In the world of finance, the term “issued” is a fundamental pillar upon which modern markets, corporate structures, and personal credit systems are built. At its simplest, to “issue” something in a financial context means to officially distribute, release, or bring a financial instrument into existence. Whether it is a company releasing shares to the public, a government printing currency, or a bank providing a new credit card to a consumer, the act of issuance represents the formal transition of a financial asset from the creator to the holder.

Understanding what “issued” means is crucial for investors, business owners, and everyday consumers alike. It dictates how value is created, how debt is structured, and how ownership is defined. This article explores the multifaceted definitions of issuance within the “Money” niche, focusing on equity, debt instruments, personal credit, and macro-level currency management.

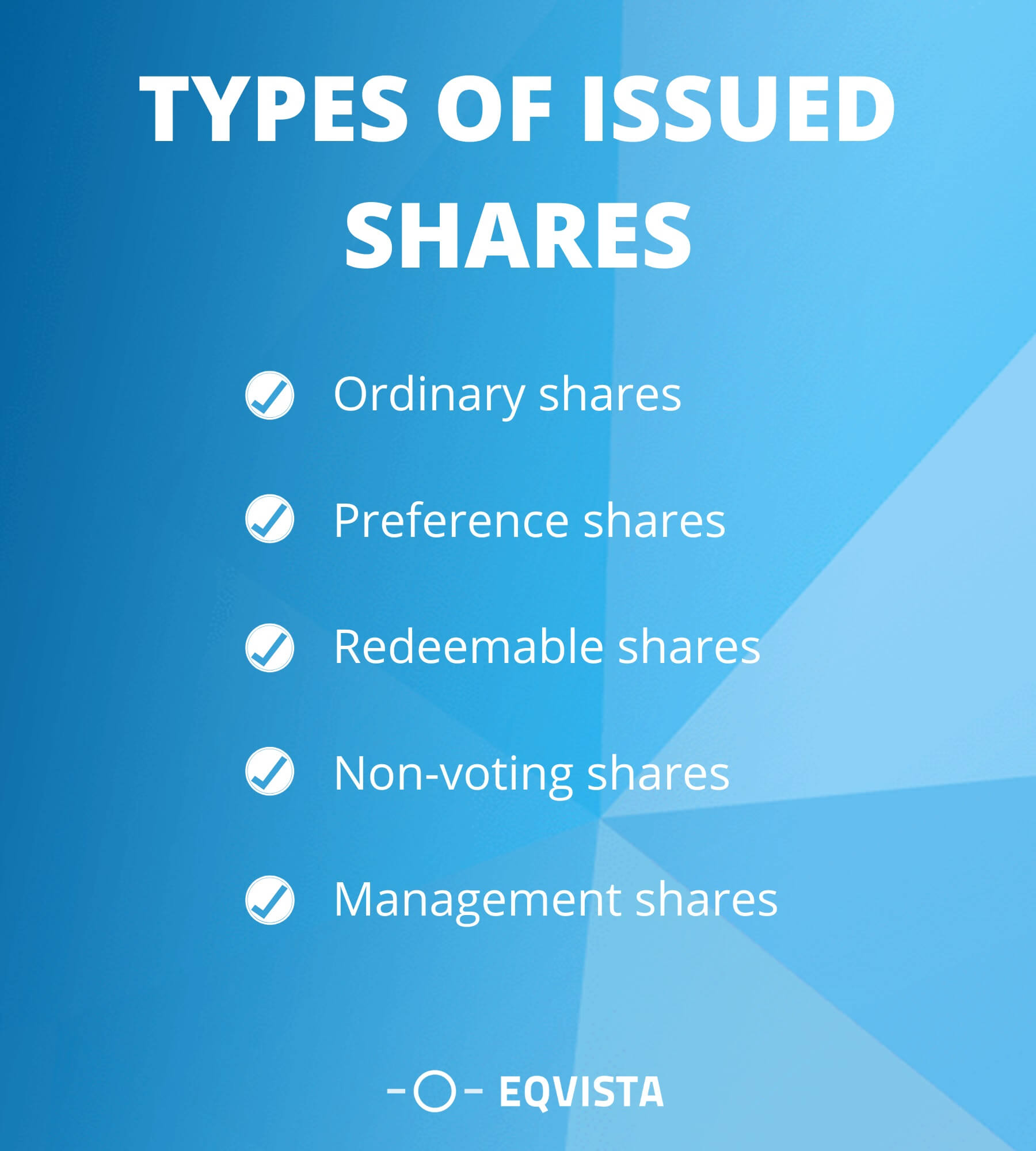

1. Issued Capital: How Companies Create Ownership and Raise Equity

For a corporation, the word “issued” is most frequently used in the context of “issued shares” or “issued capital.” This refers to the portion of a company’s total authorized stock that has been sold and held by shareholders, including both insiders and the general public.

Authorized vs. Issued Shares: Defining the Boundaries

To understand issued capital, one must first understand authorized shares. When a company is incorporated, its charter specifies the maximum number of shares it is legally allowed to create; these are “authorized” shares. However, a company rarely releases all its authorized shares at once.

“Issued shares” are the subset of authorized shares that the company has actually distributed to investors, employees, or founders. For example, if a startup is authorized to have 10,000,000 shares but only sells 2,000,000 during its first funding round, the issued capital consists of those 2,000,000 shares. The remaining 8,000,000 are “unissued,” sitting in the company’s “treasury” for future use.

The Mechanics of an Initial Public Offering (IPO)

The most high-profile instance of issuance occurs during an Initial Public Offering (IPO). This is the process by which a private company becomes a public one by issuing shares to the public for the first time. In this scenario, the company works with investment banks (the underwriters) to determine the “issue price”—the price at which the shares will be sold to the initial investors before they begin trading on a secondary exchange like the NYSE or NASDAQ.

Share Dilution and the Impact of New Issuance

For existing shareholders, the issuance of new stock is a double-edged sword. While it brings in essential capital for growth, it can lead to “dilution.” When a company issues more shares, each existing share represents a smaller percentage of ownership in the company. Savvy investors closely monitor a company’s “shares outstanding”—which is the number of issued shares minus any shares the company has bought back—to gauge the true value of their holdings.

2. Debt Issuance: How Organizations Borrow Capital Through Bonds

In the realm of fixed-income investing, “issued” refers to the creation of debt. When a government needs to build a bridge or a corporation needs to fund a merger, they often “issue” bonds rather than taking out a traditional bank loan.

The Role of the Issuer and the Holder

In a bond issuance, the “issuer” is the borrower, and the “holder” (the investor) is the lender. When a bond is issued, the issuer provides a legal document promising to pay back the principal amount (the “par value”) at a specific date (the “maturity date”), along with regular interest payments known as “coupons.”

The moment of issuance is known as the “primary market” transaction. Once the bond is issued and in the hands of the public, it can be traded among investors in the “secondary market,” where its price will fluctuate based on interest rates and the creditworthiness of the original issuer.

Government Bonds and Treasury Issuance

On a macroeconomic scale, the issuance of government debt is a vital tool for national fiscal policy. In the United States, the Department of the Treasury issues Treasury Bonds, Notes, and Bills. These are considered some of the safest investments in the world because they are backed by the “full faith and credit” of the government. When the Treasury issues these securities, it is essentially borrowing money from the public to fund government operations.

Corporate Bonds and Credit Ratings

When a corporation issues debt, the process is slightly more complex. Before issuance, the company usually seeks a credit rating from agencies like Moody’s or Standard & Poor’s. This rating tells potential investors how likely the issuer is to pay back the debt. A “newly issued” corporate bond with a high credit rating will typically offer a lower interest rate than a “junk bond” issued by a company with a higher risk of default.

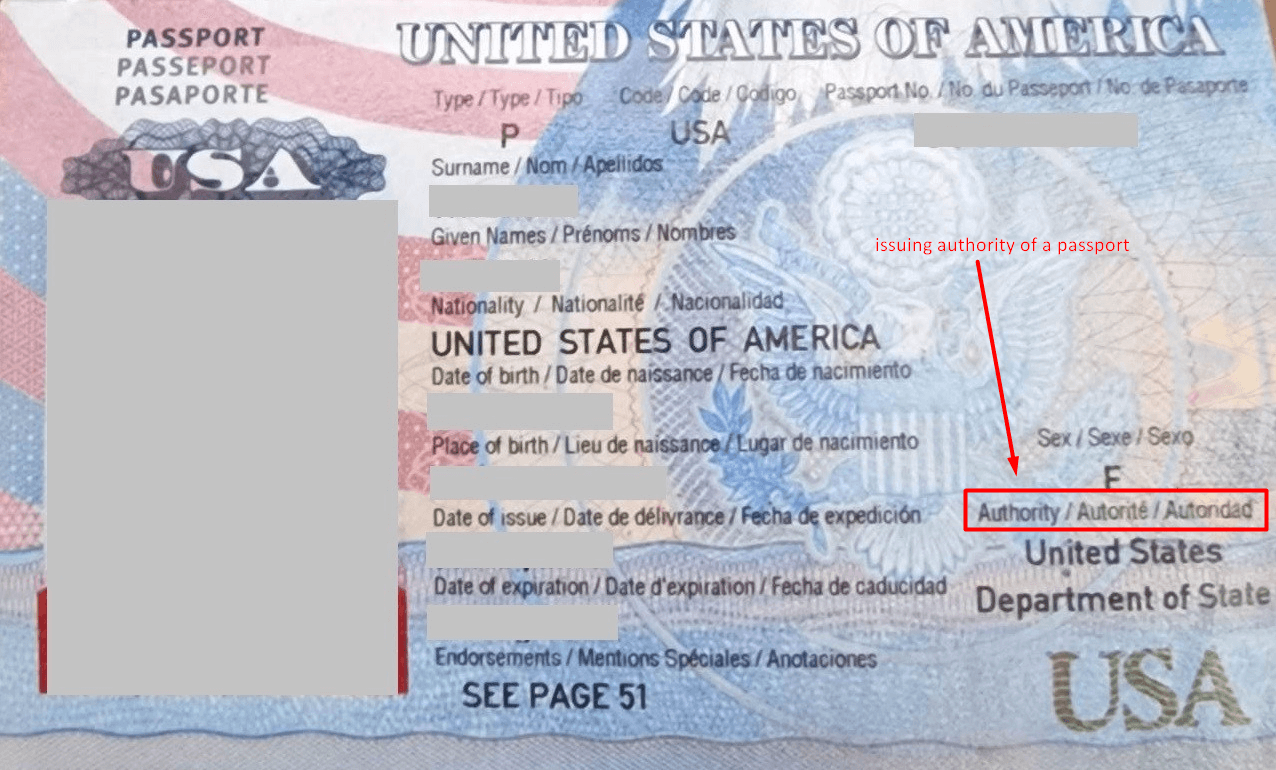

3. Personal Finance and Consumer Credit Issuance

On a personal level, the term “issued” most often appears in the context of financial products like credit cards, debit cards, and loans. In this niche, the “issuer” is typically a financial institution that provides the line of credit or the financial vehicle to the consumer.

The Role of the Issuing Bank

When you carry a credit card in your wallet, it is “issued” by a bank (such as Chase, Barclays, or a local credit union). The issuing bank is responsible for approving the consumer’s application, setting the credit limit, and managing the billing and collection process. While the card might bear a logo like Visa or Mastercard, those entities are “networks” that facilitate the transaction; they are not the issuers. The issuer is the entity that actually extends the credit to you.

Loan Disbursement vs. Loan Issuance

In the mortgage or personal loan industry, “issuance” and “disbursement” are often used interchangeably, but they have subtle differences. The issuance of a loan occurs when the lender officially approves the contract and creates the debt obligation. The disbursement is the actual act of sending the funds to the borrower or the seller. Understanding the “date of issuance” is critical because it often marks the beginning of interest accrual.

The Rise of Fintech and Virtual Issuance

Modern technology has transformed how financial products are issued. In the past, “issuing” a credit card meant printing a physical plastic card and mailing it to a customer, a process that took days. Today, fintech companies utilize “instant issuance” or “virtual issuance.” This allows a user to be approved for a credit line and have a virtual card issued to their digital wallet (like Apple Pay or Google Pay) in a matter of seconds. This shift has accelerated the velocity of consumer spending and changed the landscape of personal banking.

4. Currency Issuance and Central Banking

At the highest level of the money niche lies the concept of currency issuance. This is the process by which a country’s central bank, such as the Federal Reserve in the U.S. or the European Central Bank in the EU, manages the supply of legal tender.

Fiat Currency and Legal Tender

Most modern economies operate on “fiat” currency, which is money that is not backed by a physical commodity like gold but is “issued” by government decree. When a central bank decides to issue more currency, it is not simply printing paper; it is managing the “monetary base.” This can be done through physical printing or, more commonly in the digital age, through “open market operations”—where the central bank buys government bonds to inject liquidity into the banking system.

Controlling Inflation through Issuance Policy

The rate at which a central bank issues or withdraws currency is the primary lever for controlling inflation. If a central bank issues too much currency too quickly, the value of each unit of money decreases, leading to rising prices (inflation). Conversely, if the issuance is too tight, it can lead to a decrease in spending and potential economic stagnation. Therefore, the “issuance policy” of a nation is one of the most scrutinized aspects of global finance.

The Future of Issuance: Central Bank Digital Currencies (CBDCs)

The next frontier of financial issuance is the development of Central Bank Digital Currencies (CBDCs). Unlike decentralized cryptocurrencies like Bitcoin, CBDCs are digital forms of fiat money issued and regulated by the central bank. The issuance of a CBDC would represent a fundamental shift in how money enters the economy, potentially bypassing traditional commercial banks and allowing the government to issue stimulus or manage interest rates with surgical precision directly to citizens’ digital wallets.

Conclusion: The Power of the “Issued” Designation

In conclusion, “issued” is a term that denotes the birth of a financial asset. Whether it is a share of stock that gives an investor a piece of a company’s future, a bond that provides a steady stream of income, a credit card that offers purchasing power, or the very cash in your pocket, every financial tool begins its life at the moment of issuance.

For the investor, understanding issuance means understanding the potential for growth and the risks of dilution. For the borrower, it means understanding the terms of a debt obligation. For the citizen, it means understanding the forces that dictate the value of their currency. By mastering the nuances of what it means to be “issued,” individuals can navigate the complex world of finance with greater clarity, making more informed decisions about how they earn, spend, and grow their wealth.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.