For many taxpayers, the arrival of tax season is met with a mix of anxiety and anticipation. The prospect of a tax refund represents more than just a return of overpaid taxes; for many households, it is the largest single financial windfall of the year. While the IRS “Where’s My Refund?” tool provides a basic progress bar, savvy taxpayers often turn to their official IRS tax transcripts for a more granular view of their filing status. On these transcripts, one specific alphanumeric string carries more weight than any other: Transaction Code 846.

Understanding what Code 846 means, how it impacts your liquidity, and how to strategically manage the resulting capital is a cornerstone of proactive personal finance. This guide explores the technical meaning of Code 846, the timeline for fund disbursement, and how to utilize your refund to strengthen your overall financial position.

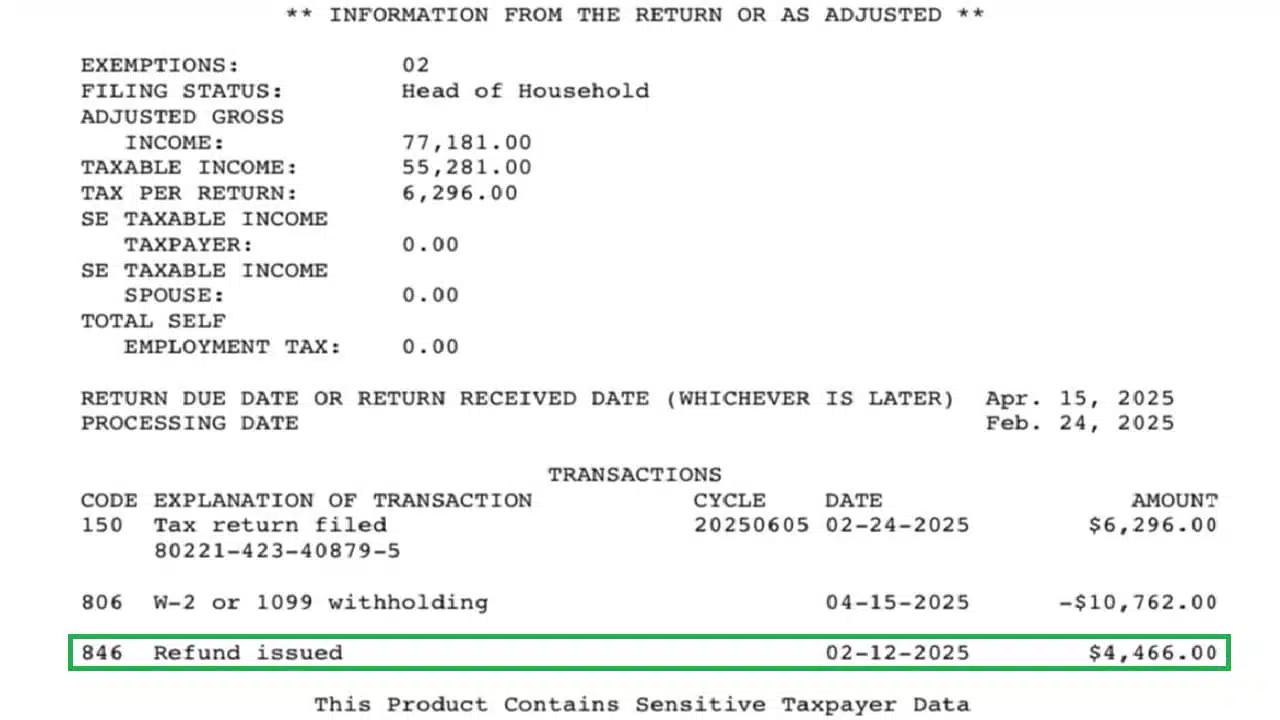

Decoding the IRS Transcript: What is Transaction Code 846?

The IRS uses a series of three-digit transaction codes (TC) to track every action taken on a taxpayer’s account. These codes act as a specialized language for tax professionals and internal auditors. While codes like 150 (Tax Return Filed) or 806 (W-2 Withholding) are part of the processing journey, Code 846 is the destination.

The Language of the IRS

In the world of federal taxation, “Code 846” is the official designation for “Refund Issued.” When this code appears on your transcript, it indicates that the IRS has finished processing your return, calculated your overpayment, and authorized the Treasury Department to release the funds. It is the final green light in the administrative process.

Unlike the “Where’s My Refund?” portal, which may lag by several days, the tax transcript is the internal record of truth. If you see Code 846, the bureaucracy has concluded its review, and your refund is officially in the queue for disbursement.

Why Code 846 is the “Golden Ticket”

For those managing tight budgets or planning significant investments, Code 846 provides a level of certainty that other statuses do not. Until this code appears, your return could still be subject to “Code 570” (Account Action Pending) or “Code 420” (Examination Indicator/Audit). The appearance of 846 signals that any holds have been cleared and the math has been verified. It transforms an expected asset into an active cash inflow, allowing for concrete financial scheduling.

Locating the Code on Your Transcript

To find this code, taxpayers must access their “Record of Account” or “Account Transcript” through the IRS.gov website. Under the “Transactions” section, you will see a list of codes. You are looking for “846” in the left-hand column, followed by the description “Refund issued.” Crucially, next to this code, you will find a date. This is the “cycle date” or the authorized date for the release of your funds.

The Financial Impact: When Will You See the Money?

Once Code 846 is visible, the next logical question is one of timing. While the IRS provides a date next to the code, the actual arrival of the money in your bank account depends on the delivery method and your financial institution’s processing speed.

Refund Issue Date vs. Deposit Date

The date listed next to Code 846 is the day the IRS sends the payment instruction to the Bureau of the Fiscal Service. If you opted for direct deposit, the funds are typically transmitted on that specific date. However, banking systems do not operate instantaneously. Most major banks may hold the funds for 1–3 business days as they process the incoming Automated Clearing House (ACH) transfer.

Direct Deposit vs. Paper Check Timelines

The disparity between digital and physical delivery is significant. If your Code 846 is associated with a direct deposit, you can generally expect the funds within a week of the transcript date. Conversely, if you requested a paper check, the 846 date represents the day the check is printed and handed to the United States Postal Service. Depending on mail speeds and your location, a paper check can take an additional 7–14 days to arrive. From a personal finance perspective, direct deposit remains the superior choice for maximizing the “time value” of your money.

![]()

Factors That Can Delay Your Funds

Even with a Code 846 present, certain external factors can cause a “last mile” delay.

- Banking Holidays: Federal holidays can push back ACH settlements.

- Incorrect Account Info: If the bank rejects the deposit due to an incorrect account number, the funds are sent back to the IRS, and a paper check is issued, adding weeks to the process.

- Refund Anticipation Loans (RALs): If you utilized a tax preparation service that deducts fees from your refund, the money goes to the preparer’s partner bank first, which then forwards the remainder to you. This can add a 24–48 hour delay.

Managing Your Windfall: Personal Finance Strategies for Tax Refunds

A tax refund is not a “bonus” from the government; it is an interest-free loan you provided to the Department of the Treasury throughout the year. When Code 846 appears, it marks the return of your capital. To maximize the utility of this money, it is essential to have a plan before the funds hit your account.

Prioritizing High-Interest Debt

The most mathematically sound use of a tax refund is the elimination of high-interest debt, specifically credit card balances. With average credit card APRs often exceeding 20%, using a $3,000 refund to pay down debt is the equivalent of “earning” a 20% guaranteed return on your investment. Using the “Debt Avalanche” method—targeting the highest interest rate first—can save you hundreds of dollars in future interest payments and improve your credit utilization ratio.

Building an Emergency Fund

If your high-interest debt is manageable, the next priority should be liquidity. Financial advisors typically recommend keeping 3–6 months of living expenses in a liquid, high-yield savings account (HYSA). If you currently have less than $1,000 in savings, your tax refund is the perfect tool to establish a “starter” emergency fund. This creates a buffer against future “financial shocks,” such as car repairs or medical bills, preventing you from falling back into high-interest debt cycles.

Strategic Investing for Long-Term Growth

For those with stable savings and low debt, the Code 846 refund represents an opportunity for wealth building.

- Roth IRA Contributions: If you haven’t hit your annual contribution limit, your refund can be diverted into a Roth IRA. This allows the money to grow tax-free, providing a double tax advantage.

- Brokerage Accounts: Investing in a low-cost S&P 500 index fund or a total market ETF allows your refund to participate in the growth of the economy.

- Education Savings: Contributing to a 529 plan for children or dependents can provide state tax benefits (in many states) while preparing for future tuition costs.

Troubleshooting Common Issues with Code 846

Sometimes, the appearance of Code 846 brings surprises—specifically regarding the amount of the refund. Understanding the potential for discrepancies is vital for accurate financial planning and budgeting.

What if the Amount Doesn’t Match?

If the amount listed next to Code 846 on your transcript is different from the amount you calculated on your Form 1040, the IRS has likely made a “math error adjustment.” This often happens due to errors in claiming the Child Tax Credit, the Earned Income Tax Credit (EITC), or discrepancies in reported income. The IRS will typically mail a notice (CP11, CP12, or CP13) explaining the change, but the Code 846 amount is what you will actually receive.

Offset Codes and Deductions

Your refund may be reduced by the Treasury Offset Program (TOP). If you owe back taxes, defaulted student loans, or past-due child support, the IRS is legally required to “offset” your refund to pay these debts. On your transcript, you would see Code 846 for the original amount, followed by a separate code (often 826 or 898) indicating the transfer of funds to another agency. From a money management perspective, it is important to check the Bureau of the Fiscal Service’s offset line if you suspect you may have outstanding federal or state liabilities.

Missing Refunds Despite the 846 Code

If the date on your Code 846 has passed and several weeks have elapsed without a deposit or a check, the refund may be lost or stolen. In this case, you can initiate a “refund trace.” This involves filing Form 3911 (Taxpayer Statement Regarding Refund) to help the IRS locate the disbursement. While rare, tracking this through your transcript allows you to act much faster than if you were simply waiting for the mail.

![]()

Conclusion: Turning a Code into Financial Progress

Transaction Code 846 is more than just a line on a government document; it is a signal of liquidity and a tool for financial advancement. By understanding the mechanics of the IRS transcript, taxpayers can move away from the “guessing game” of tax season and into a position of informed financial control.

Whether you use your refund to shore up your emergency fund, aggressively pay down debt, or invest in your retirement, the goal should be to ensure that these funds—your hard-earned money—work as hard for you as you did for them. As soon as you see that 846 code, the clock begins on your next financial move. Use it wisely to build a more secure and prosperous future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.