In the high-stakes arena of corporate litigation and financial dispute resolution, the term “hearsay” is often wielded like a shield or a sword. For business owners, investors, and financial professionals, understanding the legal mechanics of hearsay is not merely an academic exercise in law; it is a critical component of risk management. When millions of dollars in assets, stock valuations, or contractual obligations are on the line, the admissibility of a single statement can determine the solvency of an enterprise.

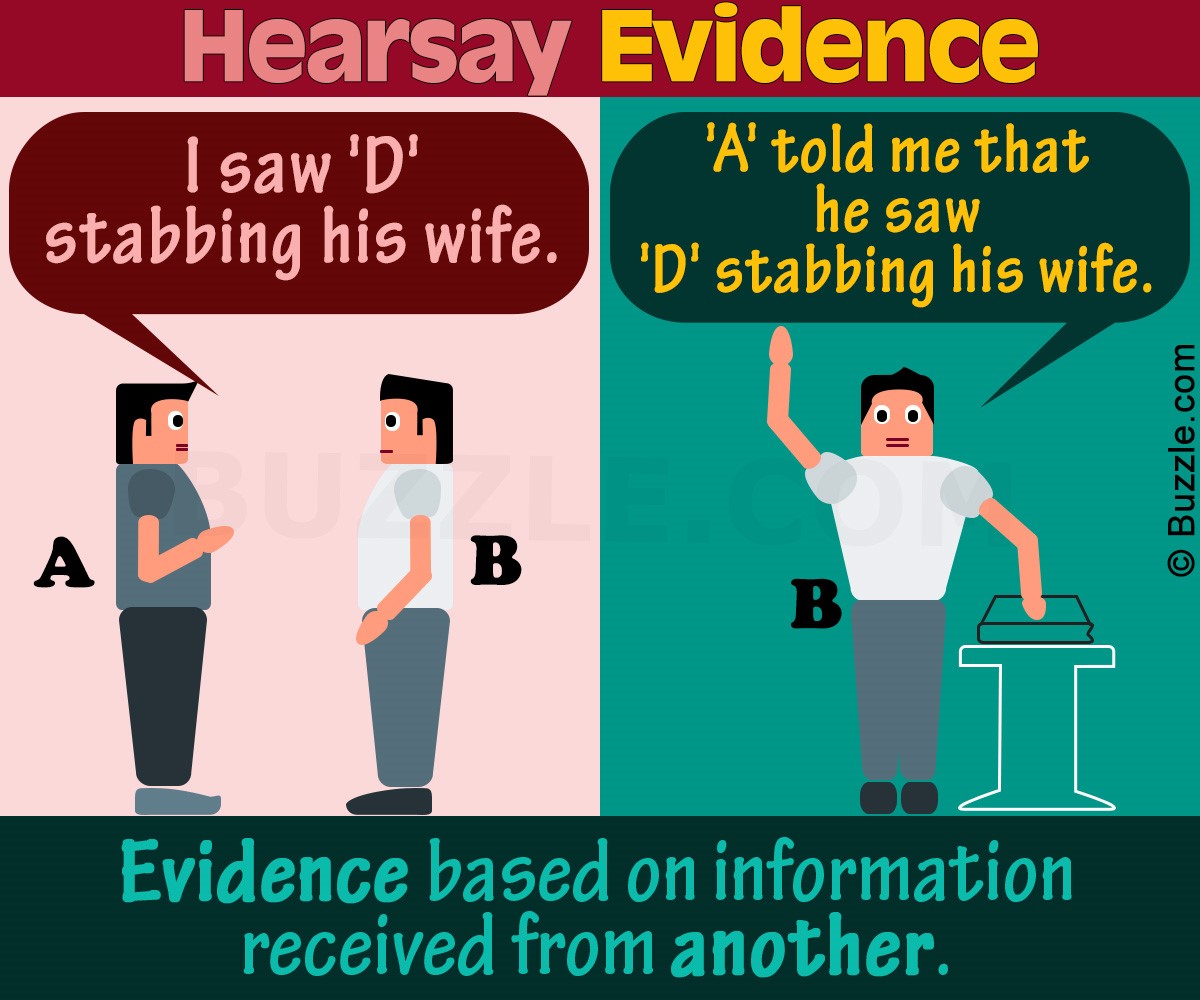

At its core, hearsay is an out-of-court statement offered in court to prove the truth of the matter asserted. While it sounds simple, the financial ramifications of this rule are vast. In the world of “Money”—encompassing personal finance, business valuation, and investment strategy—the hearsay rule governs what evidence can be used to protect your wealth and what “evidence” is nothing more than expensive noise.

Defining Hearsay within the Corporate and Financial Landscape

To navigate the financial risks associated with legal proceedings, one must first grasp the technical definition of hearsay. According to the Federal Rules of Evidence (specifically Rule 801), hearsay occurs when a witness testifies about what someone else said in order to prove that the content of that statement is true.

The Legal Definition vs. Business Interpretation

In a business context, hearsay often surfaces during disputes over “handshake deals” or informal email exchanges. If a Chief Financial Officer (CFO) testifies that a vendor told them the price of raw materials would remain fixed for three years, that testimony is hearsay if it is used to prove the price was indeed fixed.

From a financial perspective, the danger of hearsay lies in its inherent unreliability. Courts exclude hearsay because the person who made the original statement—the declarant—is not under oath and cannot be cross-examined. For an investor, relying on hearsay is akin to making a trade based on a “hot tip” from a stranger at a bar; the lack of verifiability creates an unacceptable level of financial exposure.

Why the “Truth of the Matter Asserted” Matters for Your Bottom Line

The phrase “truth of the matter asserted” is the pivot point of the hearsay rule. If a statement is introduced for a reason other than proving its truth, it is not hearsay. For example, in a defamation case where a business’s reputation (a key intangible asset) has been harmed, a statement might be introduced to show the effect it had on the listener, rather than to prove the statement itself was true.

Understanding this distinction is vital for financial planning. When documenting transactions, businesses must ensure that their communications are structured to be admissible. Relying on “what was said” during a high-stakes negotiation is a recipe for a financial loss if those statements cannot be admitted as evidence during a breach of contract trial.

The Financial Risk of Relying on Inadmissible Information

In the realms of investing and business finance, information is the primary currency. However, not all information is created equal. The hearsay rule serves as a filter, and failing to understand how that filter works can lead to significant fiscal damage.

Market Volatility and Unverifiable Rumors

The stock market is often driven by sentiment, which is frequently fueled by what is effectively “market hearsay.” Rumors of an acquisition, a pending regulatory fine, or a change in leadership can cause massive swings in valuation. However, from a legal and rigorous financial analysis standpoint, these rumors are inadmissible.

Professional investors must distinguish between “hearsay” (unverified reports) and “primary data” (audited financial statements, SEC filings, and direct testimony). Companies that make significant capital allocations based on hearsay risk not only direct financial loss but also potential derivative lawsuits from shareholders for failing to perform adequate due diligence.

The High Cost of Discovery in Financial Fraud Cases

When a business is embroiled in litigation—such as a forensic audit or a fraud investigation—the process of “discovery” becomes an enormous financial drain. Legal teams must sift through mountains of data to identify what is admissible evidence versus what is hearsay.

If a company’s financial records are disorganized or rely heavily on oral tradition rather than documented logs, the cost of proving a financial claim skyrockets. Every hour a high-priced attorney spends trying to find a hearsay exception for a crucial piece of evidence is an hour billed against the company’s bottom line. In this sense, the hearsay rule acts as a tax on companies with poor administrative hygiene.

Exceptions to the Hearsay Rule: Protecting Your Business Assets

Fortunately for the business world, the law recognizes that commerce would grind to a halt if every out-of-court statement were excluded. There are several “exceptions” to the hearsay rule that are specifically designed to accommodate the realities of modern finance and record-keeping.

Business Records Exception (Rule 803(6))

This is perhaps the most important legal rule for any business owner or financial officer. Under the Business Records Exception, reports, logs, or data compilations are admissible as evidence—even though they are technically out-of-court statements—if they were made at or near the time by someone with knowledge and were kept in the regular course of business.

From a money management perspective, this underscores the necessity of robust accounting software and meticulous record-keeping. If your business is sued, your QuickBooks files, bank statements, and automated inventory logs are generally admissible. These records provide a “safe harbor” against hearsay objections, ensuring that your financial narrative is heard by the court.

Statements Against Interest in Financial Disputes

Another critical exception is the “Statement Against Interest.” This occurs when a person makes a statement that is so contrary to their proprietary or pecuniary interest that a reasonable person wouldn’t have said it unless it were true.

In a partnership dispute or a high-net-worth divorce settlement, if one party admits in an email that they “know the offshore account belongs to the firm,” that statement is often admissible because it harms their own financial standing. For those involved in financial negotiations, it is important to realize that your own admissions can bypass the hearsay rule and be used to liquidate your assets in court.

Strategies for Financial Risk Mitigation and Evidence Management

Given that hearsay rules can make or break a financial legal strategy, how should individuals and corporations manage their “money” and “data” to ensure they are protected?

Implementing Robust Internal Documentation Systems

The best defense against the hearsay rule is a culture of documentation. Every significant financial commitment, internal policy change, or external agreement should be reduced to writing and stored within a formal system.

- Standard Operating Procedures (SOPs): Ensure that your financial team follows a consistent protocol for recording transactions. This establishes the “regular course of business” required for the Business Records Exception.

- Digital Audit Trails: Use software that timestamps entries and tracks who made them. In a court of law, an automated audit trail is far more persuasive (and admissible) than a manager’s memory of who authorized a payment.

- Contemporaneous Notes: If a verbal agreement is made, immediately follow up with a “confirming email.” This creates a paper trail that can serve as a “present sense impression” or a business record, moving the information out of the realm of inadmissible hearsay.

Due Diligence: Moving Beyond Hearsay in Investment Analysis

For individual investors and venture capitalists, the “hearsay rule” should be adopted as a mental model for due diligence. When evaluating a side hustle, a startup investment, or a real estate deal, ask yourself: Is this information hearsay, or is it verifiable?

If a founder tells you, “Big Tech Company X is interested in buying us,” that is hearsay. If you see a signed Letter of Intent (LOI) on Big Tech Company X’s letterhead, that is a business record. Successful wealth building requires shifting your decision-making away from hearsay and toward hard, admissible data.

The Bottom Line: Evidence as an Asset

In the intersection of law and money, information is not just power—it is a tangible asset. Understanding “what hearsay means in court” allows you to value your information correctly. If your business relies on oral promises and unrecorded conversations, you are operating with a “toxic asset” that may have zero value in a legal crisis.

By prioritizing the Business Records Exception and maintaining a rigorous approach to documentation, you protect your personal finance and corporate interests. In court, as in the market, the truth only matters if you can prove it with evidence that sticks. Treat your documentation with the same respect you treat your capital, and you will find that the rules of evidence become a tool for financial stability rather than a trap for the unwary.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.