In an increasingly digital world, the concept of exchanging money has undergone a profound transformation. Gone are the days when cash was king or checks were the primary method for settling debts between individuals. Today, a new lexicon has emerged, dominated by terms like “send me a Venmo” or “just Venmo me.” But beyond its ubiquitous presence in casual conversation, “what does Venmo mean” in the larger context of technology, digital finance, and our daily lives? At its core, Venmo means an innovative, social, and streamlined approach to peer-to-peer (P2P) payments, fundamentally reshaping how individuals interact with their money through the power of an intuitive mobile application.

Venmo is a mobile payment service owned by PayPal that allows users to transfer money to one another digitally. It simplifies the often cumbersome process of splitting bills, paying friends back, or settling small debts, turning it into a seamless, almost instantaneous transaction. More than just a utility, Venmo has carved out a unique identity through its integration of social networking features, transforming private financial exchanges into a somewhat public, shared experience. For many, it’s not just an app; it’s a verb, a cultural touchstone that signifies convenience, connection, and the ongoing evolution of digital technology in personal finance. This article delves into Venmo from a technological perspective, exploring its core functionalities, the innovations it brought to digital payments, its security measures, and its significant footprint in the tech landscape.

The Digital Evolution of Peer-to-Peer Payments

The shift from physical currency to digital transactions has been a gradual yet relentless march of technological progress. For centuries, the exchange of goods and services necessitated a tangible medium of exchange. The advent of credit cards and online banking introduced early forms of digital transactions, but these often lacked the immediacy and simplicity required for casual, everyday money transfers between individuals. Venmo emerged as a key player in bridging this gap, propelling P2P payments into the mainstream.

From Cash to Clicks: A Brief History of P2P

Before Venmo, P2P payments were either clunky or non-existent in a truly accessible form. Bank transfers often involved inconvenient routing numbers and account details, along with processing times that could stretch for days. Cash, while immediate, carried security risks and logistical hurdles, especially for remote transactions or splitting exact amounts. Early digital solutions existed, but none captured the public imagination quite like Venmo. The need for a simple, fast, and secure way to send money between friends became increasingly apparent as smartphones became ubiquitous and social interactions frequently involved shared expenses – from dinner tabs to concert tickets.

The technology behind P2P payments essentially involves a digital ledger system that records transfers between user accounts, often linked to bank accounts or debit cards. What distinguished Venmo from earlier iterations was not just the underlying technology, but its user-friendly interface and the innovative application of social media principles to what was traditionally a private affair. This combination proved revolutionary.

Venmo’s Genesis and Market Impact

Founded in 2009 by Andrew Kortina and Iqram Magdon-Ismail, Venmo initially started as a text message-based payment system before evolving into the smartphone app we know today. Its acquisition by Braintree in 2012, and subsequently by PayPal in 2013, provided the necessary infrastructure and backing to scale significantly. PayPal’s extensive experience in online payments and its robust security framework allowed Venmo to mature rapidly, gaining user trust and market share.

Venmo’s market impact has been profound. It democratized instant money transfers, making them accessible to anyone with a smartphone and a bank account. It tapped into a younger demographic, particularly millennials and Gen Z, who were already accustomed to digital interactions and social media. The app became a standard for splitting costs, whether for rent, groceries, or a night out. Its ease of use and low friction transformed how people handled their casual financial obligations, making it a critical piece of the modern digital toolkit and demonstrating the immense potential of well-executed mobile software in disrupting traditional financial services.

Venmo’s Core Technology and Functionality

To understand “what Venmo means” from a technology standpoint, one must delve into its operational mechanics and the features that define its user experience. Venmo is not merely a conduit for money; it’s a sophisticated application designed for ease of use, speed, and social interaction.

Seamless Transactions: How Venmo Works

At its heart, Venmo functions by facilitating direct transfers between user accounts. When a user sends money, Venmo debits the amount from their linked funding source (a bank account, debit card, or Venmo balance) and credits it to the recipient’s Venmo balance. The recipient can then choose to keep the money in their Venmo balance for future transactions, use it to make purchases with a Venmo Debit Card, or transfer it to their linked bank account. Most standard transfers to a bank account are free but take 1-3 business days, while an instant transfer incurs a small fee.

The technology behind this seamless operation involves:

- APIs (Application Programming Interfaces): Venmo leverages robust APIs to connect securely with various financial institutions, enabling users to link their bank accounts and debit/credit cards for funding transactions and cashing out.

- Cloud Infrastructure: Operating on scalable cloud platforms allows Venmo to handle millions of transactions daily, ensuring high availability and performance even during peak usage.

- Real-time Processing: The system is designed for near-instantaneous transaction processing, providing immediate confirmation to both sender and receiver, which is a key differentiator from traditional bank transfers.

- Mobile-First Design: The entire platform is optimized for mobile devices, with intuitive gestures and clear navigation, making complex financial operations feel simple and accessible.

Beyond Payments: Social Features and Enhanced User Experience

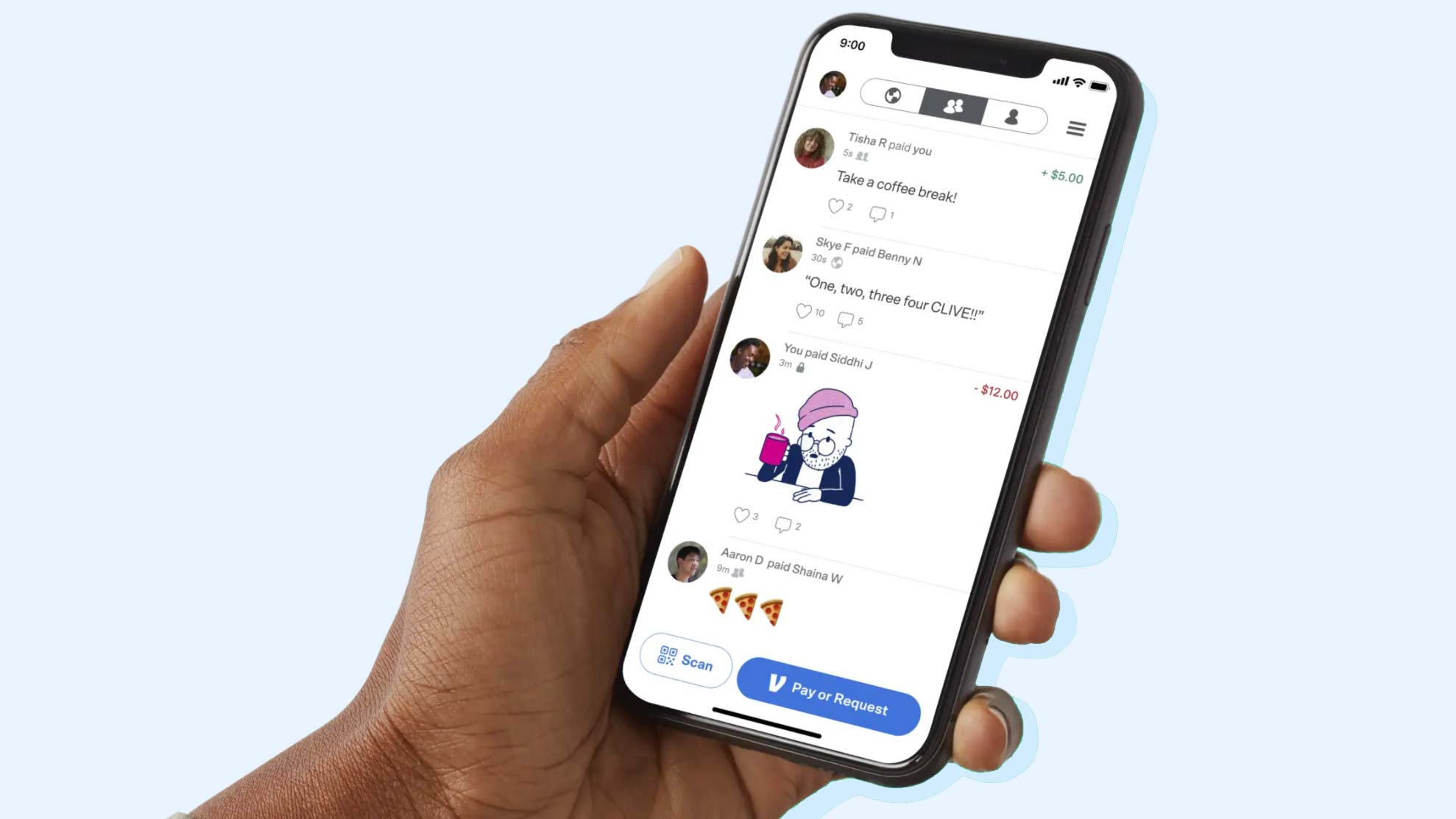

One of Venmo’s most distinctive and technologically interesting features is its social feed. Unlike traditional banking apps, Venmo encourages users to add notes, emojis, and even public or friends-only visibility settings to their transactions. This “social layer” was a groundbreaking innovation, transforming a typically private act into something shareable.

- Public/Private Feed: Users can choose to make their transactions public (visible to anyone on Venmo), visible only to friends, or entirely private. This feature created a unique dynamic, often leading to humorous or cryptic payment descriptions that became part of the app’s appeal.

- Emoji-Rich Descriptions: The ability to use emojis and informal language in transaction notes adds a playful, personal touch, reinforcing its social utility.

- Friends List Integration: Venmo integrates with a user’s phone contacts and social networks to easily find and connect with friends, simplifying the process of sending or requesting money.

This blend of financial utility with social media mechanics exemplifies clever technological design aimed at enhancing user engagement. It turned a mundane task into an interactive experience, fostering a sense of community around shared expenses.

Versatile Use Cases: Splitting, Requesting, and Business Profiles

Venmo’s technological framework supports a diverse range of use cases, making it incredibly versatile:

- Splitting Expenses: The app offers straightforward functionality to split a bill among multiple friends, automatically calculating individual shares and facilitating collection.

- Requesting Money: Users can easily send requests for money, which is particularly useful for reminding friends about shared costs or collecting overdue payments.

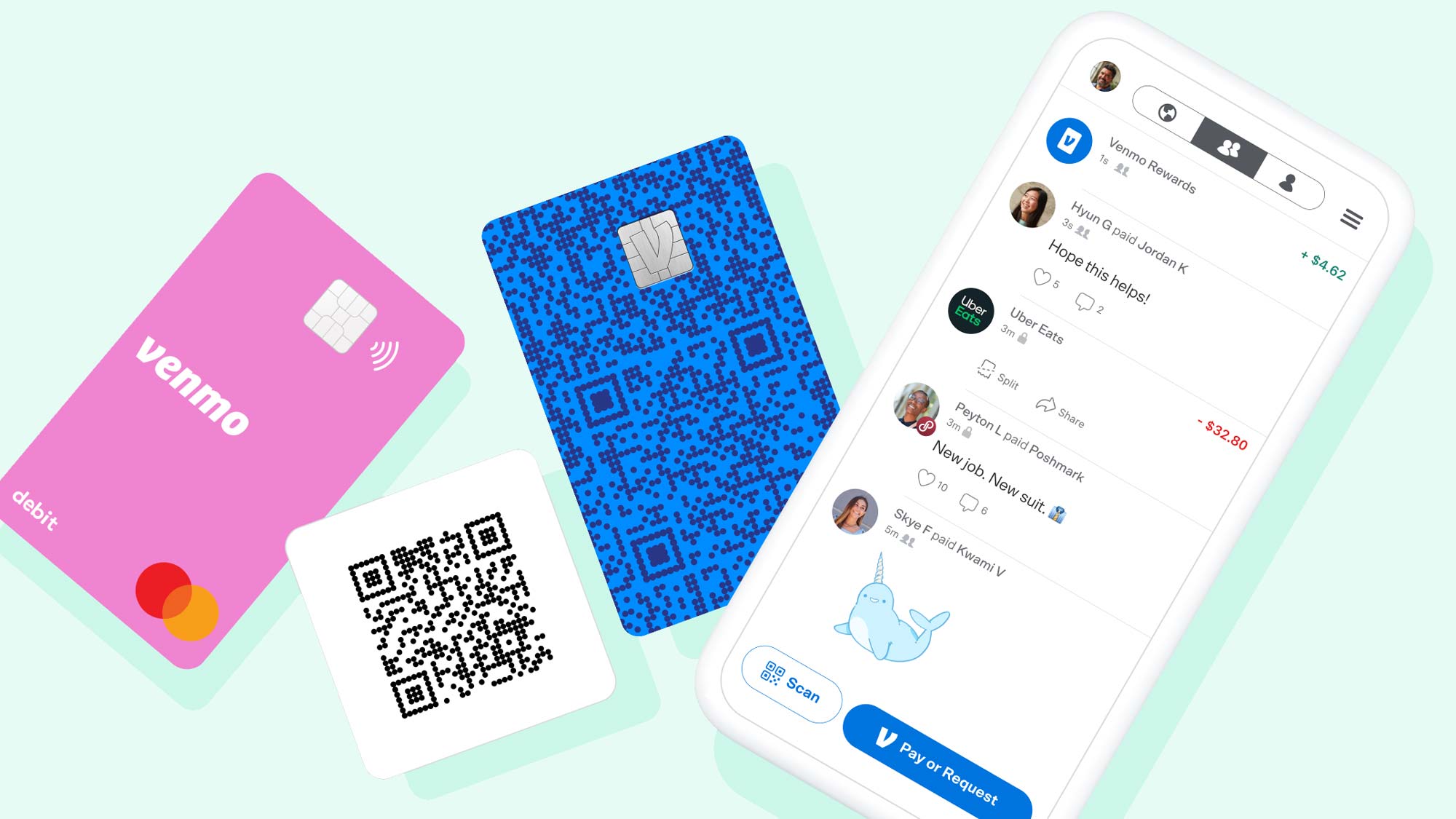

- Business Profiles: Recognizing its utility beyond P2P, Venmo has expanded to allow small businesses and freelancers to accept payments, introducing a layer of business-to-consumer (B2C) functionality built upon its P2P foundation. This often involves QR code payments, further simplifying transactions in physical settings.

- Venmo Debit Card and Credit Card: Extending its reach beyond just the app, Venmo offers a physical debit card, powered by Mastercard, allowing users to spend their Venmo balance anywhere debit cards are accepted. A Venmo Credit Card also integrates with the app, offering rewards on eligible purchases. These physical cards signify a technological expansion into traditional banking services while remaining rooted in the Venmo ecosystem.

These features, all underpinned by robust technological infrastructure, collectively define what Venmo means: a flexible, user-centric, and socially integrated payment solution.

Security and Trust in the Venmo Ecosystem

For any platform dealing with money, security is paramount. “What does Venmo mean” without trust in its ability to protect user funds and data? Venmo, as a critical financial tool, employs a multi-layered security approach, continuously evolving to combat sophisticated cyber threats and ensure user confidence.

Protecting Your Digital Wallet: Encryption and Authentication

Venmo utilizes industry-standard encryption protocols to safeguard all transactions and personal data. When you send money, your information is encrypted both in transit and at rest, making it incredibly difficult for unauthorized parties to intercept or access.

- Data Encryption: All sensitive information, including financial details and transaction histories, is encrypted using advanced cryptographic methods.

- Secure Servers: Venmo’s data centers are protected by firewalls and other physical and electronic security measures, adhering to stringent industry compliance standards.

- Multi-Factor Authentication (MFA): Users can enable MFA, adding an extra layer of security by requiring a second form of verification (like a code sent to their phone) in addition to their password when logging in or making certain transactions.

- Session Monitoring: Venmo continuously monitors for suspicious activity, using algorithms to detect unusual login attempts or transaction patterns that might indicate fraud.

These technological safeguards are crucial in maintaining the integrity of the platform and protecting users from financial threats inherent in digital environments.

Understanding Transaction Limits and Fraud Prevention

Venmo implements various measures to prevent fraud and manage risk, including transaction limits. These limits vary based on account verification status and transaction types (e.g., P2P payments, purchases from authorized merchants, bank transfers).

- Identity Verification: To combat money laundering and fraud, Venmo requires users to verify their identity by providing personal information like their social security number, date of birth, and address. This KYC (Know Your Customer) process helps in securing accounts and adhering to financial regulations.

- Fraud Detection Systems: Sophisticated AI and machine learning algorithms are employed to analyze transaction data for patterns indicative of fraudulent activity. These systems can flag suspicious transactions in real-time and, if necessary, temporarily hold funds or freeze accounts to investigate.

- Unauthorized Transaction Protection: While Venmo aims to be secure, it also provides mechanisms for users to report unauthorized transactions, initiating investigations and potential reversals where applicable. However, it’s important to note that Venmo is designed for payments between trusted individuals, and transactions between strangers often carry higher risk.

User Responsibility in Maintaining Security

While Venmo deploys robust security technologies, user vigilance remains a critical component of overall security.

- Strong Passwords: Users are encouraged to create unique, strong passwords and update them regularly.

- Beware of Phishing: Users must be wary of phishing attempts via email or text messages that try to trick them into revealing login credentials or personal information.

- Trust Your Recipient: Venmo emphasizes that it’s designed for payments between friends and people you trust. Sending money to strangers for goods or services can carry risks, as Venmo generally does not offer purchase protection for such transactions, unlike its parent company PayPal.

- Regular Account Review: Checking transaction history regularly can help users spot unauthorized activity early.

Ultimately, Venmo means a technologically secure platform, but one where shared responsibility between the platform and its users is key to maintaining a safe and trustworthy digital payment environment.

Venmo’s Place in the Broader Tech Landscape

Venmo didn’t just innovate; it influenced. Its success propelled other companies to adopt similar P2P functionalities, and it continues to shape the trajectory of digital payments. Its presence profoundly impacts how financial technology (FinTech) evolves.

Integration with Other Platforms and Services

Venmo’s influence extends beyond its standalone app. It has become a standard payment option in various digital ecosystems:

- PayPal Integration: As a PayPal subsidiary, Venmo benefits from and integrates with PayPal’s vast network, leveraging its infrastructure and reach.

- Merchant Integration: Many online and in-app merchants now accept Venmo as a payment method, expanding its utility from P2P to B2C transactions. This allows users to pay for goods and services directly from their Venmo balance or linked funding sources, blurring the lines between a simple P2P app and a full-fledged digital wallet.

- Third-Party App Connectivity: Developers can integrate Venmo’s payment capabilities into their own applications, enabling seamless checkouts or in-app money transfers. This open approach allows Venmo to become an embedded service within a broader digital landscape.

These integrations highlight Venmo’s technological versatility and its strategic positioning as a fundamental payment rail in the digital economy.

The Future of Digital Payments: Venmo’s Role in Innovation

Venmo continues to evolve, pushing the boundaries of what a P2P payment app can be. Its commitment to innovation is evident in its continuous feature updates and expansions.

- Cryptocurrency Integration: Venmo has entered the cryptocurrency space, allowing users to buy, hold, and sell select cryptocurrencies directly within the app. This move positions Venmo at the forefront of digital asset adoption, reflecting broader trends in FinTech and blockchain technology.

- Augmented Reality (AR) Features: Experimentation with AR for features like sending money via AR “gifts” showcases a willingness to explore novel interactive payment experiences.

- Financial Wellness Tools: As part of the PayPal ecosystem, Venmo is likely to integrate more features related to budgeting, spending insights, and other financial wellness tools, moving beyond just transactions to provide a more holistic financial management experience.

- Global Expansion: While primarily US-focused, the long-term vision for Venmo might involve international expansion, leveraging PayPal’s global infrastructure to offer its distinctive service to a wider audience.

Competitors and the Evolving P2P Space

Venmo operates in a highly competitive market, facing challengers from various fronts:

- Bank-Backed Services: Zelle, directly integrated into many major US banking apps, offers instant transfers without a separate app, providing strong competition, particularly for those who prefer to keep their banking and payment services consolidated.

- Other Tech Giants: Apple Pay Cash, Google Pay, and Cash App (Square) all offer similar P2P functionalities, often bundled with broader digital wallet services, loyalty programs, and even investment features.

- Traditional Banks: Even traditional banks are enhancing their own digital transfer capabilities, albeit often without the social flair of Venmo.

The presence of robust competitors continually pushes Venmo to innovate and differentiate. Its unique social element and user-friendly interface have allowed it to maintain a strong brand identity and user loyalty amidst this fierce competition. This dynamic environment means that Venmo, as a technology, must constantly adapt and evolve to stay relevant and meaningful to its user base.

Conclusion

So, what does Venmo mean? From a technological perspective, Venmo means an innovative mobile application that redefined peer-to-peer payments by combining seamless transaction capabilities with a compelling social experience. It signifies the power of intuitive software design, robust security protocols, and strategic integration within the broader digital ecosystem to simplify and humanize financial interactions. It means instant gratification for settling debts, a digital ledger of shared experiences, and a secure platform for managing everyday money.

Venmo’s impact transcends mere functionality; it represents a cultural shift towards digital fluency in personal finance, especially among younger generations. As technology continues to advance, and as our lives become increasingly interconnected through digital platforms, Venmo stands as a testament to how innovative apps can fundamentally change behavior, expectations, and the very meaning of exchanging value in the 21st century. It is not just an app for sending money; it is a dynamic digital tool that continues to shape the future of how we interact with our finances and each other.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.