The financial landscape is constantly evolving, and understanding its terminology is key to making informed decisions, whether you’re managing personal finances, building a business, or leveraging technology for income. Among the many concepts that can appear complex, “capitalised interest” stands out. It’s a term that surfaces in various contexts, from student loans to business financing, and its implications can significantly impact your financial trajectory. In essence, capitalised interest refers to interest that has been added to the principal amount of a loan or debt, subsequently earning more interest. This article will delve into the meaning of capitalised interest, its implications across different financial scenarios, and how it intersects with the broader themes of technology, branding, and money management that define our modern digital economy.

Unpacking the Definition: Beyond Simple Interest Accumulation

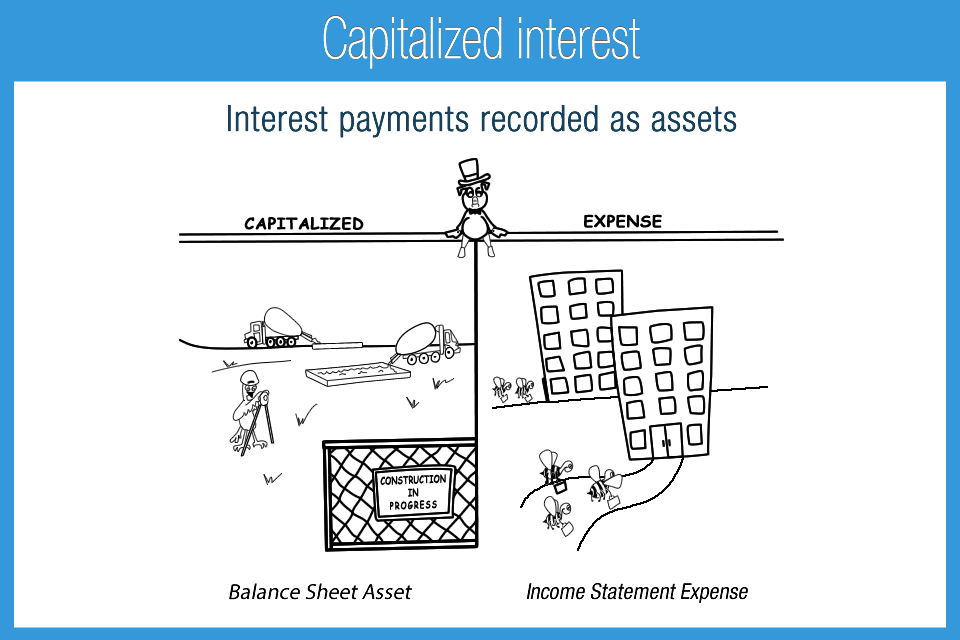

At its core, capitalised interest is the process by which unpaid interest on a loan is added to the outstanding principal balance. Instead of paying this interest separately, it becomes part of the debt itself. From that point forward, this newly increased principal accrues its own interest. This can create a snowball effect, often referred to as “interest on interest,” leading to a higher total repayment amount over the life of the loan than if the interest had been paid as it accrued.

To truly grasp this, let’s consider a simplified example. Imagine you have a loan with a principal of $10,000 and an annual interest rate of 5%. If you don’t make any payments for a year, the interest accrued would be $500. Without capitalization, this $500 would remain a separate amount owed. However, with capitalization, this $500 is added to your principal, making your new outstanding balance $10,500. The next year, interest will be calculated on this $10,500, not the original $10,000. This distinction is crucial because it means the total amount you repay will be higher.

The Mechanics of Capitalization: When and How Does it Happen?

Capitalisation isn’t a random occurrence; it typically happens under specific circumstances, often dictated by loan agreements and borrower actions (or inactions). Understanding these triggers is vital for avoiding unwelcome increases in debt.

Deferment and Forbearance: Temporary Relief with Potential Consequences

One of the most common scenarios where capitalised interest comes into play is during periods of loan deferment or forbearance. Deferment allows borrowers to temporarily postpone loan payments, while forbearance grants a similar reprieve but often with less strict eligibility requirements and sometimes with accrued interest continuing to accumulate.

During deferment, interest may or may not accrue, depending on the type of loan. For instance, on unsubsidised federal student loans, interest continues to accrue even during deferment. If this accrued interest isn’t paid off before the deferment period ends, it can be capitalised. This means that when you resume making payments, your principal will be higher, and consequently, your monthly payments and the total interest paid over time will increase.

Forbearance, while offering a pause on payments, often allows interest to accrue. If these accrued interest amounts are not paid during the forbearance period, they are frequently capitalised once the forbearance ends. This is a critical point for borrowers to understand, as the perceived “relief” of skipping payments can lead to a larger debt burden down the line if the accumulated interest isn’t managed proactively.

Loan Consolidation and Refinancing: A Double-Edged Sword

Loan consolidation and refinancing, often employed to simplify payments or secure better interest rates, can also lead to the capitalization of interest. When you consolidate multiple loans into a single new loan, any unpaid interest from the original loans is typically added to the principal of the new consolidated loan. Similarly, when refinancing a loan, the outstanding balance, which might include accrued but unpaid interest, is often rolled into the new loan.

While these processes can be beneficial for managing debt, borrowers must be aware of how interest capitalization affects the overall cost. A slightly lower interest rate on a refinanced loan might be offset by the inclusion of previously accrued interest into the principal, potentially leading to a longer repayment period or higher total interest paid.

Default and Delinquency: The Unavoidable Outcome

In cases of loan default or prolonged delinquency, lenders often have the right to capitalise accrued interest. This is because the borrower has failed to meet their contractual obligations, and the lender seeks to recoup their losses, including the interest that should have been paid. This can drastically escalate the amount owed, making it even more challenging for the borrower to get back on track.

The Impact of Capitalised Interest: A Multifaceted Financial Effect

The implications of capitalised interest extend far beyond a simple arithmetic increase in debt. They touch upon cash flow, long-term financial planning, and even the accessibility of future credit.

Increased Total Repayment: The Most Direct Consequence

The most immediate and significant impact of capitalised interest is the increase in the total amount of money a borrower will have to repay over the life of the loan. This is due to the compounding effect of interest on interest. Even a seemingly small amount of capitalised interest can grow substantially over years, especially on long-term loans.

Higher Monthly Payments: A Strain on Immediate Cash Flow

When the principal amount of a loan increases due to capitalised interest, it generally leads to higher monthly payments. Lenders recalculate your payment based on the new, larger principal and the remaining loan term. This can place a considerable strain on a borrower’s immediate cash flow, making it harder to meet other financial obligations.

Extended Loan Terms: A Lingering Debt

In some cases, particularly with student loans, capitalised interest might not immediately result in higher monthly payments but can extend the loan term. This means you’ll be making payments for a longer period, and while the immediate financial pressure might be less, the cumulative interest paid over the extended term can still be significant.

Reduced Financial Flexibility: A Hindrance to Future Goals

A higher debt burden due to capitalised interest can limit a borrower’s financial flexibility. This might mean delaying major life events like buying a home, starting a family, or pursuing further education. It can also affect one’s ability to save for retirement or build an emergency fund, impacting long-term financial security.

Navigating Capitalised Interest in the Digital Age: Tech, Branding, and Strategic Money Management

The principles of understanding capitalised interest are amplified and intertwined with the realities of the digital economy. Technology offers new tools for managing finances, while brand perception plays a role in accessing financial products, and strategic money management is more crucial than ever.

Leveraging Technology for Financial Awareness and Control

The same technologies that drive innovation in AI, apps, and digital security can be powerful allies in understanding and managing capitalised interest.

- Budgeting and Financial Planning Apps: Modern apps offer sophisticated tools to track loan balances, interest accrual, and potential capitalization points. By integrating loan information, these apps can provide proactive alerts when interest is about to be capitalised, allowing borrowers to make payments to avoid it. Features that simulate loan payoffs and illustrate the impact of capitalization can be invaluable for financial education.

- AI-Powered Financial Advisors: Emerging AI tools can analyze loan portfolios, identify opportunities to reduce interest costs, and advise on strategies to prevent capitalization. These tools can offer personalized insights, helping borrowers make informed decisions about when to pay off accrued interest, consolidate loans, or manage deferment periods effectively.

- Digital Security for Financial Data: As more financial interactions occur online, robust digital security becomes paramount. Protecting loan information and online banking credentials is essential to prevent unauthorized transactions that could lead to unintentional capitalization or financial distress.

- Online Calculators and Simulators: A plethora of free online calculators can help visualize the impact of capitalised interest. These tools allow users to input loan details and interest rates to see how capitalization will affect their total repayment and monthly payments, fostering a deeper understanding of the financial consequences.

Branding Your Financial Approach: Reputation and Trust in Financial Markets

While “capitalised interest” might not directly relate to personal branding in the traditional sense, the concept of your financial reputation or “brand” is critical in accessing and managing financial products.

- Creditworthiness and Lender Trust: A history of managing debt responsibly, which includes understanding and avoiding adverse financial events like excessive capitalised interest, builds a strong financial reputation. This trust translates into better interest rates, more favorable loan terms, and easier access to credit when needed, whether for personal investments or business ventures.

- Corporate Identity and Business Finance: For businesses, understanding how capitalised interest impacts financing is crucial for their financial health and strategic planning. A company’s ability to manage its debt effectively contributes to its overall financial brand and investor confidence. Poor debt management, including the accumulation of capitalised interest, can damage a business’s reputation and hinder its growth.

- Personal Branding as a Financial Savvy Individual: Developing a personal brand that signifies financial responsibility and savvy can be advantageous. This means demonstrating an understanding of financial concepts like capitalised interest, making informed decisions, and communicating effectively with financial institutions.

Strategic Money Management: Proactive Prevention and Informed Decision-Making

Understanding capitalised interest is a cornerstone of proactive and strategic money management, especially in an era where online income streams and side hustles are common.

- Prioritizing Interest Payments: For loans where interest capitalisation is a risk, strategically prioritizing payments to cover accrued interest before it’s added to the principal can be a highly effective strategy. This requires careful budgeting and a clear understanding of your loan terms.

- Evaluating Loan Consolidation and Refinancing Carefully: When considering consolidation or refinancing, always scrutinize the terms. Understand precisely how accrued interest will be handled and use financial tools to model the total cost of the new loan, comparing it to the current one. Don’t be swayed solely by a lower advertised interest rate if it masks a higher overall repayment due to capitalization.

- Maximizing Income and Minimizing Debt: The pursuit of online income and side hustles can provide the necessary capital to make timely interest payments or lump-sum payments that reduce the principal, thereby mitigating the risk of capitalization. Conversely, minimizing unnecessary debt reduces the opportunities for interest to accumulate and capitalize.

- Understanding Student Loan Options: For students and recent graduates, the nuances of federal student loan repayment plans, including how interest is handled during in-school periods, grace periods, and deferments, are critical. Capitalised interest on student loans can significantly increase the burden, so understanding options like income-driven repayment plans and the benefits of paying interest as it accrues is vital.

Conclusion: Empowering Your Financial Future

Capitalised interest is not merely a technical financial term; it’s a concept with tangible consequences that can significantly impact your financial well-being. By understanding its definition, the circumstances under which it occurs, and its far-reaching effects, you can take proactive steps to manage your debt effectively. In the digital age, where technology offers powerful tools for financial management and where your financial reputation carries weight, a thorough comprehension of capitalised interest empowers you to make informed decisions, optimize your financial strategies, and ultimately build a more secure and prosperous future. Whether you are managing personal finances, navigating business loans, or exploring online income opportunities, mastering the intricacies of capitalised interest is an investment in your financial literacy and a crucial step towards achieving your financial goals.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.