In the world of finance, few acronyms carry as much weight as “FV.” Standing for Future Value, this concept serves as a cornerstone for personal investing, corporate finance, and long-term wealth management. Whether you are calculating the potential growth of a retirement fund, evaluating a business investment, or simply deciding between a lump sum payment today and a series of payments over time, understanding FV is essential. At its core, Future Value is a window into the potential of your capital, allowing you to project what an investment made today will be worth at a specific point in the future, given a certain rate of return.

Understanding the Fundamentals of Future Value

To grasp what FV means, one must first look at the broader landscape of financial theory. It is not merely a mathematical output; it is a reflection of economic potential and the behavior of capital over time.

Defining Future Value in a Financial Context

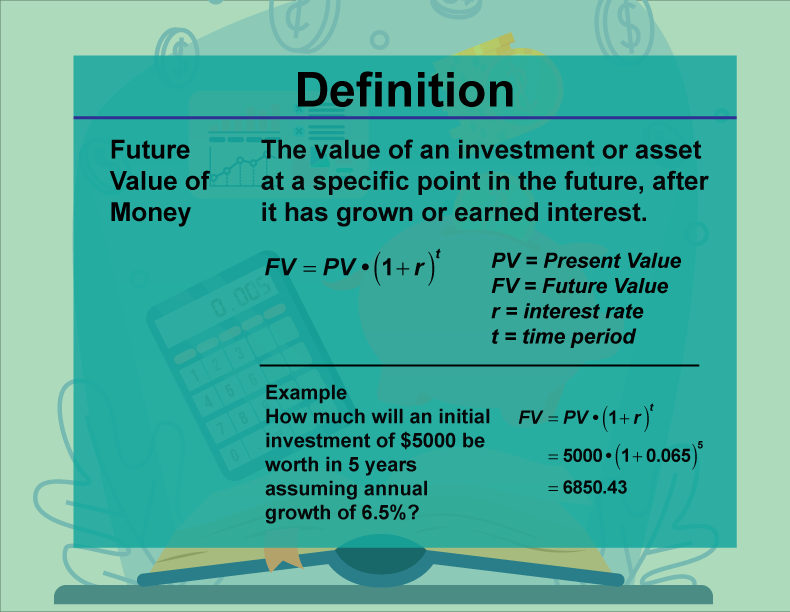

Future Value is a calculation that determines the value of a current asset or a series of cash flows at a specified date in the future. It assumes a specific rate of growth, often referred to as the interest rate or the discount rate. For an investor, FV answers the fundamental question: “If I put a certain amount of money to work today, how much will I have in five, ten, or thirty years?”

The concept applies to various financial instruments, including savings accounts, bonds, stocks, and even real estate. By calculating the FV, an individual can move beyond guesswork and begin to build a data-driven financial plan that accounts for the passage of time and the power of productivity.

The Core Principle: The Time Value of Money

The reason FV is such a critical metric is rooted in the Time Value of Money (TVM). This principle states that a dollar available today is worth more than a dollar promised in the future. There are three primary reasons for this:

- Opportunity Cost: Money held today can be invested to earn interest or capital gains. By choosing to receive money later, you forgo the earnings that could have been generated in the interim.

- Inflation: Over time, the purchasing power of currency tends to decline. A dollar in twenty years will likely buy fewer goods and services than a dollar today.

- Risk: There is always a level of uncertainty regarding future payments. Receiving money today eliminates the “default risk” associated with waiting for a future date.

The Mechanics of FV: Formulas and Variables

To accurately calculate Future Value, one must understand the variables involved and how they interact. The math of FV is a testament to the power of exponential growth, which is the engine behind most successful wealth-building strategies.

Simple Interest vs. Compound Interest

There are two primary ways that value grows over time: simple and compound interest.

- Simple Interest: This is calculated only on the initial principal. If you invest $1,000 at 5% simple interest for three years, you earn $50 each year, resulting in an FV of $1,150.

- Compound Interest: This is where the true power of FV lies. Compound interest is calculated on the initial principal plus the accumulated interest from previous periods. In the same scenario above, the $50 earned in the first year would itself earn interest in the second year. Over long periods, compounding creates a “snowball effect” that significantly outperforms simple interest.

Breaking Down the Future Value Formula

The standard formula for calculating the Future Value of a lump sum is:

FV = PV × (1 + r)^n

Where:

- FV: Future Value

- PV: Present Value (the initial amount of money)

- r: The interest rate or rate of return (per period)

- n: The number of periods (usually years)

For example, if you invest $10,000 (PV) at an annual interest rate of 7% (r = 0.07) for 20 years (n = 20), the formula would be $10,000 × (1.07)^20. This results in a Future Value of approximately $38,696.84. This formula demonstrates how the variable “n” (time) acts as an exponent, meaning that the longer you leave your money invested, the more dramatically the FV grows.

The Impact of Compounding Frequency

The frequency with which interest is compounded—whether annually, semi-annually, quarterly, or even daily—can significantly alter the FV. The more frequently interest is added to the principal, the faster the total balance grows. If you are comparing two savings accounts with the same nominal interest rate, the one that compounds daily will yield a higher FV than the one that compounds annually. In professional finance, this is known as the Effective Annual Rate (EAR).

Why Future Value Matters for Personal Finance and Investing

Understanding FV is not just an academic exercise; it is a practical tool used by successful investors to make informed decisions and stay disciplined during market fluctuations.

Retirement Planning and Goal Setting

The most common application of FV is in retirement planning. Most people have a “target number” they wish to reach before they stop working. By using FV calculations, you can determine how much you need to save each month to reach that goal. For instance, if you know you need $1.5 million in 30 years, and you expect an 8% average annual return, FV helps you reverse-engineer your current savings strategy. It transforms a vague hope into a concrete, mathematical roadmap.

Evaluating Investment Opportunities

When presented with different investment options, FV provides a standardized way to compare them. Suppose you are choosing between a low-risk bond paying 4% and a diversified stock portfolio that might return 9%. By projecting the FV of both options over a 10-year horizon, you can clearly visualize the “cost” of safety. FV allows investors to weigh the trade-off between risk and reward by showing the tangible difference in end-state wealth.

Inflation: The Silent Eroder of Future Value

While FV tells you how much money you will have, it is equally important to consider what that money will actually buy. Professional financial planners often distinguish between Nominal Future Value (the actual dollar amount) and Real Future Value (the value adjusted for inflation). If your investment grows by 7% but inflation is 3%, your “real” growth rate is effectively 4%. High-level financial strategy involves targeting an FV that exceeds the projected rate of inflation to ensure that your future wealth maintains its purchasing power.

Practical Tools and Methods for Calculating FV

In the modern era, you don’t need to be a mathematician to utilize Future Value. Various tools make these complex calculations accessible to everyone from retail investors to corporate CFOs.

Financial Calculators and Spreadsheet Functions

For those who prefer a digital approach, software like Microsoft Excel or Google Sheets offers built-in functions to handle these equations. The formula =FV(rate, nper, pmt, [pv], [type]) is a standard tool in business.

- Rate: The interest rate per period.

- Nper: The total number of payment periods.

- Pmt: The payment made each period (used for annuities).

- PV: The present value or lump sum.

This functionality is particularly useful for calculating the FV of an annuity, which is a series of equal payments made at regular intervals (like contributing $500 to an IRA every month).

The Rule of 72: A Quick Estimation Tool

For a fast mental calculation without a computer, investors often use the “Rule of 72.” This is a simplified way to estimate how long it will take for an investment to double in value (i.e., for the FV to be 2x the PV). By dividing 72 by the annual rate of return, you get the approximate number of years required for doubling. For example, at a 6% return, your money will double in roughly 12 years (72 / 6 = 12). This shorthand is an excellent way to conceptualize FV during high-level financial discussions.

Conclusion: Leveraging FV for Long-Term Wealth

In the final analysis, “FV” is more than just a financial term—it is a perspective. It encourages individuals to look beyond the immediate gratification of spending and consider the long-term potential of their capital. By understanding that every dollar saved today is an investment in a much larger future sum, investors can cultivate the patience and discipline required for wealth accumulation.

Mastering Future Value allows you to take control of your financial destiny. It provides the clarity needed to navigate complex choices, from choosing the right retirement account to evaluating a business expansion. In a world of economic uncertainty, the ability to mathematically project the growth of your assets is perhaps the most powerful tool an investor can possess. Whether you are just starting your career or are well on your way to financial independence, keeping your eyes on the FV ensures that your money is always working as hard as you are.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.