Understanding your financial health is paramount to making informed decisions about your future, whether that involves aggressive investment, planning for retirement, or simply navigating daily expenses. While many financial metrics exist, one that offers a particularly clear and immediate snapshot of your financial flexibility is liquid net worth. It’s a concept that often gets overlooked in broader discussions about net worth, yet it’s crucial for understanding your ability to react to unexpected events or seize opportune moments.

Net worth, in its most basic form, is the sum of all your assets minus all your liabilities. It’s a measure of your overall wealth. However, not all assets are created equal when it comes to accessibility. Some assets are readily convertible into cash, while others are illiquid, meaning they can take time, effort, or significant financial loss to convert into usable funds. Liquid net worth hones in on this accessibility, providing a more practical gauge of your immediate financial standing.

This article will delve deep into the meaning of liquid net worth, exploring what constitutes liquid assets, how it differs from total net worth, why it’s a vital metric for personal finance, and how you can calculate and improve it.

Understanding Liquid Assets: The Foundation of Liquidity

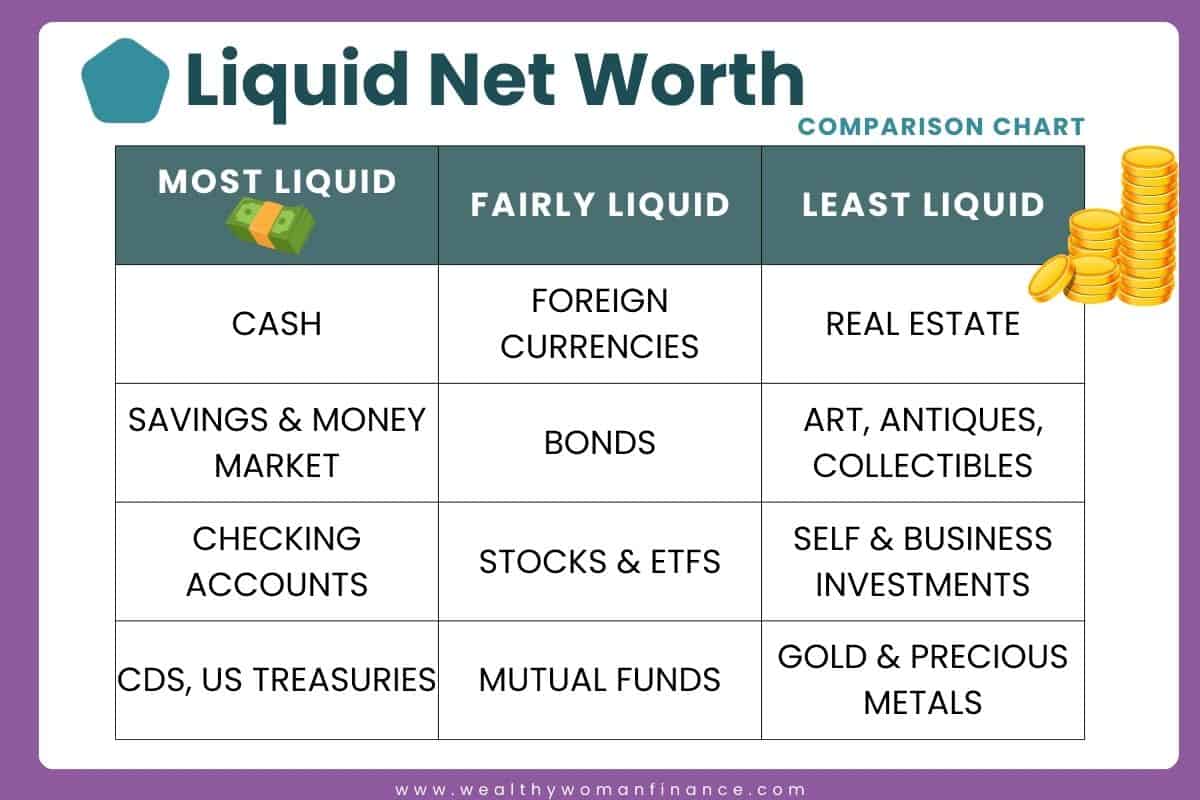

At the heart of liquid net worth lies the concept of liquid assets. These are the financial resources that can be quickly and easily converted into cash without a substantial loss in value. Think of them as the money readily available in your wallet, your checking account, or easily accessible savings. The key characteristic is their speed and lack of significant depreciation during conversion.

Cash and Cash Equivalents

The most obvious and fundamental liquid assets are physical cash and its immediate equivalents. This includes:

- Physical Currency: The bills and coins you keep in your wallet or at home. While not often held in large amounts for everyday use, it represents the most fundamental form of liquid asset.

- Checking Accounts: Funds held in your primary checking accounts are instantly accessible via debit card, checks, or electronic transfers.

- Savings Accounts: Money deposited in traditional savings accounts offers a high degree of liquidity, typically accessible with minimal delay or penalty.

- Money Market Accounts: These accounts, often offered by banks and brokerage firms, typically offer higher interest rates than standard savings accounts while still providing easy access to funds, often with check-writing privileges.

- Certificates of Deposit (CDs) with Short Maturities: While CDs are designed to lock away funds for a period, those with short maturities (e.g., 3 to 12 months) can be considered relatively liquid, especially if the penalty for early withdrawal is minor and acceptable.

Marketable Securities

Beyond immediate cash, certain investments are also considered highly liquid due to their active trading markets and established valuations. These are assets that can be sold on an exchange within a short timeframe at or near their current market price.

- Stocks: Shares of publicly traded companies on major stock exchanges (e.g., NYSE, Nasdaq) can generally be sold within minutes during trading hours. The price you receive will fluctuate with market conditions, but the ability to sell quickly is what defines their liquidity.

- Bonds: Similar to stocks, publicly traded bonds, especially government bonds or highly rated corporate bonds, can be sold on the secondary market. While some bonds might have less active trading than popular stocks, they are generally considered liquid.

- Exchange-Traded Funds (ETFs) and Mutual Funds: These pooled investment vehicles, traded on exchanges or redeemable through the fund company, are typically highly liquid. Their value is derived from the underlying assets they hold, and they can be bought and sold with relative ease.

The accessibility and speed of conversion are paramount here. While you might own a valuable piece of art or a vintage car, these are not liquid assets because finding a buyer at a fair price can take weeks or months, and the negotiation process can be lengthy.

Differentiating Liquid Net Worth from Total Net Worth

It’s essential to distinguish liquid net worth from the more commonly discussed metric: total net worth. While both are crucial components of financial assessment, they serve different purposes and paint distinct pictures of your financial well-being.

Total Net Worth: The Comprehensive Wealth Snapshot

Total net worth is the ultimate balance sheet of your financial life. It encompasses all your assets, regardless of their liquidity, minus all your liabilities.

-

Assets: This includes everything you own that has monetary value.

- Liquid Assets: As defined above (cash, checking/savings accounts, marketable securities).

- Illiquid Assets: These are assets that are not easily or quickly convertible to cash without significant loss. Examples include:

- Real Estate: Your primary residence, investment properties, vacant land. Selling a property can take months and involves substantial transaction costs.

- Retirement Accounts: While valuable, funds in 401(k)s, IRAs, and pensions are typically subject to penalties and taxes if withdrawn before retirement age, making them illiquid in the short to medium term.

- Business Ownership: Equity in a private business is often highly illiquid, as finding a buyer and agreeing on a valuation can be a complex and lengthy process.

- Valuable Personal Property: Collectibles, artwork, jewelry, vehicles (unless it’s your primary means of business and you can sell it quickly).

- Annuities: These are often illiquid, with surrender charges for early withdrawal.

-

Liabilities: This includes everything you owe to others.

- Mortgages: Outstanding balances on home loans.

- Auto Loans: Balances on vehicle financing.

- Student Loans: Outstanding educational debt.

- Credit Card Balances: Amounts owed on credit cards.

- Personal Loans: Any other outstanding debts.

The formula for total net worth is:

Total Net Worth = Total Assets – Total Liabilities

Liquid Net Worth: The Measure of Financial Agility

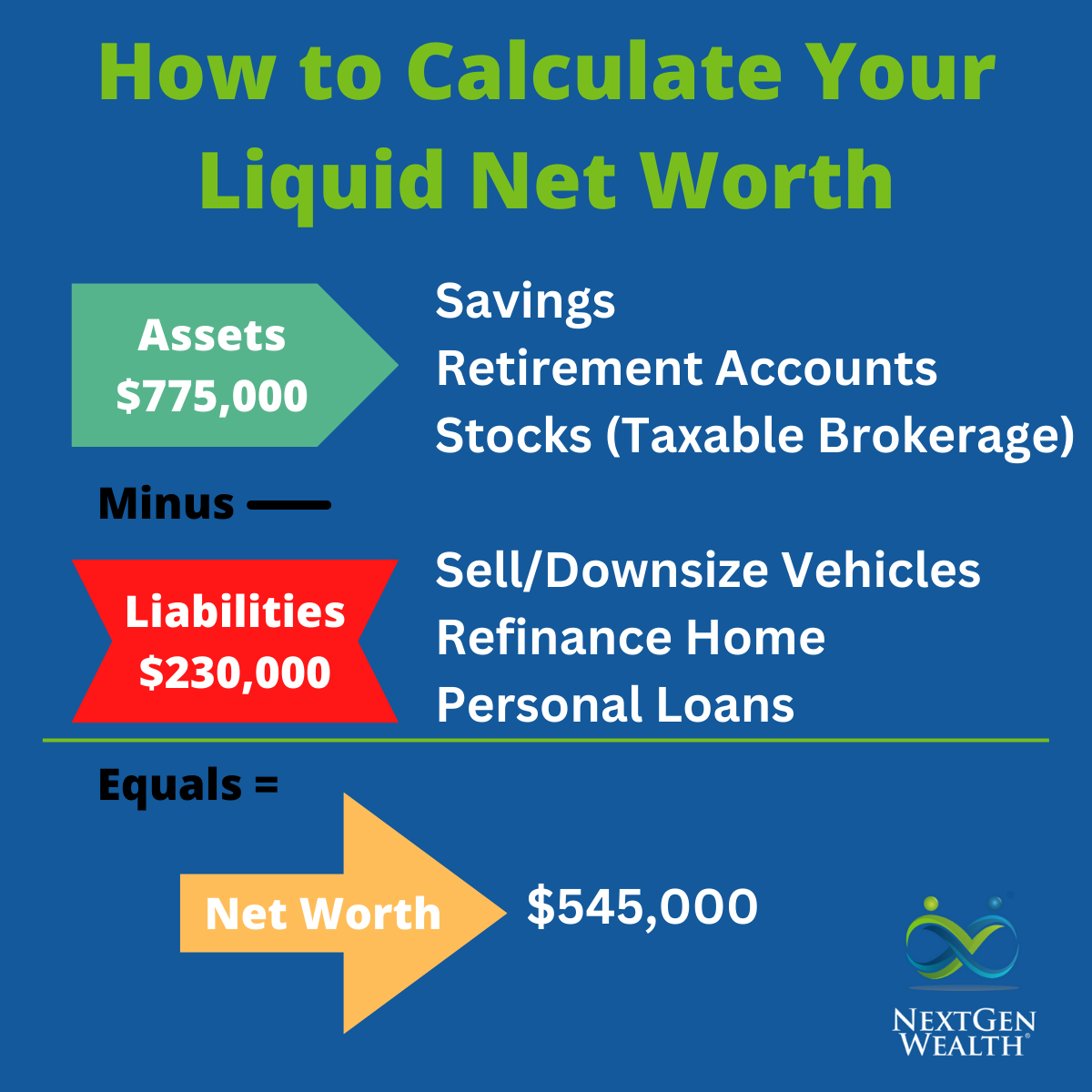

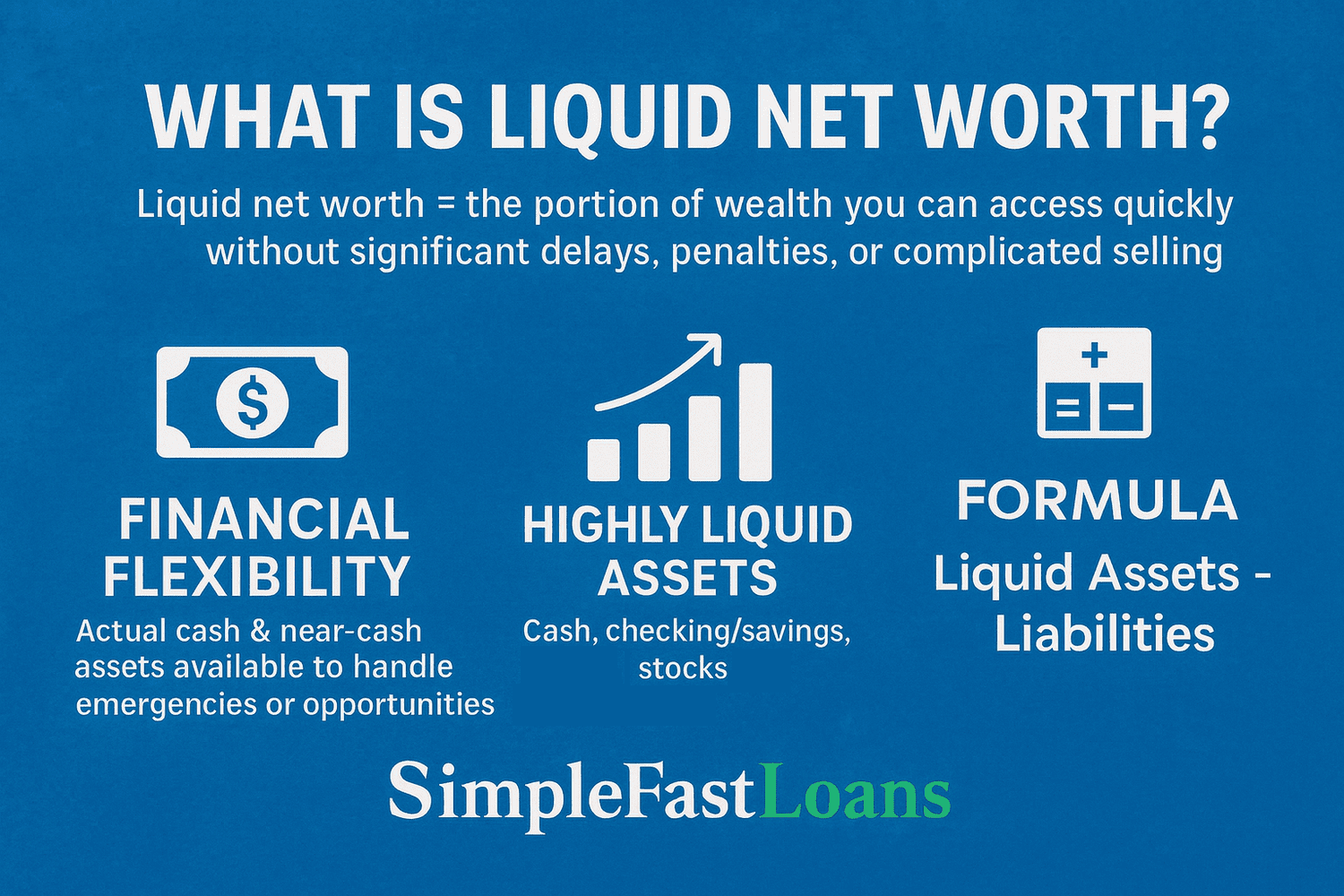

Liquid net worth, on the other hand, focuses exclusively on your immediate financial capacity. It is calculated by taking your liquid assets and subtracting any short-term liabilities that would typically be paid from those liquid funds.

- Liquid Assets: Cash, checking accounts, savings accounts, money market accounts, short-term CDs, stocks, bonds, ETFs, and mutual funds.

- Short-Term Liabilities: These are obligations typically due within a year or that would be paid from your readily available cash. This often includes:

- Upcoming bill payments (rent, utilities, mortgage payments due soon).

- Credit card balances due for payment.

- Short-term loans or payments due on other personal loans within the next year.

- Unpaid taxes that are imminent.

The formula for liquid net worth is:

Liquid Net Worth = Liquid Assets – Short-Term Liabilities

The primary difference lies in the scope of assets considered. Total net worth provides a long-term perspective on wealth accumulation, while liquid net worth offers a critical short-term perspective on financial resilience and flexibility. You could have a high total net worth due to significant real estate holdings or retirement savings, but still have a low liquid net worth if you don’t have readily accessible cash to cover unexpected expenses.

Why Liquid Net Worth Matters: Your Financial Safety Net

Understanding and maintaining a healthy liquid net worth is not just an academic exercise; it has profound practical implications for your financial well-being and your ability to navigate life’s uncertainties. It serves as your immediate financial safety net, empowering you to handle unexpected events with confidence and to seize opportunities without undue stress.

The Importance of an Emergency Fund

One of the most compelling reasons to focus on liquid net worth is its direct correlation to the strength of your emergency fund. An emergency fund is a pool of money set aside specifically to cover unexpected expenses, such as:

- Job Loss: If you lose your primary source of income, your liquid assets can provide a buffer while you search for new employment, preventing you from having to sell long-term investments at a loss or go into debt.

- Medical Emergencies: Unexpected medical bills, even with insurance, can be substantial. Having liquid funds readily available can alleviate financial strain during a health crisis.

- Home or Auto Repairs: Major appliances can break down, or your car might need significant repairs. These are often urgent expenses that require immediate cash.

- Natural Disasters: In the event of a natural disaster, you might need funds for temporary housing, essential supplies, or to cover deductibles for insurance claims.

A well-funded emergency fund is typically recommended to cover 3 to 6 months of essential living expenses. This fund should be kept in highly liquid accounts, such as savings accounts or money market funds, ensuring you can access it immediately when needed. A strong liquid net worth ensures you have the resources to build and maintain this crucial safety net.

Seizing Financial Opportunities

Beyond acting as a defense against unexpected expenses, a healthy liquid net worth also positions you to take advantage of financial opportunities. These might include:

- Investment Opportunities: Market downturns can present excellent buying opportunities for stocks or other assets. If you have liquid funds, you can invest at lower prices without having to sell other assets or take on debt.

- Real Estate Deals: Sometimes, properties are listed at attractive prices for quick sales. Having cash on hand can allow you to make a competitive offer and secure such a deal.

- Business Ventures: If you have an idea for a side hustle or a small business, having liquid capital can provide the initial funding to get it off the ground without immediately needing external financing.

- Negotiating Power: In certain situations, having the ability to pay in cash can give you significant negotiating power, whether you’re buying a car, a piece of furniture, or even negotiating a settlement.

Essentially, liquidity provides you with options and reduces your dependence on immediate borrowing or the forced liquidation of less accessible assets.

Reducing Financial Stress and Increasing Financial Freedom

The presence of readily available funds can significantly reduce financial stress. Knowing that you can cover unexpected costs without derailing your long-term financial goals provides a sense of security and peace of mind. This psychological benefit is invaluable and contributes to overall well-being.

Furthermore, a robust liquid net worth is a cornerstone of financial freedom. It means you are less beholden to lenders and less vulnerable to market fluctuations that might impact your illiquid assets. It empowers you to make choices based on your desires and goals, rather than being dictated by immediate financial pressures. This financial agility is a critical component of achieving true financial independence.

Calculating and Improving Your Liquid Net Worth

Understanding how to calculate your liquid net worth and implementing strategies to improve it are essential steps towards enhanced financial security and flexibility. It’s a dynamic metric that requires regular review and proactive management.

The Calculation Process: A Step-by-Step Approach

Calculating your liquid net worth is straightforward once you’ve identified your liquid assets and short-term liabilities.

-

Identify and Sum Your Liquid Assets:

- Go through your accounts and list all your cash and cash equivalents:

- Physical cash on hand.

- Balances in all checking accounts.

- Balances in all savings accounts.

- Balances in money market accounts.

- Value of short-term CDs (consider the principal amount).

- Identify and sum your readily marketable securities:

- Current market value of all stocks you own.

- Current market value of all bonds you own.

- Current market value of all ETFs and mutual funds you own.

- Total Liquid Assets = Sum of all listed liquid assets.

- Go through your accounts and list all your cash and cash equivalents:

-

Identify and Sum Your Short-Term Liabilities:

- List all your financial obligations that are due within the next 12 months:

- Current credit card balances.

- Upcoming mortgage payments (e.g., the next 12 months).

- Upcoming rent payments (e.g., the next 12 months).

- Balances on auto loans due within the next year.

- Balances on student loans due within the next year.

- Any other personal loans or outstanding debts with payments due within the next 12 months.

- Estimated tax payments due in the next year.

- Total Short-Term Liabilities = Sum of all listed short-term liabilities.

- List all your financial obligations that are due within the next 12 months:

-

Calculate Your Liquid Net Worth:

- Liquid Net Worth = Total Liquid Assets – Total Short-Term Liabilities

Example:

Let’s say you have:

- Checking Account: $5,000

- Savings Account: $15,000

- Money Market Fund: $10,000

- Stocks: $25,000

- ETFs: $10,000

- Total Liquid Assets = $65,000

And your short-term liabilities are:

- Credit Card Balance: $3,000

- Next 12 Months Mortgage Payments (estimated): $24,000

- Next 12 Months Car Loan Payments (estimated): $6,000

- Total Short-Term Liabilities = $33,000

Your Liquid Net Worth would be:

$65,000 – $33,000 = $32,000

Strategies for Improving Your Liquid Net Worth

Once you’ve calculated your liquid net worth, you might identify areas for improvement. Fortunately, there are several proactive strategies you can employ:

- Prioritize Building an Emergency Fund: This is the most direct way to boost your liquid net worth. Automate regular transfers from your checking account to a dedicated high-yield savings or money market account. Treat this savings goal as a non-negotiable expense.

- Reduce High-Interest Debt: Carrying significant credit card debt or high-interest personal loans erodes your liquid net worth. Aggressively pay down these debts. The interest you save is effectively a guaranteed return, and freeing up cash flow allows you to build liquidity faster.

- Increase Income: Explore avenues to increase your earnings. This could involve negotiating a raise at your current job, taking on a part-time job, starting a freelance gig, or developing a side hustle. The additional income can be directed towards building liquid assets.

- Optimize Your Spending: Conduct a thorough review of your budget and identify areas where you can cut back on non-essential expenses. Redirecting these savings into liquid assets will directly improve your financial flexibility.

- Convert Illiquid Assets Strategically (with Caution): While not always advisable for long-term goals, if you have significantly underperforming or non-essential illiquid assets, consider selling them. However, be mindful of market conditions, transaction costs, and potential capital gains taxes. This should be a carefully considered decision, not a hasty one.

- Review Investment Allocation: Ensure your investment portfolio is appropriately balanced. While long-term growth is important, having a portion of your portfolio in highly liquid, lower-risk investments can contribute to your liquid net worth without sacrificing all growth potential. For instance, a well-diversified ETF or a balanced mutual fund can offer both liquidity and growth.

Regularly reviewing your liquid net worth, perhaps quarterly or annually, will help you stay on track with your financial goals and make necessary adjustments to your strategies. It’s a powerful tool that, when understood and managed effectively, can lead to greater financial security, reduced stress, and increased control over your financial destiny.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.