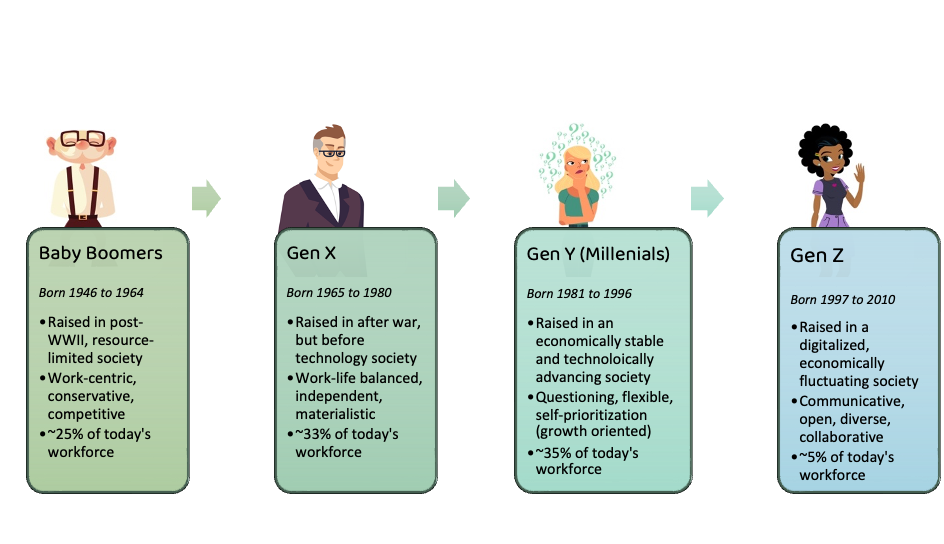

When we discuss the transition of wealth and the evolution of the global economy, the conversation often lingers on the massive influence of Baby Boomers or the disruptive digital habits of Millennials. However, situated directly between these two demographic titans is the generation that followed the Boomers: Generation X. Born roughly between 1965 and 1980, Generation X is often dubbed the “forgotten generation,” yet from a financial perspective, they are currently the most critical players in the market.

As the generation after the Boomers, Gen X is currently navigating their peak earning years. They occupy the majority of senior management roles, hold significant purchasing power, and are the primary architects of modern family offices and retirement portfolios. This article explores the unique financial landscape of Generation X, focusing on their role as the “sandwich generation,” their sophisticated approach to investing, and how they are preparing for the largest wealth transfer in human history.

The Economic Architecture of the Post-Boomer Era

To understand the financial behavior of Generation X, one must first understand the economic environment in which they came of age. Unlike the Boomers, who benefited from a post-war boom and the proliferation of defined-benefit pension plans, Gen X was the first generation to be largely responsible for their own retirement through defined-contribution plans like the 401(k).

The Shift from Pensions to Personal Responsibility

Generation X entered the workforce just as the traditional “gold watch” retirement model began to fade. This forced a fundamental shift in personal finance. Instead of relying on corporate guarantees, this generation had to master the nuances of mutual funds, stock market fluctuations, and tax-advantaged accounts early in their careers. This self-reliance has made Gen X a generation of pragmatic investors who value diversification and transparency over blind institutional trust.

Peak Earning Years and Wealth Accumulation

Currently aged between 44 and 59, the majority of Gen Xers are in the “sweet spot” of their careers. Their income levels are at an all-time high, allowing for aggressive debt reduction and significant contributions to investment portfolios. However, this period of high earning is often offset by high expenses, as they navigate the complexities of late-stage mortgage payments, peak tax brackets, and the rising costs of higher education for their children.

Navigating the Challenges of the Sandwich Generation

One of the most defining financial characteristics of the generation after Boomers is their position as the “Sandwich Generation.” This demographic is simultaneously providing financial support to their aging Boomer parents while funding the lifestyles and educations of their Millennial or Gen Z children.

Balancing Elder Care and Educational Funding

The financial pressure of caring for two different generations is immense. Gen X investors must find a balance between the emotional desire to support family and the mathematical necessity of securing their own retirement. Professional financial planning for this group often involves complex “stress tests” to determine how long-term care for parents might impact their own net worth. The rise of long-term care insurance and health savings accounts (HSAs) has become a staple in the Gen X financial toolkit to mitigate these risks.

The Importance of Liquid Emergency Reserves

Because of these dual pressures, the traditional advice of keeping three to six months of expenses in an emergency fund is often insufficient for Gen X. Financial advisors now recommend that post-Boomer professionals maintain a “stability fund” that accounts for potential medical emergencies for parents or extended periods of unemployment for adult children. This necessity for liquidity has driven Gen X interest in high-yield savings accounts and short-term treasury bills, ensuring that wealth is accessible without incurring market-timing penalties.

Investment Strategies for the Retirement Home Stretch

With retirement no longer a distant concept but a looming reality, the generation after Boomers is aggressively recalibrating their portfolios. The focus is shifting from pure growth to a more nuanced balance of capital preservation and inflation-protected income.

Moving from Aggressive Growth to Strategic Preservation

In their 20s and 30s, many Gen Xers benefited from the tech booms and market recoveries of the 90s and early 2000s. Now, they are increasingly utilizing “target-date funds” or custom-built portfolios that slowly de-risk as they approach their 60s. However, because life expectancy is increasing, Gen X cannot afford to be entirely conservative. They are maintaining a significant allocation in equities—particularly dividend-paying stocks and ETFs—to ensure their purchasing power isn’t eroded by inflation over a thirty-year retirement.

Maximizing Catch-Up Contributions and Tax Efficiency

The IRS provides a “catch-up” provision for individuals aged 50 and older, allowing them to contribute more to their 401(k) and IRA accounts. For Gen X, these contributions are the primary engine for closing any gaps in their retirement savings. Furthermore, this generation is becoming highly sophisticated in tax-loss harvesting and utilizing Roth conversions to minimize the tax bite on their distributions later in life. They understand that it’s not just about how much they grow their money, but how much they keep after the government takes its share.

Digital Income and the Modern Side Hustle

While Millennials are often credited with the “Gig Economy,” the generation after Boomers has successfully co-opted these tools to bolster their personal finance. Gen X is leveraging decades of corporate expertise to create high-value consulting side hustles and digital income streams.

Leveraging Corporate Experience in the Gig Economy

Many Gen X professionals are realizing that their specialized knowledge is a tradable commodity. Through platforms like LinkedIn, or through private consulting firms, they are generating secondary income that is often funneled directly into brokerage accounts. This “active-passive” income allows them to accelerate their retirement timeline without sacrificing their current lifestyle.

Real Estate and Passive Income Streams

Beyond the stock market, Gen X has a strong affinity for tangible assets. This generation holds a significant portion of the residential real estate market, not just as primary residences, but as rental properties. By utilizing modern property management software and platforms like Airbnb, they have turned real estate into a scalable source of passive income. This diversification serves as a hedge against stock market volatility and provides a steady cash flow that is independent of their primary salary.

Preparing for the Great Wealth Transfer

Perhaps the most significant financial event for the generation after the Boomers is the impending “Great Wealth Transfer.” As Baby Boomers pass on their assets, an estimated $68 trillion is expected to change hands, with Generation X being the primary recipients.

Managing Inheritances and Windfalls

Receiving a significant inheritance can be a double-edged sword. Gen Xers are increasingly seeking professional advice on how to integrate inherited IRAs, real estate, and taxable brokerage accounts into their existing financial plans. The goal is to avoid the “lottery winner” trap where sudden wealth is squandered. Instead, they are using these windfalls to pay off remaining debt, fund generational trusts, or pivot into early retirement.

Estate Planning and Building a Multi-Generational Legacy

Having seen the complexities of settling their parents’ estates, Gen X is remarkably proactive about their own estate planning. They are the generation of “living trusts” and “pour-over wills.” By utilizing financial tools to bypass probate and minimize estate taxes, they are ensuring that the wealth they have built—and inherited—remains within the family. They are not just focused on their own comfort; they are focused on establishing a financial foundation for the generations that follow them.

In conclusion, Generation X—the generation after the Boomers—is far from “forgotten” in the world of finance. They are the linchpin of the current economy, managing the most complex financial lives of any demographic. By balancing the needs of their parents and children, maximizing their peak earning years, and preparing for a massive transfer of assets, they are setting a new standard for mid-life financial management. As they move toward retirement, their pragmatic, tech-savvy, and diversified approach to money will continue to shape the global financial landscape for decades to come.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.