Navigating the complexities of a credit report can often feel like deciphering a foreign language. Among the various notations, “Closed Account” is one that frequently causes confusion and anxiety for consumers. Whether you initiated the closure yourself or your lender decided to terminate the relationship, seeing this status on your credit report can leave you wondering about the immediate and long-term implications for your financial standing.

In the realm of personal finance, your credit report is your digital reputation. Understanding the nuances of closed accounts—how they happen, how they influence your credit score, and how long they linger—is essential for anyone looking to build or maintain a robust financial profile. This article provides an in-depth exploration of what a closed account signifies and how it interacts with the algorithms that determine your creditworthiness.

Understanding Why Accounts Close

An account doesn’t simply disappear when it is closed; instead, its status is updated to reflect that it is no longer active for new transactions. The “why” behind the closure is often noted in the report’s remarks section, and the reason matters significantly for your financial narrative.

Voluntary Closure (Consumer-Initiated)

The most common reason for an account closure is that the consumer requested it. You might decide to close a credit card because it carries a high annual fee, you no longer use the service, or you want to simplify your financial life. When you initiate the closure, the report usually states “Account closed at consumer’s request.” While this sounds benign, it still triggers various mechanical changes in your credit score calculation.

Involuntary Closure (Issuer-Initiated)

Sometimes, a lender decides to close an account without the consumer’s request. This often happens due to “inactivity.” If you have a credit card that hasn’t been used in 12 to 24 months, the bank may see it as a liability or an unprofitable account and shut it down. Other reasons include “adverse action” due to a drop in your credit score elsewhere, or a violation of the terms of service. While “Closed by Grantor” doesn’t inherently lower your score more than a voluntary closure, it can be a red flag to future lenders who might wonder if you were a risky borrower.

Account Paid in Full and Terminated

For installment loans—such as auto loans, mortgages, or student loans—the account is automatically closed once the final payment is made. This is a positive milestone. It indicates that you have fulfilled your contractual obligation. Unlike revolving credit (credit cards), closing an installment loan through successful repayment is generally viewed favorably, though it may result in a minor, temporary dip in your score due to changes in your credit mix.

The Impact of a Closed Account on Your Credit Score

Many consumers are surprised to see their credit score drop immediately after closing an account. This happens because credit scoring models, like FICO and VantageScore, look at several variables that are directly altered when an account status changes from “Open” to “Closed.”

Credit Utilization Ratio (The Immediate Impact)

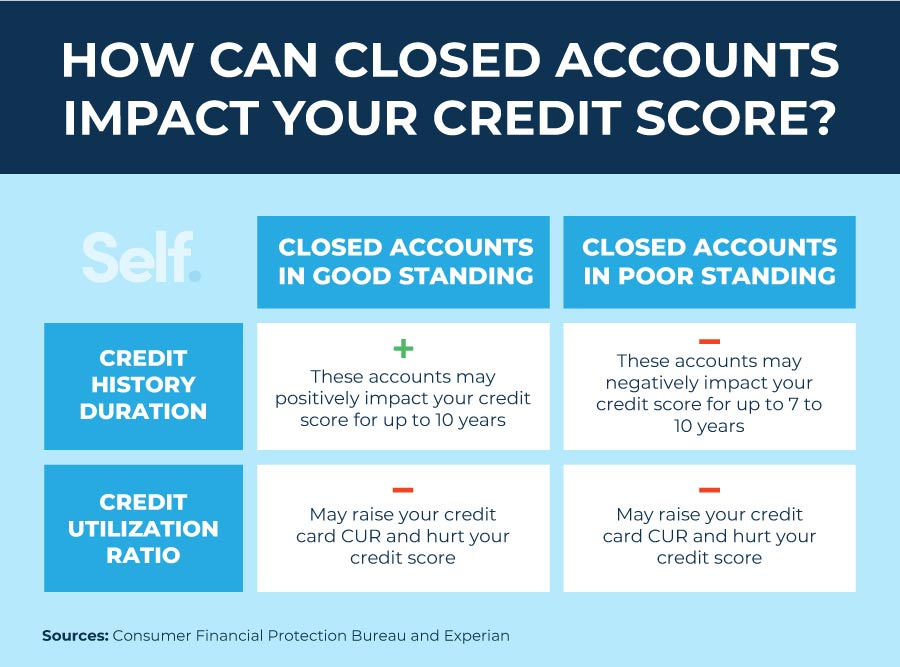

The most significant immediate impact of closing a revolving credit account is on your credit utilization ratio. This ratio compares how much credit you are using to your total available credit limit. For example, if you have two credit cards with $5,000 limits each (total $10,000) and you owe $2,000 on one, your utilization is 20%. If you close the unused card, your total available credit drops to $5,000, and your utilization instantly jumps to 40%. Since utilization accounts for roughly 30% of your FICO score, this spike can cause a noticeable decline in your points.

Average Age of Accounts (The Long-Term Impact)

The “Length of Credit History” accounts for about 15% of your credit score. Many people believe that closing an account removes its age from the calculation immediately. Fortunately, that is not entirely true. Under the FICO model, a closed account in good standing remains on your report for 10 years and continues to contribute to your average age of accounts. However, once that 10-year mark passes and the account falls off the report, you may see a drop in your score because your average credit age will suddenly decrease.

Credit Mix and Diversity

Lenders like to see that you can manage different types of credit responsibly, including revolving accounts (cards) and installment accounts (loans). If you close your only credit card or finish paying off your only installment loan, your “credit mix” becomes less diverse. This represents about 10% of your score. While it is never wise to keep a loan just for the sake of a score, losing that diversity can lead to a slight reduction in your overall rating.

How Long Do Closed Accounts Stay on Your Credit Report?

A closed account is not a permanent fixture, but it doesn’t vanish overnight. The duration it remains on your report depends entirely on the “flavor” of the account at the time of closure.

Positive Accounts vs. Negative Accounts

The credit bureaus (Equifax, Experian, and TransUnion) treat positive history differently than negative history. If an account was closed with no late payments and a $0 balance, it is considered a “positive” account. If it was closed because of delinquency, default, or was “charged off,” it is a “negative” account.

The 10-Year Rule for Positive History

To reward consumers for long-term responsible behavior, the credit bureaus keep positive closed accounts on your file for 10 years from the date of closure. This is beneficial because it preserves the “age” of your credit history. During this decade, the account continues to bolster your score, showing future lenders that you have a track record of successful account management.

The 7-Year Rule for Negative Records

If an account was closed and contained negative information—such as late payments or a collection status—it will typically stay on your credit report for seven years. This follows the guidelines of the Fair Credit Reporting Act (FCRA). The seven-year clock usually starts from the date of the first delinquency that led to the account being closed. The silver lining here is that as the negative information ages, its impact on your score diminishes, and eventually, it is purged entirely, allowing your score to recover.

Strategic Considerations Before Closing an Account

In the world of personal finance, most experts advise against closing old credit card accounts unless there is a compelling reason to do so. However, there are strategic moments where closing an account is the right move.

When It Makes Sense to Close an Account

There are three primary scenarios where closing an account is logical:

- Expensive Annual Fees: If a card costs $500 a year and you no longer use the travel perks or rewards that justify that cost, the financial drain of the fee outweighs the small benefit to your credit score.

- Overspending Temptation: If having a high credit limit encourages impulsive spending that leads to high-interest debt, closing the account is a healthy move for your overall financial well-being.

- Divorce or Separation: It is often necessary to close joint accounts during a legal separation to prevent one party from incurring debt that the other is legally responsible for.

Alternatives to Closing a Credit Card

Before you pull the trigger on closing a card, consider a “Product Change.” Most major issuers allow you to “downgrade” a card with a high annual fee to a no-fee version within the same “family” of cards. This allows you to keep the account number, the credit limit, and the age of the account intact while eliminating the annual cost. Another alternative is to simply keep the card in a drawer and use it once every six months for a small purchase to prevent the issuer from closing it due to inactivity.

Navigating Common Myths and Misconceptions

There is a significant amount of misinformation regarding closed accounts. Clarifying these myths can help you make better financial decisions.

Does Closing an Account Remove Late Payment History?

A common misconception is that closing an account “wipes the slate clean.” This is false. If you have late payments on a credit card and you close it, the account status will change to “Closed,” but the history of late payments will remain visible for seven years. Closing the account does not hide past mistakes; it only prevents you from making new ones on that specific line of credit.

Will My Score Rebound Automatically?

If your score drops because of a closed account (usually due to the utilization spike mentioned earlier), it won’t “bounce back” unless you take action. To recover those points, you generally need to pay down balances on your other remaining cards to bring your total utilization back down to below 30% (ideally below 10%). The score reflects your current risk, and until your available credit increases or your debt decreases, the score will likely remain at its new, lower level.

In conclusion, a closed account on your credit report is a neutral event that can have positive or negative ripple effects depending on your overall credit profile. By understanding the mechanics of utilization, account age, and reporting timelines, you can manage your credit accounts strategically. Remember: your credit report is a living document. While a closed account marks the end of one financial chapter, how you manage your remaining active accounts will always be the most important factor in your financial narrative.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.