In the world of personal finance and automotive investment, the term “Cat S” frequently appears as a double-edged sword. For the uninitiated, stumbling upon a high-end vehicle listed at a fraction of its market value might seem like a financial windfall. However, these vehicles often carry the “Cat S” designation—a marker that carries significant implications for a buyer’s wallet, insurance premiums, and long-term asset value.

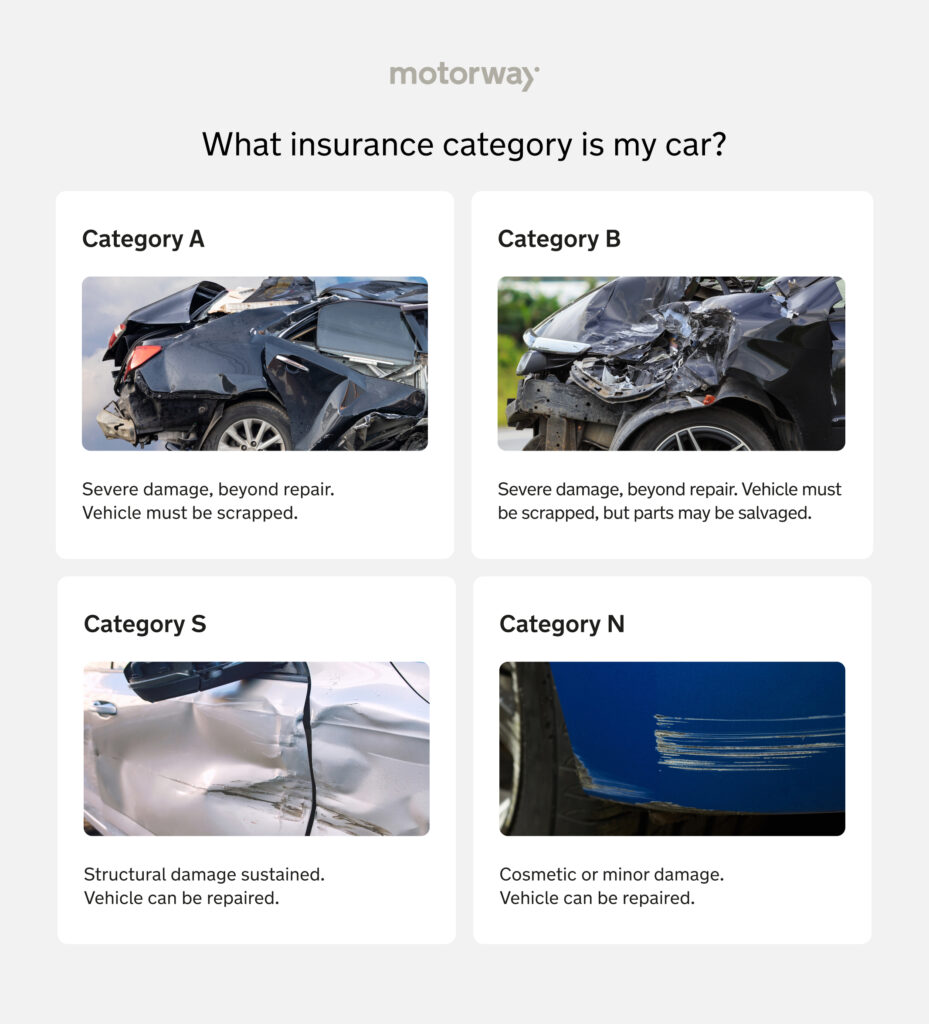

The classification of “Cat S” (formerly known as Category C) is a designation used by insurance companies to describe the status of a vehicle that has been written off but is technically repairable. Understanding exactly what this means from a financial perspective is crucial for anyone looking to optimize their personal balance sheet or navigate the complex secondary car market.

What is a Cat S Vehicle? Defining the Financial and Structural Implications

To understand the financial risk or reward of a Cat S car, one must first understand the technical definition. Since the Association of British Insurers (ABI) updated their salvage code in 2017, the focus shifted from the cost of repair to the nature of the damage.

The Shift from Category C to Category S

Historically, cars were classified based on the math: if the repair cost exceeded the vehicle’s value, it was a “Cat C.” The modern “Cat S” stands for Structural. This means the vehicle has sustained damage to its structural frame—the chassis, the crumple zones, or the pillars—but is deemed repairable. From a financial standpoint, the insurance company has decided that the “Total Loss” payout is more economically viable for them than paying for a complex structural repair.

Structural Integrity vs. Cosmetic Damage

The distinction between Cat S (Structural) and Cat N (Non-structural) is where many investors find their risk threshold. While a Cat N vehicle might have suffered electrical faults or bumper damage, a Cat S vehicle has had its “skeleton” compromised. For the budget-conscious buyer, this represents a significant “entry price” discount, but it also introduces the financial burden of ensuring the structural repair meets safety standards, which can be an expensive endeavor.

The Economics of Buying a Cat S Car: Is it a Sound Investment?

When analyzing a Cat S vehicle as a financial asset, the primary allure is the initial capital outlay. However, savvy investors know that the purchase price is only one variable in a complex equation of depreciation and maintenance.

Initial Purchase Savings and Capital Allocation

The most immediate benefit of a Cat S vehicle is the price tag. Typically, these cars trade at 30% to 50% below their “clean title” market value. For a buyer with limited liquid capital, this allows for the acquisition of a higher-tier model than they could otherwise afford. If you are looking at a vehicle as a utility tool rather than a speculative asset—meaning you intend to drive it until it has zero value—the “saving” is realized immediately upon purchase.

Calculating the Total Cost of Ownership (TCO)

In personal finance, we must look at the Total Cost of Ownership. With a Cat S car, the TCO includes:

- Independent Inspection Costs: You should never buy a Cat S vehicle without a professional structural report (such as those from the AA or RAC).

- Increased Maintenance: Structural repairs can lead to secondary issues, such as uneven tire wear due to alignment problems or persistent sensor errors.

- The “Stigma” Discount: You save 40% when you buy, but you must accept that you will likely have to sell it for 40% less than the market rate later. This is a “wash” in terms of percentage, but it limits your pool of potential buyers.

Insurance and Financing Challenges for Cat S Vehicles

One of the biggest hurdles in the financial lifecycle of a Cat S vehicle is the recurring cost of insurance and the difficulty of securing traditional financing.

Navigating Higher Premiums and Limited Choice

Insurance companies are in the business of risk assessment. A vehicle that has had its structural integrity compromised is viewed as a higher risk, not necessarily because it is more likely to crash, but because its performance in a second accident is unpredictable.

- The Premium Hike: Many mainstream insurers will either refuse to cover Cat S vehicles or will charge significantly higher premiums.

- Agreed Value Policies: Owners often have to seek out specialist insurers who offer “agreed value” policies to ensure that, in the event of another total loss, they aren’t reimbursed at a pittance. From a money management perspective, the higher monthly premium can quickly erode the initial savings gained at the time of purchase.

Securing Loans for Salvage Title Cars

If you are planning to finance a Cat S vehicle through a traditional bank loan or Hire Purchase (HP) agreement, you will likely face roadblocks. Most lenders require the vehicle to serve as collateral. Because a Cat S vehicle has a volatile and lower resale value, banks view it as “poor collateral.”

- Interest Rates: If you do find a lender willing to finance a Cat S car, the interest rates are often higher to compensate for the risk.

- Cash is King: Consequently, Cat S vehicles are best suited for cash buyers who don’t need to leverage debt to make the purchase, thereby avoiding the high interest rates associated with sub-prime automotive lending.

Resale Value and Exit Strategies: Managing Your Financial Asset

An essential part of financial planning is the “exit strategy.” How do you get your money back out of an asset when you are finished with it?

Transparency and Legal Obligations

When selling a Cat S vehicle, you are legally and ethically obligated to disclose its status. Failing to do so can lead to legal repercussions and financial penalties. From a marketing standpoint, this means your “exit” will take longer. You aren’t just selling a car; you are selling the quality of the repair.

- Documentation as Value: Keeping a comprehensive portfolio of the repair process, including “before and after” photos and invoices from certified structural engineers, is vital. This documentation helps mitigate the “stigma” discount and can help you claw back some of the resale value.

Finding the Right Buyer in the Secondary Market

The market for Cat S vehicles is niche. You will likely be selling to:

- Budget-conscious commuters: People looking for the cheapest possible transport.

- Mechanically inclined individuals: Those who understand the repairs and aren’t intimidated by the designation.

- Part-exchange/Trade-in: Be warned that many main dealerships will refuse to take a Cat S car in part-exchange, or they will offer a “scrap” value for it. This significantly limits your options for upgrading in the future, often forcing a private sale which takes more time and effort.

Conclusion: Making an Informed Financial Decision

Deciding to purchase or invest in a Cat S vehicle is not a decision to be made lightly. From a pure money management perspective, it is a high-risk, potentially high-reward strategy.

If your goal is to minimize your upfront capital expenditure and you plan to keep the vehicle for a decade or more, the Cat S designation offers a path to luxury or high-performance vehicles that would otherwise be out of reach. In this scenario, the “depreciation” has already happened, and you are the beneficiary of the insurance company’s risk-aversion.

However, if you are someone who changes cars every two to three years, or if you rely on traditional financing and mainstream insurance, the “hidden” costs of a Cat S vehicle will likely outweigh the initial savings. The higher insurance premiums, the difficulty in securing a loan, and the struggle to find a buyer at a fair price during the exit phase can turn a “bargain” into a financial burden.

Ultimately, the meaning of “Cat S” in the world of finance is “Due Diligence.” It represents a vehicle that requires a deeper level of investigation, a more robust insurance strategy, and a realistic expectation of its future worth. By approaching a Cat S listing with a calculator and a critical eye, you can determine if the structural discount aligns with your long-term financial goals.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.