Financial stability is rarely a straight line. For many individuals and business owners, unexpected life events—ranging from medical emergencies and job losses to global economic downturns—can suddenly make regular debt obligations feel insurmountable. In these moments of friction, the term “forbearance” often surfaces as a potential lifeline.

But what does loan forbearance actually mean, and how does it function within the broader ecosystem of personal finance? At its core, loan forbearance is a temporary agreement between a borrower and a lender to pause or reduce loan payments for a specific period. It is designed to provide “breathing room” during a documented financial hardship, preventing the borrower from falling into default or facing foreclosure. However, while it offers immediate relief, it is not a “get out of debt free” card. Understanding the mechanics, costs, and long-term implications of forbearance is essential for anyone looking to navigate a financial crisis without jeopardizing their long-term fiscal health.

Understanding the Fundamentals of Loan Forbearance

To grasp the utility of forbearance, one must first understand its structural position in the world of credit and lending. Forbearance is a discretionary concession made by a lender. While certain government-backed loans may have specific mandates for forbearance, in the private sector, it is often a negotiated settlement meant to protect both the borrower’s credit and the lender’s asset.

Definition and Core Purpose

The primary purpose of forbearance is to provide a temporary bridge over a period of financial instability. When you enter a forbearance agreement, the lender agrees not to take legal action or report you as delinquent to credit bureaus, provided you meet the terms of the temporary arrangement. It is vital to note that forbearance does not erase the debt. The principal amount remains, and in almost all cases, interest continues to accrue. The goal is simply to prevent the catastrophic consequences of default—such as the loss of a home or a massive hit to a credit score—while the borrower regains their footing.

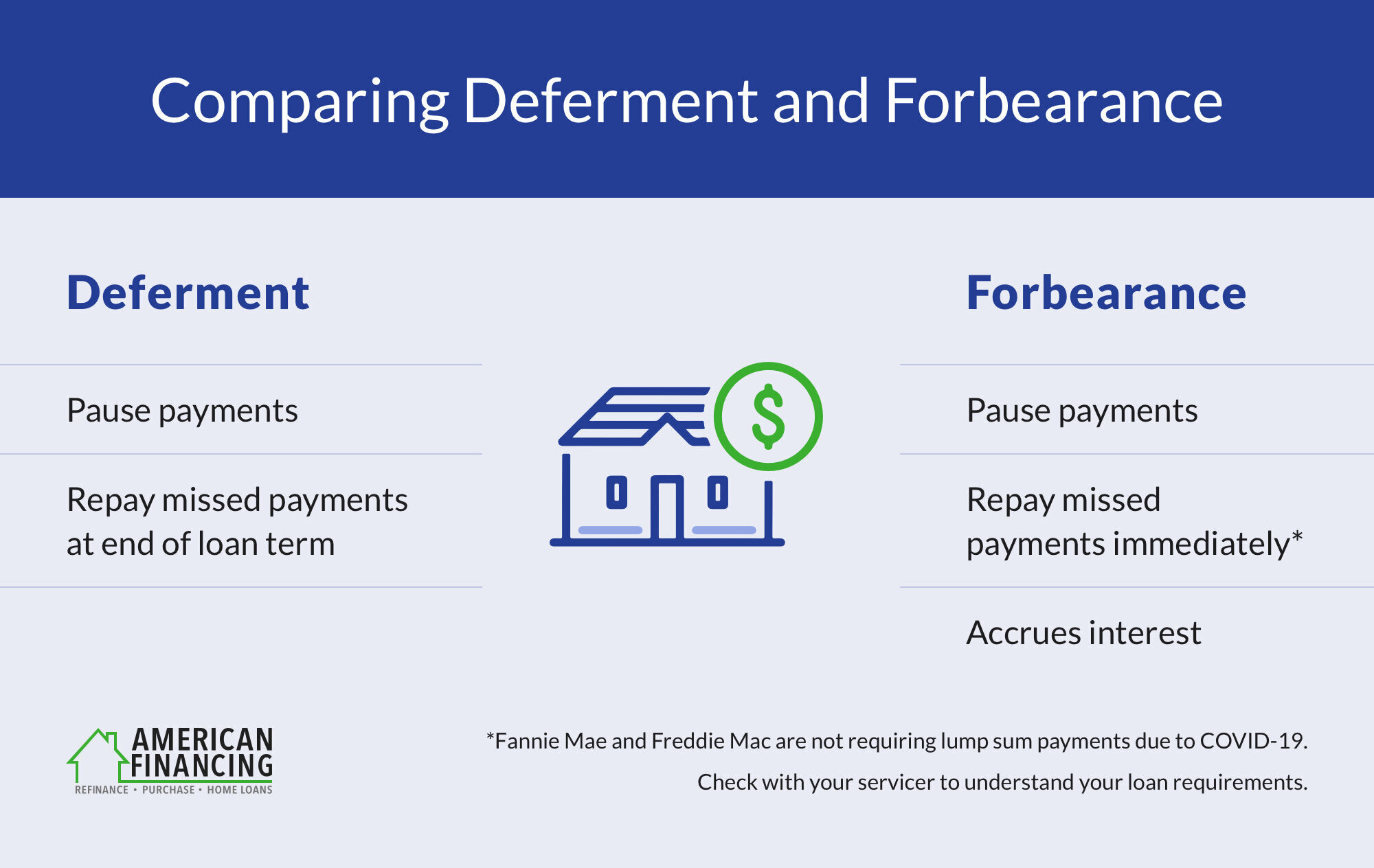

How Forbearance Differs from Deferment and Forgiveness

In the realm of personal finance, terminology is everything. Forbearance is frequently confused with “deferment” and “forgiveness,” yet they are distinct concepts.

- Forgiveness: This is the permanent cancellation of a portion or all of the debt. It is rare and usually tied to specific public service programs or extreme legal settlements.

- Deferment: Commonly associated with student loans, deferment allows you to stop payments, and in some cases (like subsidized federal loans), the government may pay the interest during the period.

- Forbearance: Unlike subsidized deferment, interest always accrues during forbearance. If you do not pay the interest during the pause, it is often “capitalized,” meaning it is added to your principal balance, increasing the total amount you owe and the amount of interest you will pay in the future.

The Impact on Your Credit Score

One of the most common questions borrowers ask is whether forbearance will ruin their credit. Generally, if a forbearance is officially granted and the borrower follows the new temporary terms, the lender will report the account as “current” but noted as “in forbearance.” While the act of being in forbearance doesn’t typically tank a credit score the way a missed payment does, it can occasionally affect your ability to take out new loans or refinance until the forbearance period has ended and a history of regular payments has resumed.

How Loan Forbearance Works in Practice

Navigating forbearance requires a proactive approach. It is never a passive process; you cannot simply stop making payments and assume the lender will understand. The process involves formal documentation, negotiation, and a clear understanding of the “repayment tail” that follows the relief period.

The Application and Approval Process

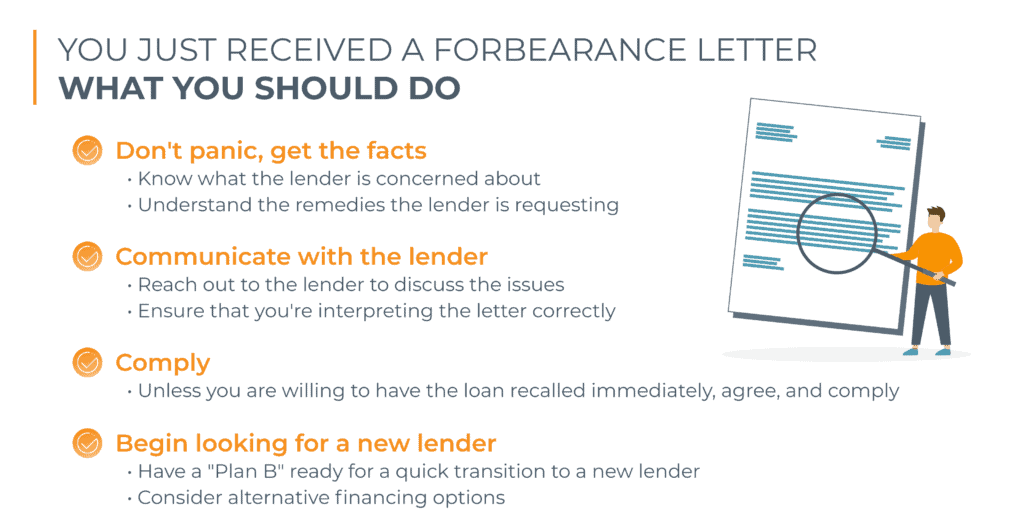

Forbearance is rarely automatic. To initiate it, a borrower must contact their loan servicer as soon as they anticipate a problem. Lenders usually require a “hardship letter” or a formal application detailing why the payments cannot be made. This might include proof of unemployment, medical bills, or records of a natural disaster. The lender then reviews the borrower’s history and the likelihood of their financial recovery before granting a specific term—usually ranging from three to twelve months.

Interest Accrual: The Silent Cost

The most significant “trap” of forbearance for the uninformed borrower is the accrual of interest. Because the principal balance remains outstanding, interest continues to build daily. For example, if you have a $300,000 mortgage at a 4% interest rate and you pause payments for six months, you aren’t just delaying six months of payments; you are adding thousands of dollars in interest to the back end of the loan. Some borrowers choose to make “interest-only” payments during their forbearance period to prevent the loan balance from ballooning. This is a savvy financial move if the borrower has even a small amount of liquidity.

The Role of the Loan Servicer

It is important to distinguish between the “lender” (the entity that owns your debt) and the “servicer” (the company that collects your payments and manages the account). When applying for forbearance, you deal with the servicer. They are the gatekeepers of the process. Effective communication with your servicer is paramount. It is highly recommended to get all forbearance agreements in writing, documenting the start and end dates, the interest treatment, and the specific requirements for when the period ends.

Common Types of Loan Forbearance

Forbearance is a tool used across various sectors of the financial world, most notably in housing and education. Each sector has its own set of rules and regulatory frameworks.

Mortgage Forbearance: Protecting Your Home

Mortgage forbearance is perhaps the most high-stakes version of this financial tool. During the COVID-19 pandemic, the CARES Act brought mortgage forbearance into the mainstream, allowing millions of homeowners to pause payments. In a typical mortgage forbearance, the lender agrees to pause the monthly payment. However, the borrower must eventually account for those missed payments. This is where many homeowners face challenges: if the agreement stipulates a “lump sum” repayment at the end of six months, the borrower might find themselves in even deeper trouble. More commonly, the missed payments are tacked onto the end of the loan term or integrated into a payment increase.

Student Loan Forbearance: Navigating Educational Debt

For federal student loans, there are two types of forbearance: Discretionary and Mandatory.

- Discretionary Forbearance: The lender decides whether to grant it based on financial hardship or illness.

- Mandatory Forbearance: The lender is required to grant it if you meet specific criteria, such as being in a medical or dental internship, serving in the National Guard, or if your total monthly student loan debt is 20% or more of your total monthly gross income.

Because student loans can last for decades, the capitalization of interest during forbearance can lead to a significant increase in the total cost of the degree.

Personal and Auto Loan Options

While less common than mortgage or student loan relief, some banks and credit unions offer “skip-a-payment” programs or short-term forbearance for auto loans and personal lines of credit. These are usually much shorter in duration (one to three months) and are intended to help a borrower get past a one-time emergency, such as a major car repair or a brief gap between jobs.

Weighing the Pros and Cons: Is It the Right Choice?

Choosing forbearance is a strategic financial decision. It should be viewed as a last-resort tool rather than a standard financial management strategy.

The Immediate Benefits of Short-Term Relief

The obvious advantage is the preservation of cash flow. In a crisis, liquidity is king. By pausing a $2,000 mortgage payment, a family can redirect those funds toward essential needs like food, utilities, and healthcare. Furthermore, forbearance protects the borrower from the aggressive collection tactics and legal ramifications of default. It buys time—time to find a new job, time to sell assets, or time to restructure a business.

Long-Term Consequences and Potential Pitfalls

The primary disadvantage is the cost. Forbearance makes your debt more expensive. If you are already struggling with debt, adding capitalized interest to your principal can create a “debt spiral” where the balance grows faster than you can pay it down once you resume payments. Additionally, some borrowers find the transition out of forbearance to be jarring. If you haven’t planned for the “exit strategy,” you may find yourself facing a higher monthly payment than the one you originally couldn’t afford.

Tax Implications and Hidden Clauses

In some niche cases, if a portion of interest is restructured or if the forbearance leads to a loan modification where debt is “extinguished,” there could be tax implications. While standard forbearance typically isn’t a taxable event, it is always wise to consult with a tax professional if the terms of your loan change significantly during the workout period.

Navigating the End of Forbearance and Moving Forward

The most critical phase of forbearance is the month before it expires. This is when the borrower must transition from “crisis mode” back into “sustainability mode.”

Repayment Structures (Lump Sum vs. Gradual)

Lenders typically offer several ways to make up the missed payments:

- Reinstatement: Paying the total missed amount in one lump sum (rarely feasible for those in hardship).

- Repayment Plan: Spreading the missed amount over several months by adding a portion to the regular monthly payment.

- Loan Extension: Moving the missed payments to the very end of the loan term, effectively extending the life of the loan.

- Loan Modification: Changing the original terms of the loan (such as the interest rate or the term length) to make the new monthly payment more affordable.

Alternatives to Forbearance

Before committing to forbearance, savvy borrowers should explore other avenues. For student loans, Income-Driven Repayment (IDR) plans are often superior to forbearance because they adjust the payment based on what you earn—sometimes to $0—while potentially qualifying for eventual forgiveness. For mortgages, refinancing to a lower interest rate can provide permanent relief rather than a temporary pause, provided the borrower still has a decent credit score and some income.

Building a Post-Hardship Financial Recovery Plan

Once the forbearance period ends, the goal should be to ensure that the hardship does not recur. This involves a rigorous audit of personal or business finances. Establishing an emergency fund—even a small one—can prevent the need for future forbearances. Furthermore, using the period of relief to eliminate smaller, high-interest debts (like credit cards) can lower your overall monthly “burn rate,” making your primary loan payments more manageable in the long run.

In conclusion, loan forbearance is a powerful instrument of financial self-defense. When used correctly, it prevents total financial collapse and provides the time necessary to recover from life’s inevitable setbacks. However, because of the accruing interest and the complexities of repayment, it requires a disciplined approach and a clear exit strategy. By understanding the nuances of the agreement and maintaining open communication with lenders, borrowers can use forbearance as a stepping stone back toward total financial health.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.