In the landscape of personal finance, few things are as volatile or as potentially devastating to a budget as healthcare costs. While most individuals understand the concept of a monthly premium—the fixed cost of “owning” insurance—the true complexity of financial planning lies in the variable costs associated with actually using that insurance. At the heart of this complexity is the “out-of-pocket limit” (or out-of-pocket maximum).

This figure is perhaps the most critical number in your health insurance policy, serving as the ultimate “stop-loss” mechanism for your personal wealth. Understanding how it functions, what it covers, and how to plan for it is essential for anyone looking to maintain a robust financial profile while navigating the modern medical system.

What is an Out-of-Pocket Limit? The Foundation of Financial Protection

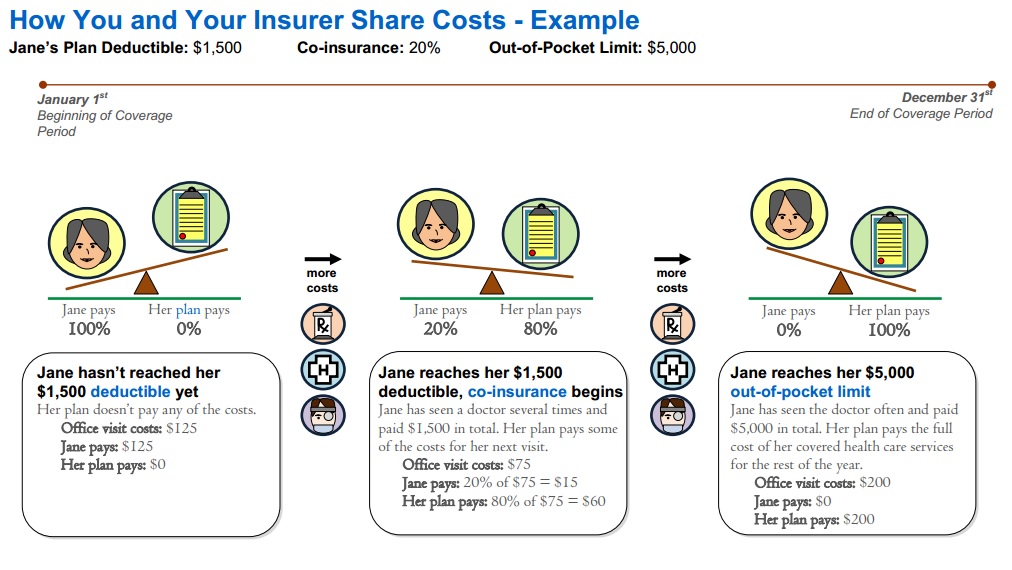

The out-of-pocket limit is the absolute maximum amount of money you will have to pay for covered medical services in a single plan year. Once you reach this threshold through your spending on deductibles, copayments, and coinsurance, your health insurance company assumes 100% of the costs for all covered “in-network” medical services for the remainder of the year.

From a financial planning perspective, the out-of-pocket limit represents your “worst-case scenario.” It is the ceiling on your liability, providing a predictable boundary for your medical expenses even in the event of a catastrophic illness or major surgery.

How It Differs from Premiums and Deductibles

To manage your money effectively, you must distinguish between the various components of an insurance plan.

- Premiums: These are your fixed monthly subscriptions. They do not count toward your out-of-pocket limit. Think of them as the cost of admission.

- Deductibles: This is the amount you pay out of pocket before your insurance starts sharing the cost (coinsurance). Every dollar spent on your deductible counts toward your out-of-pocket limit.

- Copayments and Coinsurance: These are your “cost-sharing” responsibilities after the deductible is met. These also count toward the limit.

The out-of-pocket limit is the culmination of your deductible and your cost-sharing payments. It is the final safety net that prevents medical expenses from spiraling into infinite debt.

The Legal Framework: The Affordable Care Act (ACA) Rules

Under the Affordable Care Act, there are federal mandates that limit how high an out-of-pocket maximum can be for “marketplace” and most private plans. For the 2024 plan year, the limit is capped at $9,450 for an individual and $18,900 for a family. These numbers are adjusted annually for inflation.

For a savvy investor or a household budgeter, knowing these caps allows for precise emergency fund planning. If you know the absolute maximum you could be forced to pay in a year is $9,450, you can structure your liquid savings to ensure that amount is accessible without liquidating long-term investments.

How the Out-of-Pocket Maximum Works in Practice

Understanding the theory is one thing; navigating the mechanics of a $50,000 hospital bill is another. The out-of-pocket limit functions as a progressive stage of payments. You start by paying the full cost of care until your deductible is met. Then, you enter the “coinsurance” phase, where you might pay 20% and the insurer pays 80%. This continues until your cumulative payments (deductible + 20% coinsurance) hit the out-of-pocket limit.

The Mathematics of Medical Billing

Imagine a scenario where an individual has a plan with a $2,000 deductible, a 20% coinsurance rate, and an $8,000 out-of-pocket limit. If they undergo a procedure costing $40,000:

- Deductible: They pay the first $2,000. Remaining balance: $38,000.

- Coinsurance: They owe 20% of $38,000, which is $7,600.

- The Limit Check: Adding the $2,000 deductible and $7,600 coinsurance equals $9,600.

- The Protection: Since the out-of-pocket limit is $8,000, the patient only pays $8,000. The insurance company covers the remaining $1,600 of the patient’s share, plus their own original 80% share.

Which Expenses Count Toward the Limit?

Not all medical spending moves you closer to your limit. Generally, the following contribute:

- Deductibles: The initial amount you pay for covered services.

- Copayments: Fixed fees for doctor visits or prescriptions.

- Coinsurance: Your percentage share of the cost for services.

It is vital to monitor your “Explanation of Benefits” (EOB) statements provided by your insurer. These documents track your progress toward your limit, allowing you to see exactly how much more you might owe in a calendar year.

What Doesn’t Count (Exclusions to Watch Out For)

This is where many people encounter financial friction. Certain costs never count toward your out-of-pocket limit:

- Monthly Premiums: These are never included.

- Out-of-Network Care: If you see a doctor who is not in your insurer’s network, the costs might not count toward your limit, and the insurer may not cap your liability at all.

- Balance Billing: If an out-of-network provider charges more than your insurer’s allowed amount, you may be billed for the difference.

- Non-Covered Services: Elective procedures (like most cosmetic surgeries) or therapies not deemed “medically necessary” do not count.

Strategic Financial Planning: Choosing the Right Limit for Your Budget

When selecting a health insurance plan during open enrollment, you are essentially making a high-stakes financial trade-off. Generally, plans with lower out-of-pocket limits have higher monthly premiums, while plans with high out-of-pocket limits offer lower premiums.

High Deductible Health Plans (HDHPs) vs. Low Deductible Plans

An HDHP often comes with a higher out-of-pocket limit. For a healthy individual with significant savings, this can be a strategic move. You save money on monthly premiums and only pay for healthcare if you actually use it. However, this requires the discipline to keep the full amount of the out-of-pocket limit in a liquid account.

Conversely, individuals with chronic conditions or those who expect frequent medical visits may find a “Gold” or “Platinum” plan more cost-effective. While the monthly premium is higher, the lower out-of-pocket limit provides a quicker path to 100% coverage, potentially saving thousands over the course of a year.

Health Savings Accounts (HSAs) as a Safety Net

If your plan has a high out-of-pocket limit, it often qualifies you for a Health Savings Account (HSA). In the realm of personal finance, the HSA is a “triple-tax-advantaged” powerhouse:

- Tax-Deductible Contributions: Money goes in pre-tax, lowering your taxable income.

- Tax-Free Growth: You can invest the funds in stocks or bonds, and the gains are not taxed.

- Tax-Free Withdrawals: As long as the money is used for qualified medical expenses (like reaching your out-of-pocket limit), it is never taxed.

Using an HSA to “self-insure” up to your out-of-pocket limit is one of the most effective ways to build long-term wealth while mitigating healthcare risk.

Impact on Personal Cash Flow and Long-Term Wealth

Medical debt remains the leading cause of bankruptcy in the United States. The out-of-pocket limit is the single most important tool in a financial arsenal to prevent this outcome. By understanding this limit, you transition from a reactive state of “medical bill anxiety” to a proactive state of “risk management.”

Avoiding Medical Debt and Bankruptcy

When you know your out-of-pocket limit, you can negotiate payment plans with hospitals more effectively. If you know you have reached your limit for the year, you can confidently undergo necessary screenings or procedures knowing that they will be “free” (fully covered) for the remainder of the calendar year. This “utilization window”—the period after you’ve hit your limit but before the plan resets on January 1st—is a critical time to address elective but necessary health concerns without further impacting your cash flow.

Factoring Insurance Into Your Emergency Fund

The traditional financial advice of keeping 3–6 months of expenses in an emergency fund is often insufficient if it doesn’t account for healthcare. A more sophisticated approach is to calculate your “Total Maximum Exposure.”

Total Maximum Exposure = (Annual Premiums) + (Individual/Family Out-of-Pocket Limit)

By ensuring your emergency fund can cover the out-of-pocket limit specifically, you protect your other assets—such as retirement accounts and home equity—from being liquidated to pay for medical crises.

In conclusion, the out-of-pocket limit is not merely a healthcare term; it is a fundamental pillar of personal finance. It provides the predictability needed to invest with confidence, knowing that a sudden health event will not result in unlimited financial liability. By mastering the mechanics of this limit and integrating it into your broader financial strategy, you secure both your health and your wealth.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.