For millions of Americans, the Social Security Administration (SSA) represents the bedrock of financial security. Whether it is a retired worker looking to maintain their lifestyle, a person with a disability seeking a lifeline, or a family grieving the loss of a breadwinner, the “payout” from the SSA is a critical component of personal finance. However, the system is notoriously complex, governed by a labyrinth of statutes, calculation formulas, and eligibility requirements. Understanding exactly what the SSA pays out—and how those figures are determined—is essential for any robust long-term financial plan.

In this guide, we will dissect the various categories of Social Security benefits, explore the mechanics of how payouts are calculated, and provide strategic insights into maximizing your lifetime earnings from the system.

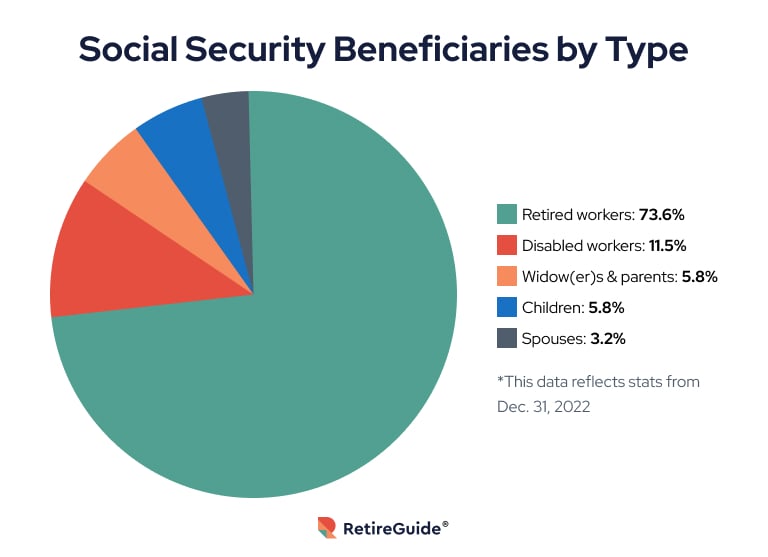

The Core Pillars of Social Security: What Benefits Are Available?

The SSA does not offer a “one size fits all” payment. Instead, it manages several distinct programs, each designed to address a specific financial risk. Broadly speaking, these are categorized into retirement, disability, survivors, and supplemental income.

Retirement Benefits: The Foundation of Post-Work Income

The most well-known SSA payout is the retirement benefit. This program is designed to replace a portion of a worker’s pre-retirement income based on their lifetime earnings. To qualify, an individual generally needs to accumulate 40 “credits,” which translates to roughly ten years of work in covered employment.

The amount paid out depends heavily on the age at which you claim. While the “Full Retirement Age” (FRA) is now 67 for those born in 1960 or later, individuals can claim as early as age 62. However, doing so results in a permanent reduction in the monthly payout. Conversely, delaying benefits until age 70 can significantly increase the monthly check through delayed retirement credits.

Disability Insurance (SSDI): Financial Protection for the Unexpected

Social Security Disability Insurance (SSDI) serves as a federal insurance policy for workers who become unable to work due to a severe, long-term medical condition. Unlike private disability insurance, the SSA’s criteria are strict; the disability must be expected to last at least 12 months or result in death, and it must prevent the individual from engaging in “substantial gainful activity.” The payout for SSDI is calculated similarly to retirement benefits, based on the worker’s average lifetime earnings before the disability began.

Survivors Benefits: Supporting Families in Times of Loss

When a worker who has paid into the Social Security system passes away, their family members may be eligible for survivors benefits. This is a crucial financial safety net for widows, widowers, and dependent children. For a surviving spouse, the payout can be as much as 100% of the deceased worker’s benefit amount, provided the survivor has reached full retirement age. Children under 18 (or 19 if still in high school) are also eligible for monthly payouts, helping to stabilize the household’s finances during a period of transition.

Supplemental Security Income (SSI): A Safety Net for the Most Vulnerable

While often confused with Social Security retirement or disability, Supplemental Security Income (SSI) is a separate program managed by the SSA. It is funded by general tax revenues rather than Social Security taxes. SSI provides monthly payouts to adults and children with disabilities, as well as seniors aged 65 and older, who have limited income and resources. The payout amounts for SSI are set at a federal level, though some states provide a supplemental payment to increase the total monthly benefit.

Decoding the Math: How the SSA Calculates Your Payout

The question of “how much will I get?” is answered through a sophisticated mathematical process that the SSA applies to every worker’s record. Understanding this formula allows for better financial forecasting and helps individuals identify gaps in their retirement savings.

The Role of Work Credits and Earning History

The journey to an SSA payout begins with your earnings record. Each year, the SSA tracks your “covered” earnings—income on which you paid Social Security taxes (FICA or SECA). To be eligible for benefits, you must earn “credits.” In 2024, you receive one credit for every $1,730 in earnings, up to a maximum of four credits per year. Once you reach 40 credits, you are “fully insured” for retirement benefits. However, the amount of your payout is not determined by these credits, but by the actual dollar amount of your earnings.

Average Indexed Monthly Earnings (AIME) and Primary Insurance Amount (PIA)

To calculate your monthly benefit, the SSA looks at your 35 highest-earning years. These earnings are “indexed” to account for inflation and changes in average wages over time. This ensures that $20,000 earned in 1990 is weighted appropriately against $60,000 earned in 2023.

The SSA then averages these 35 years of indexed earnings and divides the total by 420 (the number of months in 35 years) to arrive at your Average Indexed Monthly Earnings (AIME). From there, a formula is applied to determine your Primary Insurance Amount (PIA)—the base amount you would receive at your Full Retirement Age. The formula is progressive, meaning it replaces a higher percentage of income for lower-wage earners than for higher-wage earners.

The Impact of Retirement Age: Early Filing vs. Delayed Credits

Perhaps the most significant variable in the SSA payout equation is the timing of the claim.

- Early Filing (Age 62): Benefits are reduced by about 0.5% for every month you claim before your FRA. If your FRA is 67 and you claim at 62, your monthly payout is permanently reduced by 30%.

- Full Retirement Age (66 or 67): You receive 100% of your PIA.

- Delayed Filing (Up to Age 70): For every year you delay beyond your FRA, your benefit increases by 8%. By waiting until 70, you can receive 124% or more of your base benefit. This is one of the most effective ways to “guarantee” a higher return on your lifetime contributions.

Maximizing Your SSA Payout: Strategic Financial Planning

Social Security should not be viewed in a vacuum. It is a tool that must be integrated into a broader personal finance strategy. By understanding certain nuances, you can potentially increase the total “wealth” you extract from the system over your lifetime.

The Spousal Benefit Advantage

One of the most powerful features of the SSA payout system is the spousal benefit. Even if a spouse has never worked or has a very low earnings history, they can claim a benefit based on their partner’s work record. A spouse can receive up to 50% of the higher earner’s PIA. This is particularly beneficial for single-income households or families where one partner took time off for caregiving. It is important to note that claiming a spousal benefit does not reduce the primary worker’s own check.

Taxation of Benefits: How Much Will You Actually Keep?

Many retirees are surprised to find that their SSA payout is taxable. Whether you pay taxes on your benefits depends on your “combined income,” which the IRS defines as your adjusted gross income (AGI) + non-taxable interest + half of your Social Security benefits.

- If you are filing as an individual and your combined income is between $25,000 and $34,000, you may pay income tax on up to 50% of your benefits.

- If it exceeds $34,000, up to 85% of your benefits may be taxable.

Strategic withdrawals from Roth IRAs (which do not count toward AGI) can help keep your combined income lower, thereby preserving more of your SSA payout.

Understanding Cost-of-Living Adjustments (COLA)

Social Security is one of the few sources of retirement income that is indexed for inflation. Each year, the SSA evaluates the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). If prices have risen, the SSA issues a Cost-of-Living Adjustment (COLA) to ensure that the purchasing power of the payout does not erode. In years of high inflation, these adjustments can be significant, providing a vital hedge that private annuities or fixed pensions often lack.

The Future of Social Security: Sustainability and Personal Finance

No discussion of SSA payouts is complete without addressing the elephant in the room: the long-term solvency of the Social Security Trust Funds. As the “Baby Boomer” generation retires in record numbers, the ratio of workers to retirees is shrinking.

The Trust Fund Outlook and Potential Reforms

Current projections suggest that the Social Security Trust Funds may be depleted by the mid-2030s. However, “depletion” does not mean “bankruptcy.” Even if the trust funds are exhausted, tax revenue coming into the system is projected to cover roughly 75% to 80% of scheduled benefits. To close the gap, Congress may eventually consider reforms such as raising the payroll tax cap, increasing the full retirement age, or adjusting the benefit formula for high earners. From a personal finance perspective, it is wise to run retirement projections assuming a slightly lower SSA payout than currently promised, just to be conservative.

Integrating SSA Payouts into a Diversified Retirement Portfolio

Ultimately, the SSA payout is meant to be a foundation, not the entire house. Most financial planners suggest that Social Security should replace roughly 40% of your pre-retirement income. The remaining 60% must come from personal savings, such as 401(k)s, IRAs, and other investments.

By viewing the SSA payout as the “fixed income” or “bond” portion of your portfolio, you can afford to take more calculated risks with your other investments. This holistic approach ensures that you are not solely dependent on government policy, but rather empowered by a diversified financial structure.

The SSA payout remains a monumental achievement in social and financial engineering. By mastering the rules of eligibility, the mechanics of calculation, and the strategies for timing, you can transform Social Security from a mysterious monthly check into a powerful engine for long-term financial independence.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.