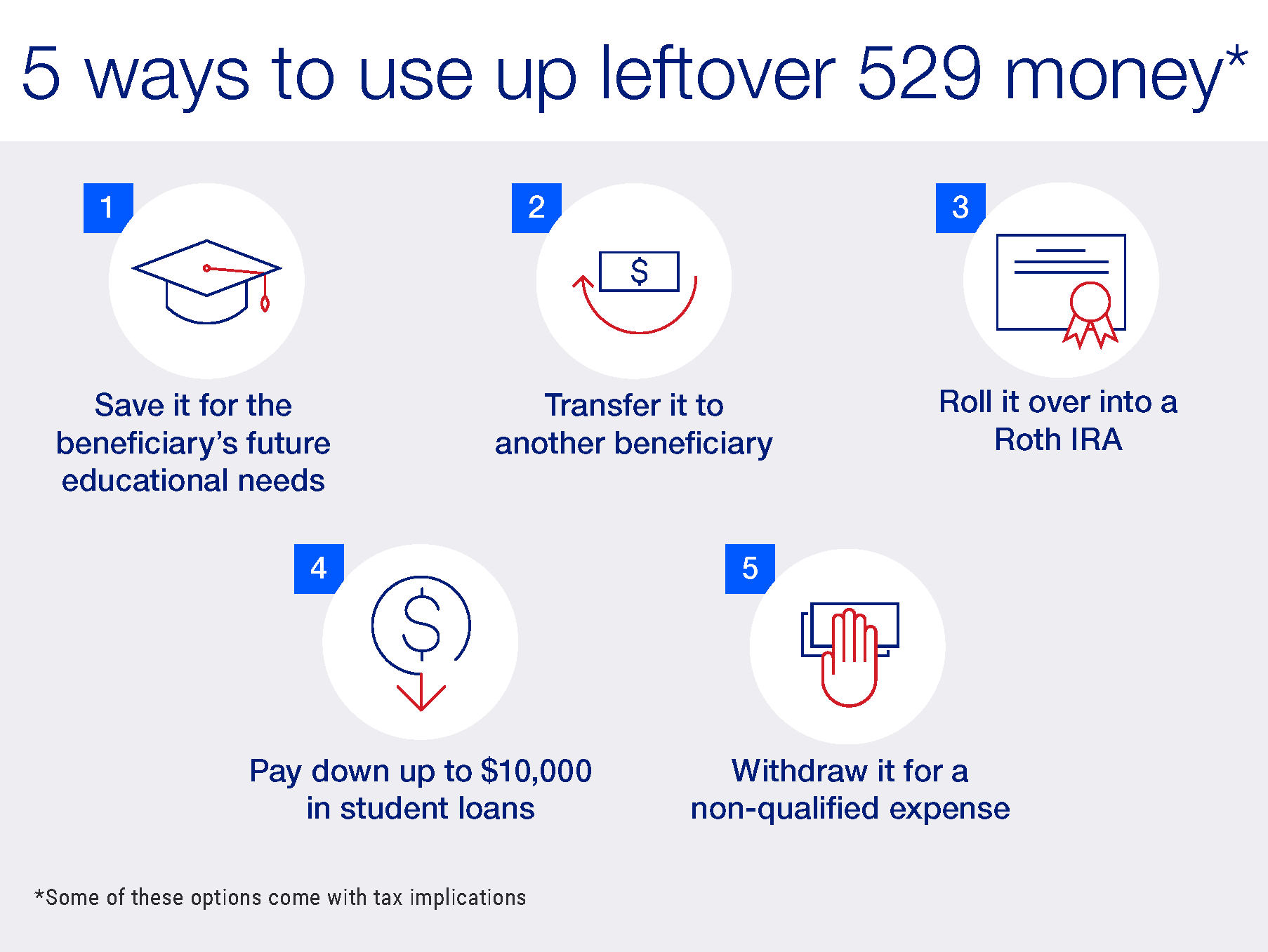

Strategic Pivot 1: Changing the Beneficiary

One of the most attractive features of a 529 plan is that the account owner retains full control over the funds, including the right to change the beneficiary. If the original beneficiary (the child) does not need the funds, you can redirect the money to another “member of the family” without triggering any taxes or penalties.

Broad Definition of “Family Member”

The IRS provides a surprisingly generous definition of who qualifies as a family member for a beneficiary change. This includes:

- Siblings (including step-siblings)

- Parents or ancestors

- Nieces and nephews

- Aunts and uncles

- First cousins

- In-laws (mother-in-law, father-in-law, etc.)

- Even the account owner themselves

Multi-Generational Wealth Planning

If you have no immediate need for the funds, you can change the beneficiary to a future grandchild or even yourself. For example, if you decide to go back to school for an MBA or take a professional development course at an accredited institution, those 529 funds can be used for your own tuition and books. By keeping the money in the plan and naming a younger relative, you allow the funds to continue growing tax-free for decades, potentially creating a “legacy fund” for education that spans generations.

Strategic Pivot 2: The SECURE 2.0 Act and Roth IRA Rollovers

A major shift in the financial landscape occurred with the passage of the SECURE 2.0 Act. Starting in 2024, account owners have a new, highly efficient way to handle leftover 529 funds: rolling them over into a Roth IRA for the beneficiary. This effectively turns an “education fund” into a “retirement fund,” solving the dilemma of overfunding.

Requirements for the 529-to-Roth Rollover

To prevent abuse of this rule, the IRS has established specific guidelines:

- The 15-Year Rule: The 529 account must have been open for at least 15 years.

- The 5-Year Rule: You cannot roll over contributions (or the earnings on those contributions) made within the last five years.

- Lifetime Limit: There is a lifetime maximum of $35,000 per beneficiary that can be rolled over from a 529 to a Roth IRA.

- Annual Limits: The rollover amount is subject to annual Roth IRA contribution limits. For example, if the limit is $7,000, you can only roll over $7,000 in a single year, and the beneficiary must have earned income equal to at least that amount.

The Benefit of Early Retirement Savings

This option is a game-changer for personal finance. It allows parents to jump-start their child’s retirement savings with tax-free growth that was originally intended for college. If a student graduates without debt and has $35,000 moved into a Roth IRA in their early 20s, that money has forty years to compound, potentially turning into hundreds of thousands of dollars by the time they reach retirement age.

Exceptions to the 10% Penalty Rule

There are specific circumstances where you can withdraw earnings from a 529 plan for non-educational purposes without paying the 10% penalty. It is important to note that while the penalty is waived, you will still owe ordinary income tax on the earnings.

The Scholarship Exception

If the beneficiary receives a scholarship, the IRS allows you to withdraw an amount equal to that scholarship from the 529 plan penalty-free. For example, if your child receives a $10,000 scholarship, you can take $10,000 out of the 529 plan to use for any purpose. This ensures that students are not “punished” for their academic or athletic success.

Military Academies and Disability

Similar to the scholarship exception, if the beneficiary attends a U.S. Military Academy (such as West Point or Annapolis), the 10% penalty is waived on withdrawals used to offset the value of the education provided. Additionally, if a beneficiary becomes disabled or passes away, the penalty is waived for withdrawals made from the account.

Apprenticeships and Student Loan Repayments

In recent years, the definition of “qualified expenses” has expanded. You can now use 529 funds to pay for fees, books, and equipment required for a registered apprenticeship program. Furthermore, under the SECURE Act of 2019, you can use a lifetime maximum of $10,000 per individual to pay down qualified student loans for the beneficiary or their siblings.

Tactical Planning: How to Avoid Overfunding

While having “too much” money in a 529 plan is a better problem than having too little, proactive financial management can help you avoid the tax bite of non-qualified withdrawals altogether.

Use the 529 for K-12 Tuition

Many people associate 529 plans exclusively with college. However, you can use up to $10,000 per year, per beneficiary, to pay for tuition at elementary, middle, or high schools (private or religious). If you realize your college savings are on track to exceed your needs, you can begin drawing down the funds earlier to cover K-12 costs.

Coordinate with Other Assets

When planning your education savings, it is often wise to use a “bucket” approach. Instead of putting every available dollar into a 529 plan, consider balancing it with a standard brokerage account or a Roth IRA (which allows for penalty-free withdrawal of original contributions for any reason). By diversifying your “tax wrappers,” you gain the flexibility to pivot if the beneficiary’s plans change.

Monitor the “Coast” Point

Financial advisors often recommend identifying a “coast” point—the moment when the current balance in your 529 plan, combined with projected market growth, is likely to cover the remaining years of education. Once you hit this point, you might stop contributing to the 529 and redirect those funds toward your own retirement or a more flexible taxable investment account.

Conclusion

The fear of “losing” money in a 529 plan is largely unfounded. Between the ability to change beneficiaries, the new Roth IRA rollover provisions, and the scholarship penalty waivers, the 529 plan remains one of the most flexible and secure ways to build wealth for the next generation. By understanding these rules, you can save with confidence, knowing that even if the original plan for higher education changes, the financial value you have built remains protected and productive. Whether it becomes a retirement nest egg for your child or a college fund for a future grandchild, your 529 contributions are never truly “wasted.”

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.