For millions of people living across the globe, the term “NRI” is more than just a label of identity—it is a critical legal and financial classification that dictates how they manage wealth, pay taxes, and invest in one of the world’s fastest-growing economies. Standing for Non-Resident Indian, the NRI status is a bridge between an individual’s life abroad and their financial roots in India.

However, from a financial perspective, what does NRI mean in practical terms? It represents a shift in banking protocols, a different set of taxation rules, and a unique landscape of investment opportunities. Understanding this status is essential for anyone of Indian origin living overseas who wishes to maintain a robust financial footprint in their home country.

1. Decoding the NRI Status: Legal and Financial Frameworks

The definition of an NRI is not a singular concept; it is defined differently by two major Indian frameworks: the Foreign Exchange Management Act (FEMA) and the Income Tax Act. While one governs how you move money, the other governs how that money is taxed.

The 182-Day Rule: How Residency is Determined

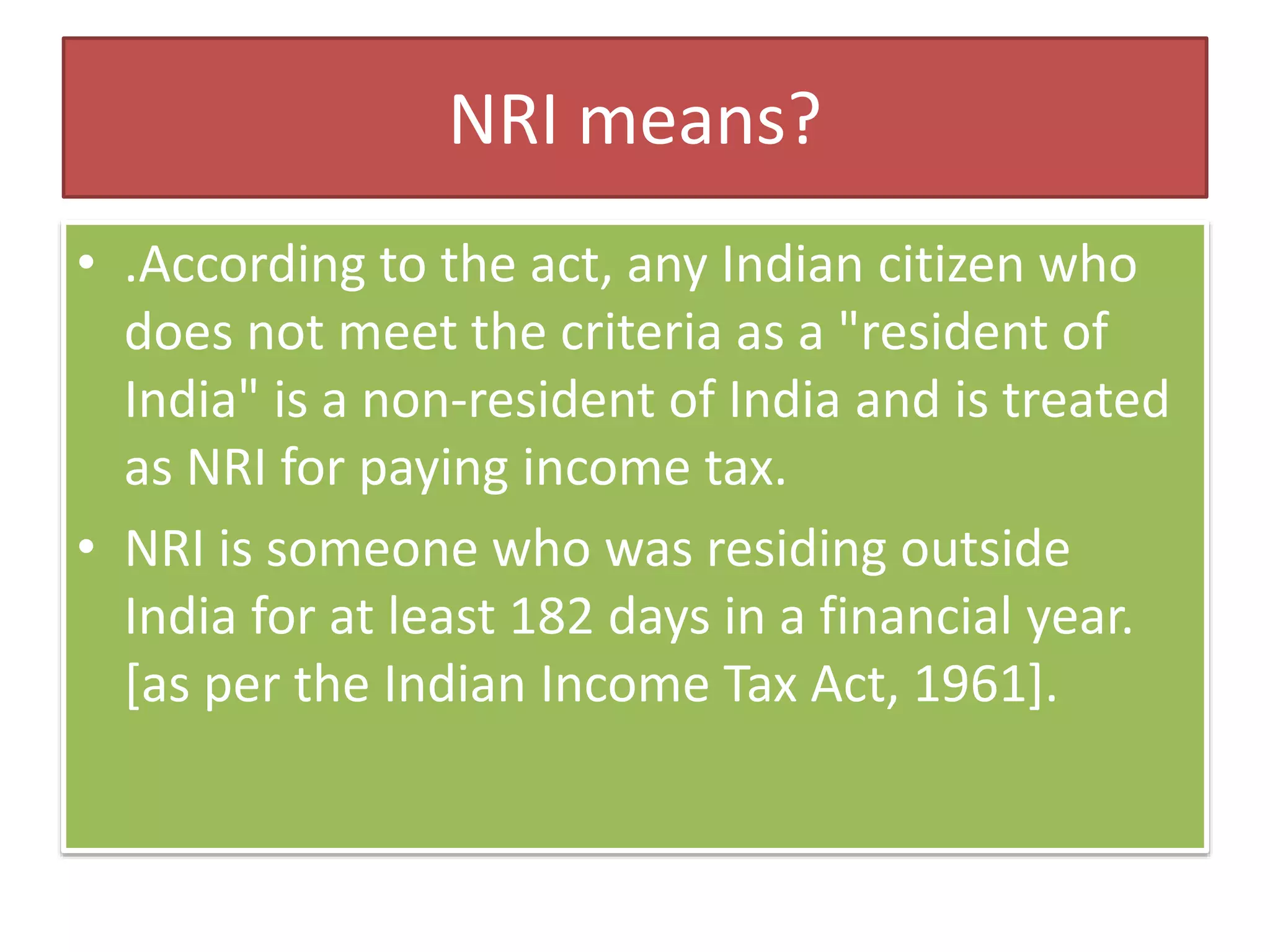

Under the Income Tax Act of 1961, your status as a “Resident” or “Non-Resident” is primarily determined by the number of days you spend in India during a financial year (April 1 to March 31). Generally, if an individual is in India for less than 182 days in a financial year, they are classified as a Non-Resident Indian for tax purposes.

Recent amendments have introduced nuances, such as the “120-day rule” for individuals with an Indian income exceeding ₹15 lakh, but the core principle remains: residency is a matter of physical presence and duration. For the global professional, tracking these days is the first step in financial compliance.

FEMA vs. Income Tax Act: Why the Distinction Matters

While the Tax Act looks at your past presence, FEMA looks at your “intent.” Under FEMA, you become an NRI the moment you leave India for the purpose of employment, carrying on a business, or any other purpose that indicates an indefinite stay abroad.

This distinction is crucial for your “Money” strategy. Once you are an NRI under FEMA, you are legally required to convert your existing resident savings accounts into NRO (Non-Resident Ordinary) accounts. Failing to do so can lead to penalties, making it imperative to understand the legal trigger points of your overseas move.

2. Banking Essentials for the Global Indian

Once the NRI status is established, the standard Indian savings account is no longer an option. The Indian banking system offers three specialized accounts designed to help NRIs manage foreign earnings and local income with ease.

NRE (Non-Resident External) Accounts: Tax-Free Repatriation

The NRE account is the gold standard for NRIs who want to send their foreign earnings back to India. These accounts are maintained in Indian Rupees (INR), but the funds originate from foreign currency.

The primary advantage of an NRE account is two-fold:

- Tax Exemption: The interest earned on an NRE savings account or fixed deposit is entirely tax-free in India.

- Full Repatriability: Both the principal amount and the interest can be freely moved back to your country of residence without any upper limit or complex paperwork. This makes it an ideal tool for liquidity management across borders.

NRO (Non-Resident Ordinary) Accounts: Managing Local Income

Many NRIs continue to earn income within India, such as rent from property, dividends from shares, or pension payments. This “Indian income” cannot be deposited into an NRE account; it must go into an NRO account.

Unlike the NRE, the interest earned on an NRO account is subject to Tax Deducted at Source (TDS) at a rate of 30% (plus applicable surcharges). Furthermore, there are limits on repatriation—usually up to USD 1 million per financial year—contingent upon the payment of applicable taxes. The NRO account serves as the primary gateway for managing one’s domestic financial obligations.

FCNR (Foreign Currency Non-Resident) Accounts: Hedging Against Volatility

For those who wish to keep their savings in foreign currency to avoid the risk of Rupee depreciation, the FCNR account is a strategic choice. You can hold deposits in major currencies like USD, GBP, EUR, or JPY. Like the NRE account, the interest is tax-free in India, and the funds are fully repatriable. This is an excellent tool for long-term wealth preservation for NRIs who plan to spend their future in a foreign currency environment.

3. Strategic Investment Opportunities for NRIs in India

India remains one of the most attractive investment destinations globally due to its demographic dividend and structural reforms. For an NRI, “Money” invested in India can often yield higher returns than traditional savings instruments in developed economies.

The Indian Stock Market and Portfolio Investment Schemes (PIS)

NRIs are permitted to invest directly in the Indian equity market through the Portfolio Investment Scheme (PIS). This allows them to buy and sell shares of Indian companies on the National Stock Exchange (NSE) and Bombay Stock Exchange (BSE).

While the process requires a PIS-enabled bank account, a Demat account, and a trading account, the long-term growth potential of Indian blue-chip companies and emerging mid-caps is a significant draw. For many NRIs, the stock market is a primary vehicle for capital appreciation.

Real Estate: Building Wealth through Physical Assets

Historically, real estate has been the preferred investment for the Indian diaspora. NRIs have a general permission from the Reserve Bank of India (RBI) to purchase residential and commercial properties in India.

The financial logic is simple: rental yields combined with capital appreciation. While NRIs cannot buy agricultural land, farmhouses, or plantation property (unless inherited), the residential sector offers significant tax benefits. For instance, the interest paid on a home loan for a property in India is deductible from the rental income, optimizing the tax outflow for the investor.

Mutual Funds and Digital Wealth Management Tools

For those who prefer a more passive approach, Indian Mutual Funds offer a diverse range of products, from aggressive equity funds to stable debt instruments. With the rise of fintech and digital wealth management platforms, NRIs can now manage their portfolios from their smartphones.

It is important to note that while most Mutual Funds are open to NRIs, those residing in the US and Canada may face certain restrictions due to FATCA (Foreign Account Tax Compliance Act) regulations. However, many leading Indian asset management companies have created compliant structures to accommodate these investors.

4. Navigating Taxation and Double Taxation Avoidance

Taxation is often the most complex aspect of the NRI status. A common misconception is that NRIs do not have to pay taxes in India. In reality, any income that “accrues or arises” in India is taxable.

Understanding TDS (Tax Deducted at Source) for NRIs

One of the most significant differences for an NRI is the higher rate of Tax Deducted at Source (TDS). Whether it is a fixed deposit, the sale of a property, or mutual fund redemptions, the Indian government mandates that tax be deducted at the highest slab (often 20% to 30%) at the time of the transaction.

While NRIs can file an Income Tax Return (ITR) to claim a refund if their total Indian income is below the taxable threshold, the initial deduction can impact cash flow. Strategic planning, such as applying for a “Lower Deduction Certificate,” can help manage this liquidity challenge.

Leveraging DTAA (Double Taxation Avoidance Agreement)

To prevent the same income from being taxed twice—once in India and once in the country of residence—India has signed Double Taxation Avoidance Agreements (DTAA) with over 80 countries, including the US, UK, UAE, Canada, and Australia.

By submitting a Tax Residency Certificate (TRC) from their current country of residence, an NRI can take advantage of the DTAA. This allows them to either pay a lower rate of tax in India or receive a credit for taxes paid in India against their tax liability in their home country. This is a vital tool for personal finance optimization that every NRI should utilize.

5. Future-Proofing Financial Goals: Retirement and Estate Planning

The ultimate “What does NRI mean?” question often finds its answer in the long-term vision. Is the stay abroad temporary, or is it a permanent relocation? This decision significantly impacts retirement and estate planning.

Planning for Return to India (RNOR Status)

For NRIs planning to move back to India, the transition period offers a unique tax advantage known as the Resident but Not Ordinarily Resident (RNOR) status. If an individual has been an NRI for 9 out of the 10 preceding years, they can claim RNOR status for up to three years after returning.

During this period, their foreign income continues to be tax-exempt in India. This “tax holiday” allows returning Indians to reshuffle their global assets and bring funds back to India without an immediate tax burden, providing a smooth financial landing.

Digital Nomads and the Modern NRI Identity

In the era of remote work, a new category of “Global Indians” is emerging—those who work for foreign companies while living in different parts of the world. These digital nomads must be even more vigilant about their NRI status.

Maintaining NRI status requires careful monitoring of stay duration to ensure they don’t inadvertently become tax residents of India, which would make their global income taxable in the country. Using financial tools like international credit cards, multi-currency accounts, and global health insurance is part of the modern NRI’s financial toolkit.

Conclusion

“What does NRI mean?” It means being a global citizen with a strategic financial foot in one of the world’s most vibrant economies. Whether it is through the tax-free benefits of NRE accounts, the high growth potential of the Indian stock market, or the legal protections of DTAA, the NRI status offers a wealth of financial advantages. By understanding the nuances of banking, investment, and taxation, NRIs can ensure that their money works just as hard as they do, regardless of where in the world they choose to call home.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.