In the realm of personal finance and property ownership, the term “assessed value” frequently surfaces, often during discussions about property taxes, home insurance, or refinancing. While it’s a critical figure that impacts your financial obligations and investment, its precise meaning can sometimes be elusive. Understanding the assessed value is not just about demystifying jargon; it’s about grasping a fundamental element of your property’s financial standing and how it directly influences your financial well-being. This article aims to demystify the concept of assessed value, breaking down its components, its calculation, and its profound implications for homeowners and investors alike.

The Fundamentals of Assessed Value: More Than Just a Number

At its core, the assessed value of a property is a monetary figure assigned by a government entity, typically a local tax assessor’s office, for the purpose of calculating property taxes. It is not the same as market value, replacement cost, or insurance value, although it can be related to these. The assessed value is essentially a standardized benchmark used by municipalities to levy taxes and fund public services such as schools, infrastructure, and emergency services.

Differentiating Assessed Value from Market Value

The most common point of confusion arises when comparing assessed value to market value. Market value represents the price a willing buyer would pay and a willing seller would accept for a property in an open and competitive market. This value is dynamic, fluctuating with supply and demand, economic conditions, neighborhood desirability, and the specific features and condition of the property.

Assessed value, conversely, is a more static figure determined by specific, often standardized, methodologies. While market conditions can influence the assessment process over time, the assessed value is not directly tied to the most recent sale price of the property or its potential selling price on any given day. Assessors often use mass appraisal techniques, which analyze numerous properties in a geographic area using statistical models to estimate values. This can lead to discrepancies between the assessed value and the actual market value. For instance, a property might have undergone significant renovations that increase its market value considerably, but if these improvements haven’t been officially reported and reassessed, the assessed value might lag behind. Conversely, a property in a declining market might have an assessed value higher than what it could realistically sell for.

The Role of the Tax Assessor and Assessment Ratio

The tax assessor’s office is the primary body responsible for determining the assessed value. Their job involves valuing all taxable property within their jurisdiction. To do this, they often employ various appraisal methods, including:

- The Sales Comparison Approach: This method analyzes recent sales of comparable properties in the area.

- The Cost Approach: This method estimates the cost to replace the property, minus depreciation.

- The Income Approach: This method is typically used for income-generating properties and estimates value based on the potential rental income.

Once a property’s value is estimated, an assessment ratio is often applied. This ratio, determined by state or local law, dictates what percentage of the property’s estimated value is actually used for tax calculation. For example, if a property has an estimated market value of $300,000 and the assessment ratio is 50%, its assessed value would be $150,000. This ratio ensures that the property tax burden is distributed equitably, especially in jurisdictions where only a portion of the property’s value is subject to taxation. Understanding the assessment ratio is crucial, as it directly impacts the tax bill.

Why is Assessed Value Important?

The assessed value is paramount for several reasons, primarily revolving around financial obligations and investment considerations:

- Property Taxes: This is the most direct and impactful consequence of the assessed value. Property taxes are levied based on the assessed value of your property. A higher assessed value generally translates to higher property tax payments. These taxes are a recurring expense that homeowners must budget for annually.

- Property Insurance: While not always the primary factor, the assessed value can influence the premiums you pay for homeowners insurance. Insurers may consider it as one of the metrics to gauge the risk and potential payout in case of damage or loss. However, it’s more common for insurance to be based on replacement cost, which is the cost to rebuild the property from scratch.

- Refinancing and Home Equity Loans: When you apply for a mortgage refinance or a home equity loan, lenders will assess the value of your property. While they will often conduct their own appraisal, the assessed value can sometimes be a preliminary indicator of the property’s worth and the lender’s potential loan-to-value ratio.

- Estate Planning and Inheritance: Upon the death of a property owner, the assessed value might be used as a starting point for determining the property’s value for estate tax purposes or for distributing assets to heirs.

Calculating Your Property’s Assessed Value: The Process and Its Components

Understanding how your property’s assessed value is determined can empower you to challenge it if you believe it’s inaccurate and to better anticipate your financial responsibilities. The process involves several key steps and considerations, often influenced by local regulations and appraisal methodologies.

The Assessment Cycle and Reappraisals

Most jurisdictions conduct property assessments on a regular cycle, which can range from annually to every few years. This cycle ensures that property values are periodically updated to reflect changes in the real estate market and physical condition of properties. During a reappraisal year, assessors will revisit properties to update their valuations. This might involve:

- Physical Inspections: In some cases, assessors may conduct physical inspections of properties to note any changes, such as new additions, renovations, or deterioration.

- Data Collection: They will gather data on recent sales of comparable properties, construction costs, rental income (for investment properties), and neighborhood trends.

- Mass Appraisal Techniques: As mentioned earlier, sophisticated computer models and statistical analysis are often employed to appraise large numbers of properties efficiently. These models take into account various characteristics of a property, such as its size, age, number of rooms, lot size, and location.

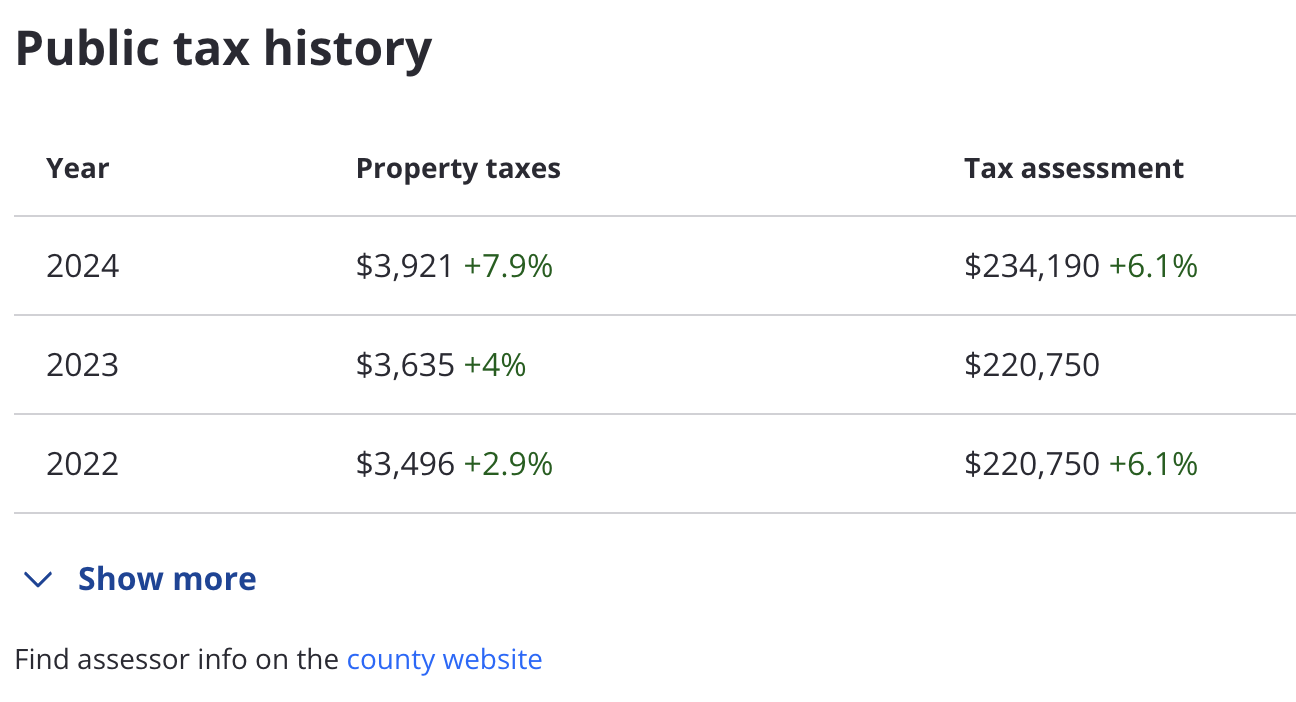

The frequency of reappraisals can vary significantly by state and even by county. Some areas may have annual reassessments, while others might only do so every five or ten years. The longer the period between reassessments, the greater the potential for a significant divergence between the assessed value and the current market value.

Factors Influencing Assessed Value

Several factors are taken into account when determining a property’s assessed value. While the specific criteria can differ, common elements include:

- Location: Properties in desirable neighborhoods with good schools, amenities, and low crime rates generally command higher values.

- Size and Square Footage: The overall living area of the home is a primary determinant of its value.

- Age and Condition: Newer homes and those in excellent condition are typically valued higher than older, dilapidated properties. Depreciation is a significant factor in the cost approach to appraisal.

- Number of Rooms and Bathrooms: The functionality and number of living spaces, including bedrooms and bathrooms, contribute to the assessed value.

- Lot Size and Features: The size of the land parcel and any desirable features like a well-maintained garden, swimming pool, or desirable view can influence value.

- Amenities and Upgrades: Features such as updated kitchens and bathrooms, high-end finishes, energy-efficient systems, or finished basements can increase a property’s assessed value.

- Zoning and Land Use: The permitted use of the land (e.g., residential, commercial) and any restrictions can impact its value.

- Recent Sales of Comparable Properties (Comps): As mentioned, the sales comparison approach is a widely used method, making recent sales of similar homes in the vicinity a significant factor.

The Assessment Ratio and its Impact

The assessment ratio is a crucial element that links the estimated market value of a property to its assessed value. It’s the percentage of the property’s true value that is subject to taxation. For example:

- If a property is estimated to be worth $400,000 and the assessment ratio is 25%, the assessed value is $100,000 ($400,000 x 0.25).

- If another jurisdiction has an assessment ratio of 100%, the assessed value would be $400,000 for the same property.

It’s important to note that a lower assessment ratio does not necessarily mean lower property taxes. The tax rate (millage rate) is applied to the assessed value. So, a property with a low assessed value but a high tax rate could end up paying more in taxes than a property with a high assessed value and a low tax rate. The key is to look at the effective tax rate, which is the total property tax paid divided by the property’s market value.

Challenging Your Assessed Value: A Homeowner’s Right

If you believe your property’s assessed value is inaccurate, you have the right to challenge it. This process, often referred to as an appeal or grievance, can potentially lead to a reduction in your property tax bill. It’s a crucial step for homeowners who feel their property has been overvalued.

When to Consider an Appeal

Several scenarios might prompt a homeowner to consider appealing their assessed value:

- Discrepancy with Market Value: If your assessed value is significantly higher than what comparable properties in your neighborhood have recently sold for, or what your own independent appraisal suggests, it’s a strong reason to appeal.

- Errors in Property Information: The assessor’s records might contain factual errors about your property, such as incorrect square footage, number of rooms, or missing features that reduce its value.

- Physical Deterioration or Damage: If your property has suffered significant damage (e.g., from a natural disaster) or has serious structural issues that haven’t been reflected in the assessment, an appeal is warranted.

- Changes in Neighborhood Value: If the overall market value of properties in your neighborhood has declined since the last assessment, and your assessed value hasn’t been adjusted accordingly, you may have grounds for appeal.

- Inconsistent Assessments: If you notice that your property is assessed at a higher ratio of its market value compared to similar properties in your area, this could indicate an inequity.

The Appeal Process: Steps and Strategies

The appeal process varies by jurisdiction, but generally involves the following steps:

- Review the Assessment Notice: Carefully examine your official property assessment notice. This document will detail the assessed value, the assessment ratio, and the valuation methods used.

- Gather Evidence: This is the most critical part of your appeal. Collect as much supporting documentation as possible:

- Recent Sales Data: Printouts of recent sales of comparable properties from real estate websites. Focus on properties that are similar in size, age, condition, and location to yours.

- Independent Appraisal: Obtain a professional appraisal of your property from a licensed appraiser. This provides an objective valuation.

- Photographs: Document any damage, deterioration, or outdated features of your property that negatively impact its value.

- Proof of Errors: Provide evidence if there are factual errors in the assessor’s records (e.g., incorrect blueprints, permits for unbuilt additions).

- Contractor Estimates: If your property requires significant repairs, get estimates from contractors to quantify the cost.

- File an Informal Review or Complaint: Most jurisdictions offer an informal review process where you can discuss your concerns directly with the assessor’s office. This might resolve the issue without further escalation. If not, you’ll typically need to file a formal appeal or grievance.

- Attend the Formal Hearing: If your informal review is unsuccessful, you will likely have a hearing before a local board of review or tax appeals tribunal. Be prepared to present your evidence clearly and concisely. You may want to research how previous appeals have been decided in your area.

- State or County-Level Appeals: If you are unsuccessful at the local level, you may have the option to appeal to a higher state or county board.

It’s crucial to be aware of the deadlines for filing appeals, as missing them will forfeit your right to challenge the assessment for that tax year.

The Benefits of a Successful Appeal

A successful appeal can result in significant financial benefits for homeowners. A reduction in the assessed value directly lowers the base upon which property taxes are calculated. Over time, this can lead to substantial savings. For instance, a reduction of $20,000 in assessed value, with a local tax rate of 2%, could save the homeowner $400 annually. Over a decade, that’s a $4,000 saving. Beyond tax savings, a lower assessed value can also positively impact your property’s perceived value and potentially improve your borrowing capacity for future financial endeavors, such as refinancing or home equity loans.

Assessed Value in the Broader Financial Landscape: Insurance and Investment

While property taxes are the most immediate concern tied to assessed value, its influence extends to other crucial aspects of personal finance, particularly property insurance and investment considerations. Understanding these connections can provide a more holistic view of your property’s financial significance.

Assessed Value and Property Insurance

The relationship between assessed value and property insurance is often misunderstood. While an assessor determines the “assessed value” for tax purposes, insurance companies are primarily concerned with the replacement cost or reproduction cost of your home.

- Replacement Cost: This is the amount it would cost to rebuild your home today using similar materials and construction standards.

- Reproduction Cost: This is the cost to rebuild your home using the exact same materials and design as the original.

The assessed value is generally not the primary basis for determining your homeowners insurance premiums. Insurers will typically conduct their own valuation or use specialized software to estimate the replacement cost. However, there can be indirect links:

- Indicator of Value: The assessed value might serve as a rough indicator of a property’s overall value, which insurers may consider as one data point among many.

- Higher-Value Properties: Properties with higher assessed values are often larger, more elaborate, or located in more expensive areas, which can correlate with higher replacement costs and, consequently, higher insurance premiums.

- Underinsurance Risk: Relying solely on the assessed value to determine insurance coverage can lead to underinsurance. If the assessed value is significantly lower than the actual replacement cost, you might not have enough coverage to rebuild your home if it’s destroyed, leading to a substantial financial shortfall. It’s crucial to communicate with your insurance provider to ensure your policy adequately covers the replacement cost of your home.

Assessed Value as a Component of Investment Analysis

For real estate investors, the assessed value plays a more nuanced role. While market value and rental income are typically paramount, the assessed value can offer additional insights:

- Property Tax Burden: A high assessed value, especially in conjunction with a high tax rate, can significantly eat into an investment property’s net operating income, reducing its profitability. Investors must factor these ongoing tax costs into their financial projections.

- Indicator of Potential Market Value: In some cases, particularly in markets with consistent assessment practices, the assessed value might provide a baseline estimate of a property’s worth, especially if direct market comparables are scarce.

- Benchmarking for Appeals: As discussed, investors can challenge assessments if they believe they are higher than the property’s true market value, thereby reducing their tax burden and increasing their return on investment.

- Loan-to-Value Ratios: Lenders will assess an investment property’s value for financing purposes. While they will conduct their own appraisals, the assessed value might be considered as part of the overall property profile.

It’s essential for investors to remember that the assessed value is a tool used by government for taxation and may not always reflect the property’s true investment potential or market dynamics. A savvy investor will look beyond the assessed value and conduct thorough due diligence on market conditions, rental income potential, and the property’s physical condition.

In conclusion, the assessed value of a property is a multifaceted financial metric with direct implications for homeowners and investors. It is the foundation for property tax calculations, a factor that can influence insurance considerations, and a piece of the puzzle in investment analysis. By understanding how it’s determined, what influences it, and your rights to challenge it, you can better navigate your financial responsibilities and make more informed decisions about your property assets.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.