In the intricate world of personal finance and investing, few concepts hold as much transformative power as compound interest. Often lauded as the “eighth wonder of the world” by Albert Einstein, its implications stretch far beyond mere mathematical calculations, influencing everything from the growth of your savings to the burden of your debt. Yet, despite its profound impact, many people only have a superficial understanding of what compound interest truly is and how it can be harnessed to build significant wealth over time.

At its heart, compound interest is simply the interest you earn not only on your initial principal but also on the accumulated interest from previous periods. It’s a process where your money starts to make money, and then that new money starts to make even more money, creating an accelerating cycle of growth. This seemingly straightforward idea forms the bedrock of long-term financial success, differentiating those who merely save from those who strategically invest for a prosperous future. Understanding this principle is not just an academic exercise; it’s a critical step toward taking control of your financial destiny and unlocking the potential for exponential growth in your investments.

The Core Concept: Interest on Interest

To fully grasp the magnitude of compound interest, it’s essential to first distinguish it from its simpler counterpart and then delve into the mechanics of how it operates. This fundamental understanding is the gateway to appreciating its transformative power.

Simple Interest vs. Compound Interest: A Fundamental Distinction

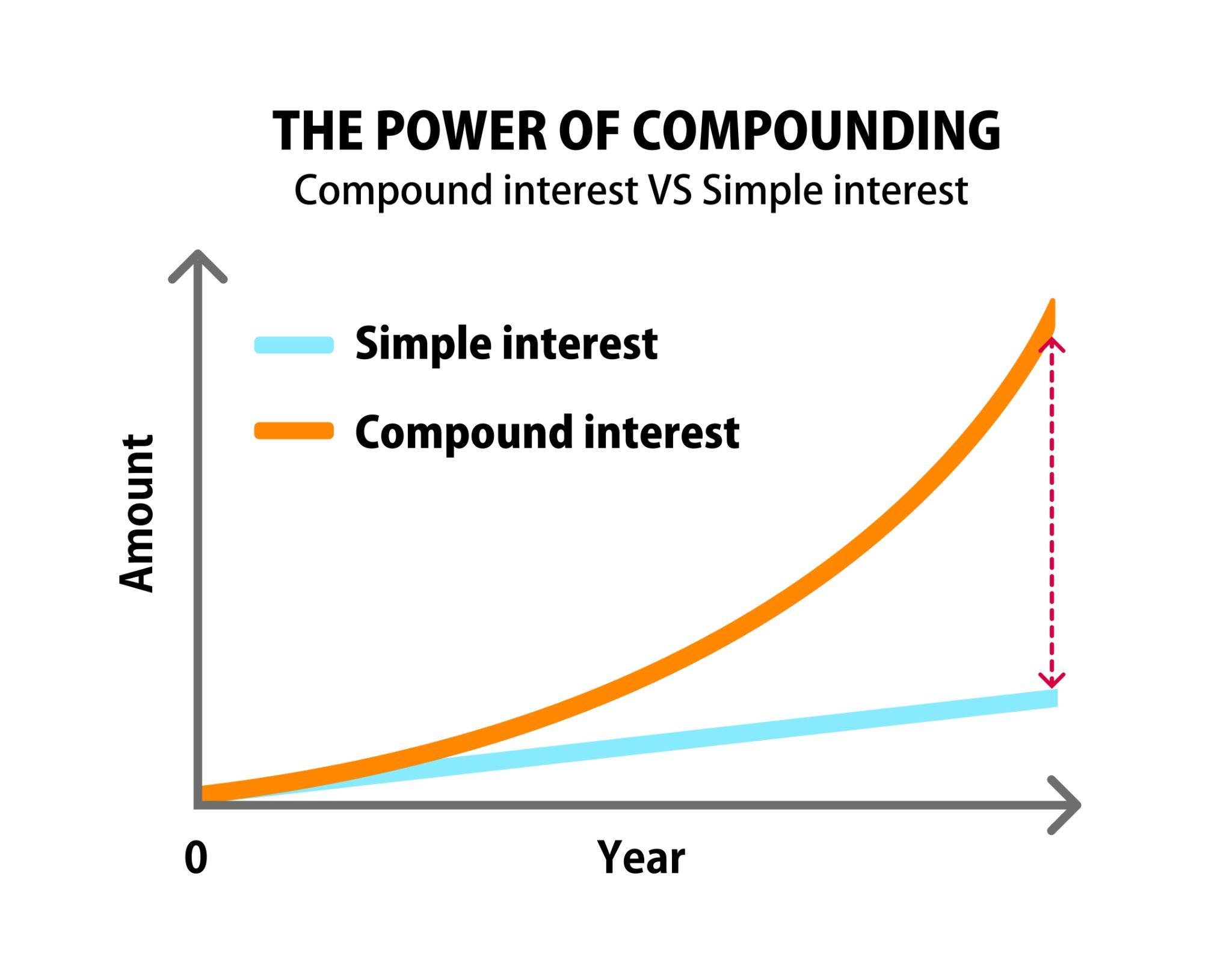

Imagine you lend money to someone, or you deposit money into a bank account. You expect to earn interest on that money. The most basic form of this earning is simple interest. Simple interest is calculated only on the initial principal amount. For example, if you invest $1,000 at a 5% simple interest rate per year, you would earn $50 each year, regardless of how many years pass. The principal amount remains the same for the calculation. After five years, you would have earned $250 in interest, bringing your total to $1,250.

Compound interest, on the other hand, is a more dynamic force. It calculates interest not only on your initial principal but also on the accumulated interest from preceding periods. Using the same example, if you invest $1,000 at a 5% annual compound interest rate:

- Year 1: You earn 5% of $1,000 = $50. Your new balance is $1,050.

- Year 2: You earn 5% of $1,050 (the original principal plus the first year’s interest) = $52.50. Your new balance is $1,102.50.

- Year 3: You earn 5% of $1,102.50 = $55.13. Your new balance is $1,157.63.

Notice how the amount of interest earned grows each year, even though the interest rate remains constant. This is the “interest on interest” effect in action, and it’s what sets compound interest apart as a far more powerful engine for wealth creation.

How Compounding Works: A Step-by-Step Breakdown

The process of compounding can be broken down into a series of iterative steps:

- Initial Investment (Principal): You start with a principal sum of money.

- Interest Calculation: At the end of a specific period (e.g., annually, semi-annually, quarterly, monthly, or even daily), interest is calculated on your current balance. This balance includes your original principal plus any previously accumulated interest.

- Reinvestment/Accumulation: The calculated interest is then added back to your principal. This new, larger sum becomes the base for the next period’s interest calculation.

- Repeat: This cycle repeats for every subsequent period. Each time, the principal grows, and therefore, the amount of interest earned also grows, creating an exponential curve of wealth accumulation.

This continuous cycle is often referred to as the “snowball effect.” Just as a small snowball rolling down a hill gathers more snow and grows larger and faster, your investments, fueled by compound interest, accumulate more money and accelerate their growth over time.

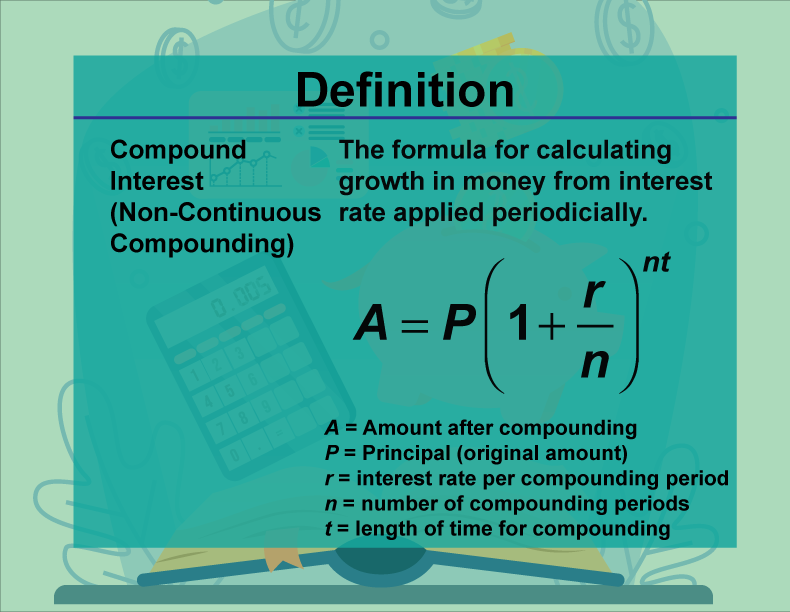

The Formula Behind the Magic

While you don’t need to be a mathematician to benefit from compound interest, understanding the basic formula can demystify its workings:

A = P (1 + r/n)^(nt)

Where:

- A = the future value of the investment/loan, including interest

- P = the principal investment amount (the initial deposit or loan amount)

- r = the annual interest rate (as a decimal)

- n = the number of times that interest is compounded per year

- t = the number of years the money is invested or borrowed for

This formula beautifully illustrates how the initial principal, interest rate, compounding frequency, and time all intertwine to determine the final accumulated amount. The exponent (nt) is particularly crucial, highlighting how both the duration of the investment and how often interest is calculated play a significant role in accelerating growth.

The Driving Forces of Compounding

While the “interest on interest” concept is fundamental, several key factors amplify or diminish its impact. Understanding these variables allows you to strategically optimize your financial decisions to harness compound interest most effectively.

Time: The Most Potent Ally

Without a doubt, time is the single most critical factor in the equation of compound interest. The longer your money has to grow, the more periods it undergoes compounding, and the more pronounced the snowball effect becomes. Even small, consistent investments made early in life can outperform much larger investments made later, simply because of the extended compounding runway. This phenomenon underscores the immense value of starting to save and invest as early as possible. Procrastination is the enemy of compounding, as every year lost is a year where your money could have been working exponentially harder for you.

Interest Rate: The Accelerant

The annual interest rate (r) acts as the accelerator of your compounding engine. A higher interest rate means a larger percentage of your growing principal is added back each period, leading to faster accumulation. While you can’t always control market rates, understanding the impact of even a percentage point difference can guide your investment choices. A 7% annual return will lead to significantly greater wealth over decades than a 5% annual return, even with the same initial investment and contributions.

Frequency of Compounding: More Frequent, More Powerful

The ‘n’ in our formula – the number of times interest is compounded per year – is often overlooked but plays a vital role. Interest can be compounded annually, semi-annually, quarterly, monthly, or even daily. The more frequently interest is compounded, the faster your money grows. For instance, an account that compounds monthly will generally yield slightly more than an account with the same annual interest rate that compounds only annually, because the interest starts earning interest sooner. While the difference might seem marginal in the short term, over long periods, it adds up.

Initial Principal and Additional Contributions: Fueling the Fire

While time and interest rate are external factors largely dictated by the market and your age, your initial principal (P) and any subsequent regular contributions are entirely within your control. The larger the starting sum, the larger the base for compounding. More importantly, consistent additional contributions act like continually pushing the snowball, giving it more material to grow with. Regular investments, even modest ones, consistently increase your principal, thereby magnifying the effect of compounding over time. This is why financial advisors often emphasize the importance of consistent saving and investing, rather than trying to time the market with a single large sum.

Why Compound Interest is a Game-Changer for Your Finances

The theoretical understanding of compound interest translates directly into practical benefits that can fundamentally alter your financial trajectory. It’s not just an abstract concept; it’s a tangible tool for wealth creation and financial security.

Accelerating Wealth Accumulation

The most obvious benefit of compound interest is its ability to accelerate wealth accumulation. Unlike simple interest, where growth is linear, compound interest leads to exponential growth. This means that your wealth grows slowly at first, but then picks up speed, increasing dramatically in later years. This characteristic is why diligent savers and investors often see the majority of their wealth growth occur in the latter half of their investing journey. It’s a testament to patience and persistence.

Battling Inflation Effectively

Inflation, the silent thief of purchasing power, erodes the value of your money over time. If your money isn’t growing at least at the rate of inflation, you’re effectively losing money. Compound interest provides a powerful defense against inflation. By ensuring your investments grow exponentially, it helps your money not only keep pace with rising costs but ideally, outpace them, thereby preserving and enhancing your future purchasing power.

The Power of Early Investment: The “Snowball Effect”

As discussed, time is paramount. Starting to invest early, even with small amounts, allows the snowball effect to work its magic over a longer duration. Consider two individuals: one who invests $5,000 a year from age 25 to 35 (10 years, total $50,000 invested) and then stops, and another who starts investing $5,000 a year from age 35 to 65 (30 years, total $150,000 invested). Assuming an identical 7% annual return, the early investor, despite investing less overall, will likely have significantly more money at age 65 due to the extra decade of compounding. This illustrates why the “time in the market” often beats “timing the market.”

Understanding Debt: The Dark Side of Compounding

While compound interest is a boon for investors, it can be a crushing burden for borrowers. The same principle that helps your savings grow exponentially can make your debts, such as credit card balances or high-interest loans, spiral out of control. When you carry a balance on a credit card, interest is compounded on your original purchase plus any accumulated interest. This is why high-interest debt can be so challenging to escape and why aggressively paying it off is often a top financial priority. Understanding compound interest illuminates the urgency of avoiding and eliminating costly debt.

Practical Applications and Strategies for Harnessing Compounding

Knowing what compound interest is and why it’s powerful is only half the battle. The other half involves actively implementing strategies to leverage it in your personal finance journey.

Retirement Planning: IRAs, 401(k)s, and Beyond

Retirement accounts like 401(k)s, IRAs (Traditional and Roth), and other employer-sponsored plans are prime vehicles for harnessing compound interest. These accounts often offer tax advantages, allowing your investments to grow untouched by annual taxes, further accelerating the compounding process. Maximize contributions, especially if your employer offers a matching program, as this is essentially free money compounding for you.

Savings Accounts and Certificates of Deposit (CDs)

For shorter-term goals or emergency funds, high-yield savings accounts and Certificates of Deposit (CDs) can also provide compound interest. While their rates are typically lower than market-linked investments, they offer security and allow your money to grow more than in a standard checking account. Ensure you choose accounts with competitive interest rates and understand their compounding frequency.

Investment Portfolios: Stocks, Bonds, and Mutual Funds

The stock market, through investments in individual stocks, bonds, mutual funds, or Exchange-Traded Funds (ETFs), offers the potential for higher returns, thus maximizing the interest rate factor in compounding. When you invest in dividend-paying stocks or bond funds, the earnings can be reinvested, purchasing more shares and further amplifying the compounding effect. Diversification across various asset classes is crucial to manage risk while pursuing growth.

Reinvesting Dividends and Earnings

A simple yet powerful strategy is to always opt for reinvesting dividends from stocks or mutual funds. Instead of receiving cash payouts, the dividends are used to buy additional shares of the same investment. This directly increases your principal, allowing more shares to earn dividends, and creating a continuous positive feedback loop of compounding growth. The same applies to interest earned on bonds or other fixed-income investments.

Automating Your Investments

Consistency is key to leveraging compound interest, and automation is the easiest way to achieve it. Set up automatic transfers from your checking account to your investment or savings accounts. Whether it’s bi-weekly or monthly, this “set it and forget it” approach ensures you consistently fuel your compounding engine, even during busy periods or when temptation to spend arises.

Common Misconceptions and Important Considerations

While compound interest is a powerful ally, a few common misunderstandings and considerations can impact its effectiveness.

It’s Not Just for the Wealthy

A pervasive myth is that compound interest is only relevant or beneficial for those with significant wealth. This couldn’t be further from the truth. The power of compounding is accessible to everyone, regardless of their starting capital. As demonstrated by the early investor example, consistent, modest contributions made over a long period can lead to substantial wealth, proving that even small amounts, given enough time, can grow into considerable sums.

Patience is Key: Avoid Short-Term Thinking

Compounding is a long-term game. The most dramatic growth often occurs in the later stages of an investment’s life. Expecting quick riches from compound interest is a misconception that can lead to disappointment and premature withdrawals. True wealth building through compounding requires patience, discipline, and the ability to ride out market fluctuations without panic.

The Impact of Fees and Taxes

While compound interest can accelerate growth, investment fees and taxes can slow it down. High management fees, transaction costs, and annual taxes on investment gains or income effectively reduce your principal amount available for compounding. Opt for low-cost index funds or ETFs where appropriate, and utilize tax-advantaged accounts like 401(k)s and IRAs to maximize your net returns and allow more of your money to compound.

Diversification and Risk Management

No discussion of investing, even one focused on compound interest, is complete without mentioning diversification and risk. While compounding fuels growth, the underlying investments still carry risk. Diversifying your portfolio across different asset classes, industries, and geographies helps mitigate specific risks and smooth out returns, providing a more stable base for compound interest to work its magic.

Conclusion

The term compound interest, at its essence, signifies the incredible phenomenon of earning “interest on interest.” It is a fundamental force in finance, capable of transforming modest savings into substantial wealth over time, provided it is given the necessary ingredients: time, a reasonable interest rate, and consistent contributions. Understanding and actively harnessing this principle is not merely a financial strategy; it is a profound insight into how money grows.

From accelerating wealth accumulation and battling inflation to the critical lessons it teaches about the perils of debt, compound interest is a concept every financially literate individual must master. By starting early, investing consistently, prioritizing higher-return vehicles (within your risk tolerance), and minimizing fees and taxes, you can effectively leverage this “eighth wonder” to build a secure and prosperous financial future. Embrace the power of compounding, and watch your financial destiny unfold exponentially.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.