The year 1929 stands as an indelible scar on the canvas of American economic history, a watershed moment that irrevocably reshaped financial markets, government policy, and the very psyche of a nation. More than just a date, it signifies the dramatic collapse of an era of unprecedented prosperity and rampant speculation, ushering in the gravest economic downturn the modern world has ever witnessed: the Great Depression. To understand 1929 is to delve into the intricate dance of market forces, human psychology, and policy failures that culminated in a financial cataclysm, offering enduring lessons for investors, policymakers, and ordinary citizens on the perils of unchecked optimism and systemic vulnerabilities.

The Roaring Twenties: A Foundation of Fragility

The decade preceding 1929, famously dubbed the “Roaring Twenties,” was characterized by an effervescent mix of technological innovation, cultural liberalization, and exuberant economic growth. From the widespread adoption of automobiles and radios to the burgeoning consumer culture, America appeared to be on an unstoppable trajectory of prosperity. Yet, beneath this glittering surface, foundational weaknesses were steadily accumulating, creating a highly unstable financial environment ripe for disruption.

Unbridled Optimism and Speculative Mania

A defining feature of the Roaring Twenties was a pervasive, almost irrational, optimism concerning the stock market. The Dow Jones Industrial Average soared, quadrupling in value between 1921 and 1929. Corporate profits were strong, but the stock prices often far outstripped their underlying earnings, driven by a widespread belief that the market would continue its upward climb indefinitely. This period saw the stock market transition from being a domain primarily for professional investors to a national pastime, with shoe-shine boys and factory workers alike pouring their savings into shares. The allure of quick riches fostered a “get-rich-quick” mentality that overshadowed fundamental financial prudence. People were increasingly investing not in the long-term value of companies, but in the short-term prospect of selling their shares for a higher price.

The Perilous Practice of Buying on Margin

Central to the speculative bubble was the widespread practice of “buying on margin.” This allowed investors to purchase stocks with borrowed money, sometimes paying as little as 10% of the stock’s value upfront and borrowing the rest from their brokers. As long as stock prices rose, investors could sell their shares at a profit, repay the loan, and pocket the difference. However, this amplified both gains and losses. If stock prices fell, brokers would issue a “margin call,” demanding immediate repayment of the loan. If the investor couldn’t cover it, their shares would be sold, often at a loss, to satisfy the debt. This mechanism created a highly leveraged market, making it extremely vulnerable to any significant downturn, as a cascade of margin calls could trigger a spiral of forced selling.

Underlying Economic Disparities and Structural Weaknesses

While urban centers and industrial sectors boomed, not all segments of the American economy shared equally in the prosperity. Agriculture, for instance, had been in a prolonged slump since the end of World War I, with overproduction leading to depressed prices and widespread rural poverty. Income inequality was also significant, meaning that purchasing power was not evenly distributed, limiting the overall domestic demand for goods despite increasing production capacity. Furthermore, the banking system was largely unregulated and fragmented, with thousands of small, independent banks susceptible to runs and failures. There was no federal deposit insurance, meaning that if a bank failed, depositors lost everything. Internationally, protectionist trade policies, particularly the Hawley-Smoot Tariff which was under debate during 1929, threatened global trade, further exacerbating the domestic economy’s fragile footing.

Black Tuesday: The Market’s Demise and Immediate Fallout

The seemingly unstoppable ascent of the stock market met its brutal reckoning in October 1929, culminating in a series of catastrophic trading days that would forever be etched in financial history. The abrupt and violent correction shattered the illusion of perpetual prosperity, sending shockwaves through the American and global financial systems.

The Days Leading Up to the Crash

The first signs of trouble emerged in September 1929, with some minor market fluctuations that were largely dismissed as healthy corrections. However, by mid-October, the market started to show more significant weakness. On October 24, 1929, a day now known as “Black Thursday,” a torrent of selling began. The market opened lower, and by mid-morning, prices were plummeting, triggering widespread panic. While a consortium of leading bankers intervened by pooling funds to buy stocks and stabilize prices, the reprieve was short-lived and ultimately insufficient to stem the tide. The damage to investor confidence was already done.

The Panic Sells and Market Freefall

The true devastation arrived on October 28, “Black Monday,” when the market experienced an unprecedented 13% decline, an event that dwarfed previous downturns. This was merely a prelude to “Black Tuesday,” October 29, 1929. On this single day, an astounding 16 million shares were traded—a record that would stand for decades—as a frenzy of selling gripped Wall Street. The ticker tapes couldn’t keep up with the volume, spreading confusion and exacerbating the panic. Investors, particularly those who had bought on margin, faced margin calls they couldn’t meet, forcing them to liquidate their holdings at any price, driving values even lower. The Dow Jones Industrial Average lost another 12% on Black Tuesday, wiping out billions of dollars in market value in a matter of hours. The combined losses over these few days were equivalent to more than $30 billion, a staggering sum for the era, exceeding the total cost of World War I for the United States.

Immediate Financial Fallout and Psychological Impact

The immediate aftermath of the crash was one of profound shock and economic uncertainty. Wealth evaporated overnight, destroying the life savings of countless individuals and families. The psychological impact was immense; the dreams of a generation were shattered, replaced by fear, despair, and a deep distrust in financial institutions. While the crash itself did not cause the Great Depression single-handedly, it acted as a brutal catalyst, severely contracting consumer and business confidence, and triggering a cascade of events that would unravel the entire economy. Businesses suddenly found it harder to raise capital, consumers cut back spending, and banks, many heavily invested in the stock market or having lent to speculators, found their balance sheets severely weakened.

The Unraveling Economy: From Crash to Depression

The stock market crash of 1929 was not an isolated incident but the opening act of a much larger economic tragedy. The ensuing years saw a relentless deterioration of economic conditions, transforming a sharp market correction into the most severe and prolonged depression in American history, characterized by mass unemployment, deflation, and widespread poverty.

Banking System Collapse and Credit Contraction

One of the most devastating consequences of the crash was the widespread failure of the American banking system. With no federal deposit insurance, depositors, fearing their banks would fail, rushed to withdraw their money, initiating “bank runs.” These runs forced banks, which typically only held a fraction of deposits in cash, to call in loans and sell assets, often at fire-sale prices, further exacerbating the economic downturn. Between 1930 and 1933, thousands of banks failed, wiping out billions in savings and tightening the availability of credit, paralyzing businesses and consumers alike. The contraction of credit meant that businesses could not invest or expand, and individuals could not borrow, stifling economic activity at every level.

Deflation and Soaring Unemployment

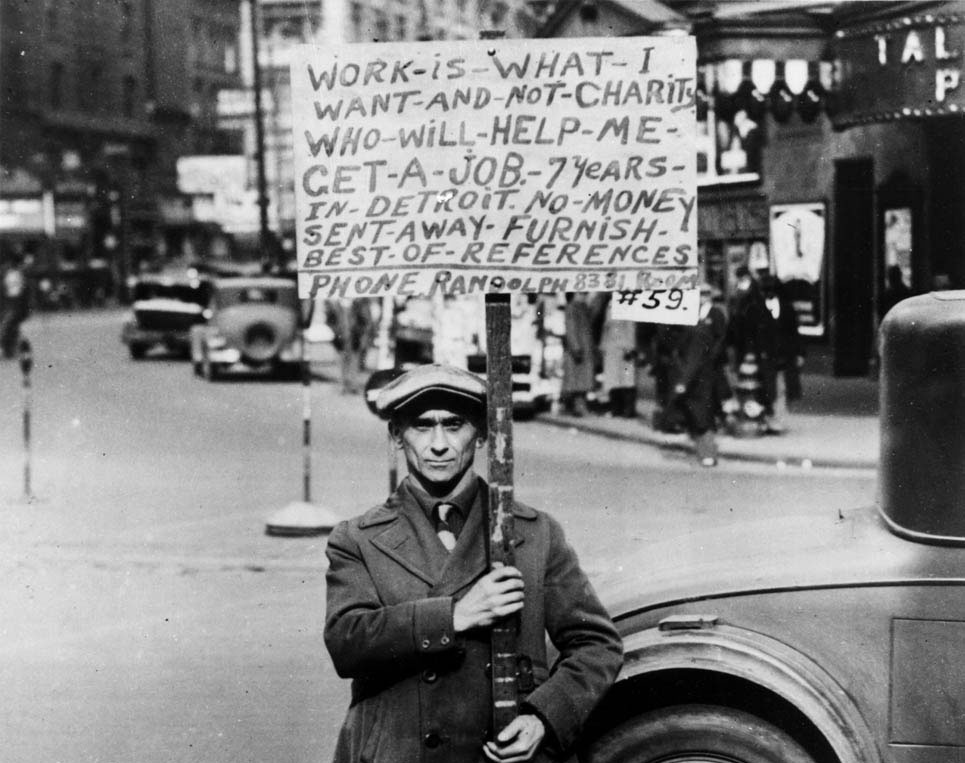

As demand plummeted and businesses scaled back, prices for goods and services began a downward spiral, a phenomenon known as deflation. While seemingly beneficial for consumers, deflation is ruinous for an economy. It makes debts harder to repay (as the value of money increases), discourages spending (as people wait for lower prices), and erodes corporate profits, forcing businesses to cut production and lay off workers. Unemployment skyrocketed, reaching an unprecedented 25% by 1933. Millions of Americans lost their jobs, their homes, and their dignity, leading to widespread poverty, homelessness, and social unrest. The lack of a social safety net meant that families often faced starvation and destitution with little government assistance.

Government Inaction and Policy Missteps

Initial government responses were largely inadequate and, in some cases, counterproductive. President Herbert Hoover, adhering to principles of limited government intervention and self-reliance, initially believed the market would correct itself and that direct federal aid would undermine individual initiative. His administration’s attempts, such as urging businesses to maintain wages and public works projects, proved insufficient against the scale of the crisis. Moreover, the Federal Reserve, the nation’s central bank, failed to act as a lender of last resort to distressed banks, further contributing to the banking crisis. The infamous Smoot-Hawley Tariff Act, signed into law in 1930, raised import duties to record levels, sparking retaliatory tariffs from other countries and severely choking international trade, further deepening the global economic downturn and isolating the U.S. economy.

Lessons from the Abyss: Enduring Financial Insights

The crucible of 1929 and the subsequent Great Depression forged a new understanding of economic governance and financial regulation. The painful lessons learned continue to inform modern financial policy, risk management, and investment strategies, serving as a perpetual reminder of the delicate balance required for sustained economic stability.

The Birth of Modern Financial Regulation and Oversight

The most significant long-term impact was the transformation of America’s financial regulatory landscape. The New Deal era, under President Franklin D. Roosevelt, introduced a raft of legislation designed to prevent a recurrence of such a catastrophe. Key reforms included the Glass-Steagall Act (1933), which separated commercial and investment banking (though largely repealed in 1999, it influenced the Dodd-Frank Act post-2008); the creation of the Federal Deposit Insurance Corporation (FDIC) in 1933, which restored confidence in banks by insuring depositors’ money; and the establishment of the Securities and Exchange Commission (SEC) in 1934, tasked with regulating stock exchanges and protecting investors from fraud and manipulation. These institutions remain cornerstones of modern financial governance, aimed at promoting transparency, accountability, and stability.

Understanding Market Bubbles and Systemic Risk

The events of 1929 underscored the dangers of speculative bubbles and the concept of systemic risk. It demonstrated how unchecked market enthusiasm, fueled by leverage, can create unsustainable valuations that are vulnerable to sudden collapse. The crash highlighted that financial markets are not merely abstract systems but are deeply intertwined with human psychology—greed, fear, and herd mentality—which can lead to irrational exuberance and devastating panics. Modern economists and financial analysts now pay close attention to indicators of market overheating, credit expansion, and asset bubbles, understanding that a crisis in one part of the financial system can quickly cascade and threaten the entire economy.

The Importance of Diversification and Long-Term Investing

For individual investors, 1929 provided a harsh but invaluable lesson in sound financial principles. The collapse of highly concentrated portfolios, often built on speculative margin buying, underscored the critical importance of diversification across different asset classes and geographies. It reinforced the idea that investing should be a long-term endeavor, focused on fundamental value and growth, rather than a short-term gamble based on market timing or speculative trends. The post-crash era saw a gradual shift towards more conservative investment strategies, with an emphasis on capital preservation and robust financial planning. The concept of “buy and hold” and dollar-cost averaging gained prominence as ways to mitigate market volatility and build wealth steadily over time.

Personal Finance in the Wake of Disaster: A New Paradigm

The seismic shifts of 1929 and the subsequent Depression profoundly altered the way Americans viewed personal finance, savings, and security. A generation scarred by economic hardship developed a deep-seated conservatism and a renewed appreciation for financial resilience.

A Shift in Consumer Behavior and Thrift

The experience of the Great Depression instilled a strong sense of thrift and frugality in survivors. Debt was viewed with extreme caution, and saving, even small amounts, became a priority. This generation learned to “make do” with less, reuse items, and prioritize necessities over luxuries. This cautious consumer behavior, while necessary during the lean years, also contributed to slower economic recovery as demand remained suppressed. However, it also fostered a culture of financial prudence that lasted for decades, influencing how future generations approached spending, saving, and debt.

The Enduring Value of Emergency Savings

The widespread destitution and unemployment of the Depression era made it painfully clear that financial stability was precarious. The absence of a robust social safety net meant that personal savings were often the only buffer against utter ruin. This experience cemented the concept of an “emergency fund” as a critical component of personal finance, emphasizing the need to set aside several months’ worth of living expenses to guard against unforeseen job loss, illness, or other financial shocks. This principle remains a cornerstone of responsible personal financial planning today.

Redefining Wealth and Security

Before 1929, wealth was often equated with speculative gains and the dazzling promise of the stock market. After the crash and the Depression, the definition of wealth and security fundamentally shifted. Real estate, tangible assets, and steady, secure employment gained immense value. Financial security became less about rapid accumulation through speculation and more about stability, steady income, freedom from debt, and the ability to weather economic storms. The trauma of 1929 ingrained a powerful lesson: true financial well-being is built on a foundation of prudence, diversification, and a clear understanding of risk, rather than succumbing to the intoxicating allure of easy money.

In conclusion, 1929 was not merely a year of financial collapse; it was a crucible that refined America’s understanding of economic principles, governance, and personal financial responsibility. The echoes of Black Tuesday resonate through every modern financial regulation, every investment strategy, and every piece of advice on emergency savings. It stands as a timeless reminder that while prosperity can soar to dizzying heights, vigilance, regulation, and a healthy respect for economic cycles are essential to prevent a catastrophic fall.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.