In the rapidly evolving landscape of personal finance, the way we manage, save, and share money has shifted from physical ledgers to intuitive digital interfaces. Among the leaders of this revolution is Cash App, a platform that has transcended its origins as a simple peer-to-peer (P2P) payment tool to become a multi-faceted financial ecosystem. One term that frequently surfaces in the context of digital budgeting and group expenses is the “pool.”

While the term can refer to specific legacy features or general financial strategies, understanding what it means to “pool” money on Cash App is essential for anyone looking to optimize their collective purchasing power. This guide explores the mechanics of collaborative finance within the app, the strategic benefits of shared funds, and the professional management of digital assets.

1. The Mechanics of Collaborative Finance: What “Pool” Signifies

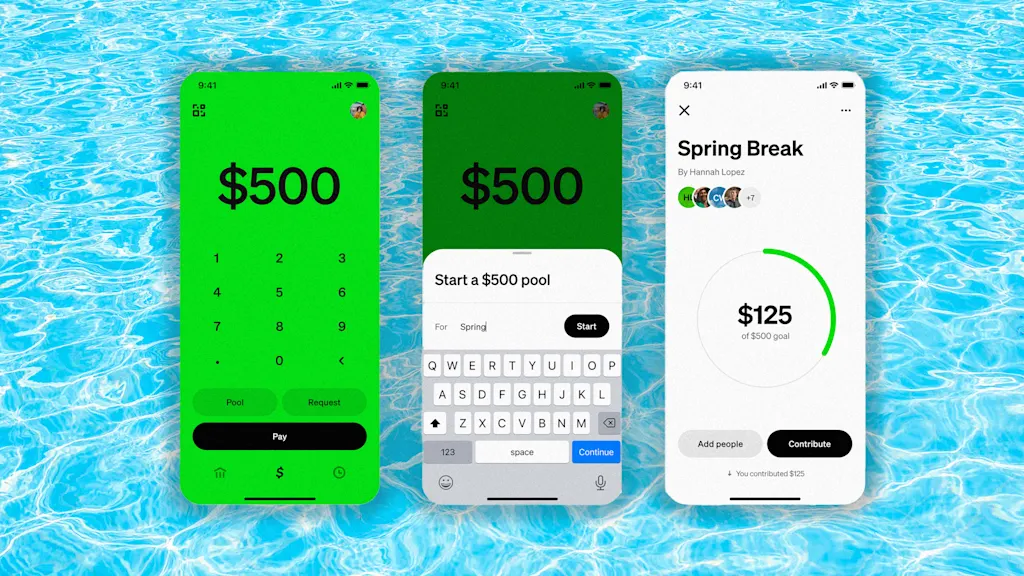

In the broader financial world, a “money pool” is a practice where a group of individuals contributes a set amount of capital into a central fund for a specific purpose. On Cash App, the concept of a “pool” traditionally referred to a specific feature designed to simplify group collections. Although the platform’s interface undergoes frequent updates, the core philosophy of pooling remains a cornerstone of its utility.

The Evolution of the Cash App Money Pool

Historically, Cash App introduced “Money Pools” as a direct way for users to collect funds for group gifts, trips, or shared bills without mixing those funds with their personal spending balance. While the specific “Pools” tab has been integrated into broader features like “Savings” and “Group Requests” in recent iterations, the term is still used colloquially by millions of users to describe the act of aggregating capital for a shared objective.

Digital Wallets as Centralized Nodes

To understand the “pool” in a modern context, one must view the Cash App balance as a centralized node. When you “pool” money today, you are essentially utilizing the platform’s high-velocity transfer capabilities to create a temporary or permanent reserve of capital. This is often managed by a “lead” user who acts as the informal treasurer, ensuring that the collective funds are allocated according to the group’s financial goals.

Transitioning from Social Payments to Financial Tools

The shift from simply “splitting a tab” to “pooling money” represents a transition in user behavior. Users are no longer just reacting to expenses; they are proactively gathering capital. This shift is a critical component of modern personal finance, allowing individuals with limited individual liquidity to participate in larger investment or purchasing opportunities through the power of the collective.

2. Strategic Applications of Pooling for Personal and Business Growth

Pooling money on Cash App isn’t just about convenience; it’s a strategic financial move. By aggregating resources, users can manage cash flow more effectively and leverage the platform’s features to achieve specific financial milestones.

Managing Shared Household Expenses

For roommates or couples, pooling money on Cash App serves as a digital joint account without the bureaucratic hurdles of traditional banking. By designating a specific balance for rent, utilities, and groceries, users can maintain a clear audit trail of contributions. This level of transparency is vital for maintaining financial harmony and ensuring that recurring liabilities are met on time.

Capital Aggregation for Small Business and Side Hustles

Entrepreneurs often use the pooling concept to kickstart small ventures. If a group of creators is looking to purchase bulk inventory or software subscriptions, they can pool their “Seed Money” on Cash App. This allows for a singular point of purchase, making it easier to track business expenses for tax purposes. In this context, the pool acts as a micro-fund, providing the necessary liquidity to scale a side hustle without dipping into personal savings.

Collaborative Saving for High-Ticket Items

Cash App’s “Savings” feature has revolutionized the way people pool money for themselves and their future. By setting aside a portion of incoming transfers into a separate “Savings” bucket, users are essentially pooling their own resources over time. When combined with group contributions—such as a wedding fund or a travel pot—the app becomes a powerful tool for goal-oriented financial planning.

3. The Financial Governance of Pooled Funds

When dealing with collective capital, professional management and security are paramount. Pooling money involves a high degree of trust, and navigating the financial implications—such as taxes and transfer limits—requires a sophisticated understanding of the platform’s regulations.

Navigating IRS Regulations and Form 1099-K

One of the most critical aspects of pooling money on digital platforms is understanding the tax implications. As of recent IRS guidelines, third-party settlement organizations (including Cash App) may be required to report “goods and services” transactions that exceed certain thresholds. If you are pooling money for a business venture or a taxable event, it is essential to categorize these transfers correctly. Managing a pool as “personal” when it is actually “business” can lead to complications during tax season.

Security Protocols and Fraud Prevention

Digital pooling carries inherent risks. To manage funds professionally, users should leverage Cash App’s security features, such as Security Locks (requiring FaceID or a PIN for every transfer) and Two-Factor Authentication (2FA). When acting as the administrator of a pool, it is your responsibility to ensure that the funds are protected from unauthorized access. Furthermore, users should only participate in pools with verified contacts to avoid the “social engineering” scams that occasionally target P2P users.

Liquidity Management and Withdrawal Limits

Professional financial management requires an awareness of liquidity. Cash App imposes limits on how much can be sent and received within certain timeframes (weekly or monthly). If a pool is intended for a large purchase—such as a $5,000 group rental—the administrator must ensure their account is verified to handle that volume. Failure to account for these limits can result in “frozen” capital at a critical moment, highlighting the need for proactive financial planning.

4. Maximizing the Utility of the “Savings” and “Round-Up” Features

To truly master the concept of pooling on Cash App, one must look beyond simple transfers and utilize the automated tools that build capital over time. These features represent the “passive” side of money pooling.

The Power of “Round-Ups”

Cash App’s “Round-Ups” feature allows users to pool their own spare change. Every time a user makes a purchase with their Cash Card, the app rounds up the transaction to the nearest dollar and moves the difference into a dedicated savings or investment account (such as Bitcoin or Stocks). This is essentially a “micro-pool” created from the remnants of daily spending, which can grow into a significant financial cushion over several months.

Goal-Based Savings as a Private Pool

Within the app, the Savings balance functions as a private, protected pool of capital. Unlike the main “Cash” balance, which is easily accessible for daily transactions, the Savings pool requires an intentional move to spend. From a psychological perspective, this “siloing” of funds is a proven strategy in behavioral finance to reduce impulsive spending and increase long-term wealth accumulation.

Leveraging the Cash Card for Pooled Benefits

The Cash Card offers “Boosts”—instant discounts at various retailers. When managing a pool of money for a group event, a savvy administrator can use these Boosts to stretch the collective dollar further. For example, using a 10% grocery Boost when purchasing supplies for a group event effectively increases the pool’s value, showcasing how strategic platform usage can yield tangible financial dividends.

5. Alternatives and the Future of Collective Wealth Management

While Cash App is a premier tool for pooling, the financial landscape is vast. Understanding where Cash App fits compared to other fintech tools is essential for a well-rounded financial strategy.

Cash App vs. Traditional Escrow and Joint Accounts

For larger sums or long-term investments, traditional joint bank accounts or escrow services may offer more robust legal protections than a P2P app. However, Cash App wins on agility and ease of use. For modern consumers, the “pool” on Cash App represents the “Fast Money” lane—perfect for immediate, social, and flexible financial maneuvers that traditional institutions are too slow to accommodate.

The Rise of Decentralized Finance (DeFi) Pooling

Looking forward, the concept of the “pool” is expanding into the world of cryptocurrency and decentralized finance. Cash App’s integration of Bitcoin suggests a future where pooling might involve “liquidity pools” or “staking” directly within the app. For the forward-thinking investor, the current “Money Pool” is just the beginning of a shift toward more complex, automated, and globalized collective finance.

Conclusion: Mastering the Digital Pot

Ultimately, “pool” on Cash App is more than just a feature; it is a financial methodology. It represents the democratization of fund management, allowing individuals to aggregate capital with the tap of a screen. Whether you are saving for a collective goal, managing household expenses, or building a small business, mastering the art of the pool requires a blend of strategic planning, security awareness, and an understanding of the digital economy. By treating these digital funds with the same rigor as a traditional investment portfolio, users can turn a simple app feature into a powerful engine for financial growth.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.