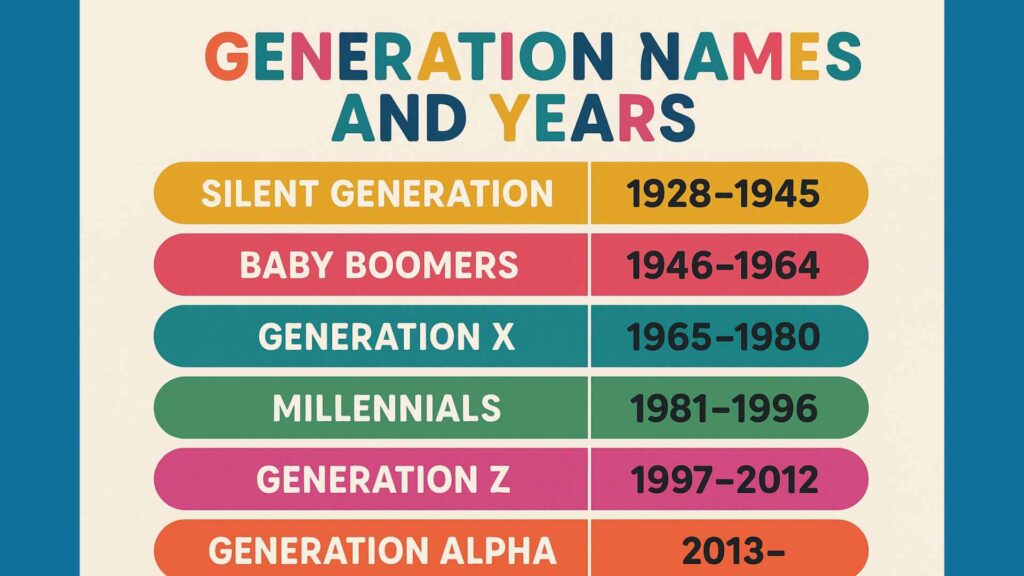

Understanding the generational identity of those born in 1945 requires looking beyond a simple birth year. In the world of sociology and demographics, individuals born in 1945 belong to the Silent Generation, sometimes referred to as the “Builders” or “Traditionalists.” This cohort, born roughly between 1928 and 1945, occupies a unique space in history, wedged between the “Greatest Generation” that fought World War II and the massive “Baby Boomer” surge that began in 1946.

From a financial perspective, the 1945 birth year is particularly significant. Those born in this year arrived just as the global economy was restructuring itself following the most destructive conflict in human history. This upbringing forged a specific financial psyche characterized by fiscal conservatism, a high degree of loyalty to institutions, and a “waste-not, want-not” mentality. As this cohort moves through their late 70s and early 80s, their financial focus has shifted from accumulation to preservation and, crucially, the “Great Wealth Transfer.”

Identifying the 1945 Cohort: The Silent Generation’s Financial DNA

To understand the financial behavior of those born in 1945, one must understand the economic landscape of their formative years. Unlike the Boomers who followed them, the Silent Generation was a relatively small demographic. However, their impact on the global economy and modern investment structures is disproportionately large.

From Post-War Scarcity to Economic Expansion

Individuals born in 1945 entered the world at the dawn of the Bretton Woods system, which established the US dollar as the world’s primary reserve currency. Their childhoods were defined by the rebuilding of Europe and the massive industrial expansion of North America. This era was marked by a transition from the scarcity of the Great Depression and war years to a period of unprecedented economic growth. Financially, this created a generation that respects the value of a dollar but also understands the power of long-term infrastructure and industrial investment.

The “Builder” Mentality and Savings Habits

The financial DNA of someone born in 1945 is rooted in the concept of “building.” This generation prioritized homeownership, long-term employment with a single company, and the security of defined-benefit pension plans. Unlike the gig-economy workers or the “job-hoppers” of later generations, the 1945 cohort viewed financial success as a slow, steady climb. This has resulted in a generation that typically holds higher levels of home equity and lower levels of consumer debt relative to their younger counterparts. Their savings habits were not driven by the desire for “early retirement” as we know it today, but by the desire for stability and the avoidance of the financial ruin their parents witnessed during the 1930s.

Wealth Management for the 79-Year-Old Investor

As individuals born in 1945 reach the age of 79, their financial priorities are distinct from any other age group. At this stage of the life cycle, the primary objective is capital preservation and income floor sustainability. The strategies that worked during their 50s and 60s are no longer applicable, and the risks they face are significantly more acute.

Asset Allocation in the Decumulation Phase

For the 1945 generation, the investment portfolio has likely transitioned from a growth-oriented mix to a conservative, income-generating engine. The “decumulation” phase—the process of spending down assets during retirement—requires a delicate balance. A common strategy involves a heavy weighting toward high-quality fixed income, dividend-paying stocks, and cash equivalents. However, with modern longevity, a 79-year-old might still have a 15-to-20-year horizon, meaning they cannot completely exit the equity market without risking the erosion of their purchasing power.

Mitigating Inflationary Risks on Fixed Incomes

While the Silent Generation is often associated with the security of Social Security and pensions, inflation remains a formidable enemy. For someone born in 1945, the high-inflation era of the late 1970s is a vivid memory. Today, managing “real” returns—returns adjusted for inflation—is essential. Financial advisors working with this demographic often utilize Treasury Inflation-Protected Securities (TIPS) or annuities with cost-of-living adjustments (COLAs) to ensure that the purchasing power of their fixed income remains stable even as the cost of healthcare and basic goods rises.

The Great Wealth Transfer: Passing the Torch

We are currently witnessing what economists call the “Great Wealth Transfer.” It is estimated that trillions of dollars will pass from the Silent Generation and older Boomers to Gen X and Millennials over the next two decades. For those born in 1945, the focus has shifted from personal consumption to the efficient transfer of assets.

Estate Planning and Tax Efficiency

For the 1945 cohort, estate planning is not merely about writing a will; it is about sophisticated tax mitigation. This involves the use of Irrevocable Trusts, Charitable Remainder Trusts (CRTs), and strategic gifting. Under current tax laws, individuals can leverage the annual gift tax exclusion to reduce the size of their taxable estate while providing immediate financial support to their heirs. For those with significant assets, the goal is often to minimize the impact of federal and state estate taxes, ensuring that the wealth they built over seven decades remains within the family or supports chosen philanthropic causes.

Preparing Gen X and Millennials for Inheritance

A critical component of financial management for the 1945 generation is “intergenerational financial literacy.” Many born in 1945 are concerned that their heirs—often Gen Xers in their 50s or Millennials in their 30s and 40s—may not be prepared to manage a sudden influx of wealth. Consequently, we are seeing a rise in “family office” style management even for moderately wealthy families. This involves joint meetings with financial advisors where the 1945 patriarch or matriarch discusses the family’s financial values, the history of the assets, and the responsibilities that come with stewardship.

Navigating Modern Financial Tools in Late Retirement

While those born in 1945 grew up in an era of paper ledgers and physical bank branches, they are now navigating a digital-first financial world. Adapting to modern financial technology (Fintech) is a dual-edged sword for this generation: it offers unprecedented convenience but introduces new risks.

Fintech Accessibility for the Silent Generation

The “Silent” generation is more tech-savvy than stereotypes suggest, but their adoption of fintech is driven by utility rather than novelty. Mobile banking, online bill pay, and digital portfolio tracking have become essential tools for the 79-year-old who may have mobility issues or who spends part of the year in a different climate (the “snowbird” lifestyle). Financial institutions that prioritize high-contrast interfaces, simplified navigation, and robust phone support are winning the loyalty of this demographic, who still value a human connection alongside digital efficiency.

Protecting Assets from Financial Fraud

The most significant financial threat to those born in 1945 is not market volatility, but financial exploitation and fraud. As this generation holds a significant portion of the world’s liquid wealth, they are primary targets for sophisticated scams, ranging from “grandparent scams” to complex phishing schemes. Professional wealth management for this group now must include “financial defense” strategies. This includes setting up “view-only” access for trusted adult children, implementing multi-factor authentication on all accounts, and utilizing “trusted contact” forms at brokerage firms. Protecting the nest egg from external threats is as important as the investment strategy itself.

Conclusion: The Legacy of the 1945 Cohort

The year 1945 was a pivot point for the world, and the individuals born in that year embody the transition from old-world discipline to modern economic complexity. As the tail end of the Silent Generation, they are the stewards of a massive amount of global capital. Their financial journey—from the post-war industrial boom to the digital age—offers a masterclass in patience, discipline, and the power of compound interest.

For the 1945-born individual, the current financial landscape is about more than just numbers on a screen; it is about the culmination of a lifetime of work and the strategic preservation of a legacy. By focusing on smart decumulation, rigorous estate planning, and the adoption of secure financial technologies, they are ensuring that the “Builder” generation’s influence will be felt for many decades to come. Whether they are liquidating a family business, managing a diverse stock portfolio, or mentoring the next generation of investors, the 1945 cohort remains a cornerstone of the global financial system.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.