In the sophisticated world of personal finance and estate planning, the term “trustee” is often used, yet the weight and breadth of the role are frequently misunderstood. At its core, a trustee is a person or entity appointed to manage assets for the benefit of someone else. While the concept may sound simple, the execution involves a complex interplay of legal obligations, financial acumen, and ethical steadfastness. Whether you are establishing a trust, have been named a beneficiary, or are considering taking on the role of a trustee yourself, understanding the multi-faceted responsibilities of this position is essential for ensuring the long-term health of a financial legacy.

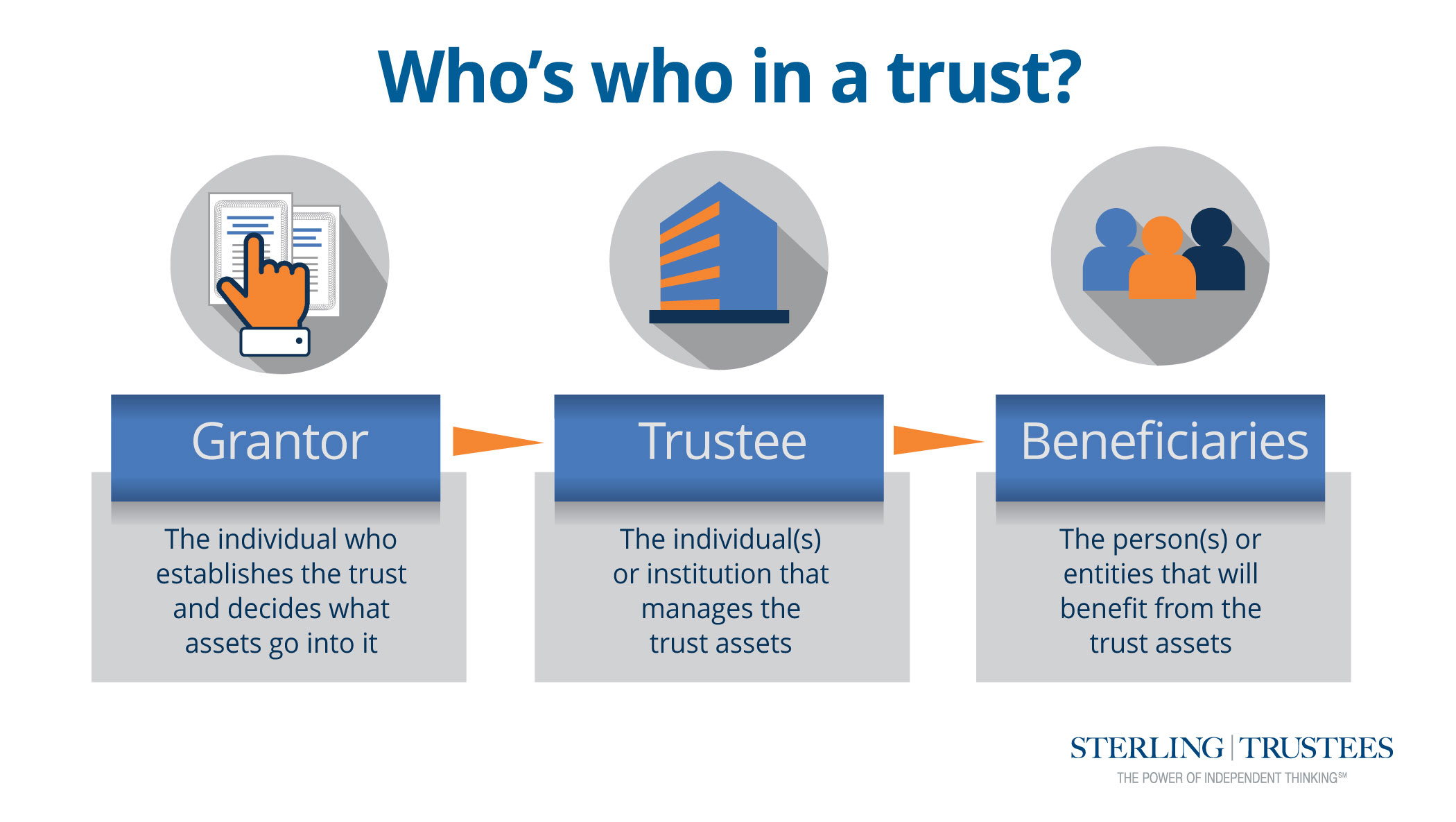

A trustee acts as the bridge between the grantor—the person who created the trust—and the beneficiaries—those who will eventually receive the assets. In the “Money” niche, the trustee is the ultimate financial steward, tasked with preserving capital, generating growth, and navigating the intricate world of tax law and investment strategy.

The Core Functions of a Trustee: Managing the Financial Engine

The primary responsibility of a trustee is the diligent management of the assets held within the trust. This is not a passive role; it requires active engagement with the financial markets, real estate, and sometimes even private business interests.

Asset Management and Investment Oversight

A trustee is responsible for the “Prudent Investor” standard. This means they must manage the trust’s portfolio with the same care and skill that a cautious professional would use. This involves creating a diversified investment strategy that aligns with the trust’s specific goals. If a trust is designed to provide for a beneficiary’s education over twenty years, the trustee might lean toward growth-oriented assets like equities. Conversely, if the trust is meant to provide immediate income for a surviving spouse, the trustee may focus on high-yield bonds or dividend-paying stocks. The trustee must constantly monitor these investments, rebalancing the portfolio as market conditions shift to ensure the risk profile remains appropriate.

Record Keeping and Financial Reporting

Transparency is the hallmark of a successful trustee. One of their most critical duties is the meticulous tracking of every penny that enters or leaves the trust. This includes interest dividends, capital gains, management fees, and distributions to beneficiaries. Trustees are typically required to provide an annual accounting to all “qualified beneficiaries.” These reports serve as a financial snapshot, proving that the trustee is acting in accordance with the trust’s instructions and the law. Without rigorous record-keeping, a trustee opens themselves up to significant legal liability and accusations of mismanagement.

Tax Compliance and Legal Obligations

Trusts are separate legal entities, and in the eyes of the IRS, they are often taxable. A trustee must ensure that the trust has its own Taxpayer Identification Number (TIN) and that all necessary tax returns—such as the federal Form 1041—are filed accurately and on time. Beyond income taxes, a trustee must also be aware of estate taxes, gift taxes, and generation-skipping transfer taxes. Managing the tax efficiency of a trust is one of the most direct ways a trustee can preserve wealth; by minimizing the “tax drag” on a portfolio, more capital remains available for the beneficiaries.

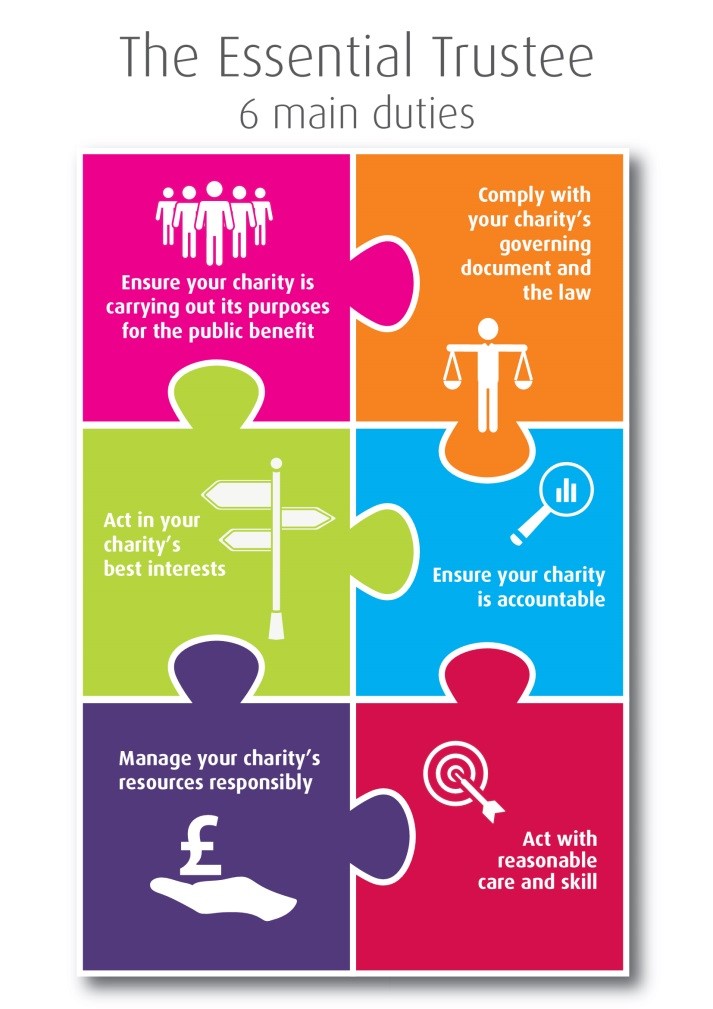

Fiduciary Duty: The Legal and Ethical Backbone

The word “trustee” is rooted in “trust,” and for a good reason. In the financial world, a trustee is a fiduciary—the highest standard of care recognized by the legal system. This means the trustee must always put the interests of the beneficiaries ahead of their own.

The Duty of Loyalty

The duty of loyalty is absolute. A trustee cannot use trust assets for their own personal gain, nor can they engage in “self-dealing.” For example, a trustee who is also a real estate agent cannot sell a piece of trust property and collect a personal commission unless explicitly authorized by the trust document. This duty ensures that the financial decisions made for the trust are motivated solely by what is best for the beneficiaries, rather than what might benefit the trustee’s own bank account or business interests.

The Duty of Care and Prudence

Under the duty of care, a trustee must act with “reasonable care, skill, and caution.” This is where the professional side of money management comes into play. If a trustee does not have the expertise to manage a complex portfolio of international stocks or commercial real estate, they have a duty to hire professionals—such as financial advisors, accountants, or attorneys—to assist them. Ignoring the portfolio or making reckless “get-rich-quick” bets with trust capital is a breach of this duty. Prudence requires a balance: the trustee must protect the principal while also seeking a reasonable return to combat inflation.

Avoiding Conflicts of Interest

A trustee must remain impartial. This can be particularly challenging in family situations where a trustee might be the sibling of one beneficiary and the parent of another. The trustee cannot favor one beneficiary over another unless the trust document specifically allows for it (e.g., a “sprinkle trust” where the trustee has discretion to give money to whoever needs it most). By maintaining a professional distance and adhering strictly to the written instructions of the trust, a trustee avoids the emotional and financial conflicts that often tear families apart during estate settlements.

Distributions and Beneficiary Relations

While managing the money is the “back-end” of the job, interacting with beneficiaries is the “front-end.” A trustee’s most visible role is deciding how and when to distribute funds.

Interpreting the Trust Document

Every trust comes with a set of “marching orders” written by the grantor. Some are very specific, stating that a beneficiary should receive $20,000 upon graduating from college. Others are “discretionary,” giving the trustee the power to decide how much money is needed for the beneficiary’s “health, education, maintenance, and support” (often referred to as the HEMS standard). The trustee must become an expert on the language of the trust document, ensuring that every distribution is legally defensible and aligns with the grantor’s original intent.

Balancing Competing Interests

One of the most difficult aspects of being a trustee is balancing the needs of current beneficiaries (income interest) with the needs of future beneficiaries (remainder interest). For instance, if a trust is set up to pay income to a widow for life, with the remaining assets going to her children later, the widow might want high-income investments. However, the children would prefer growth-oriented investments to ensure there is a large inheritance left for them. The trustee must navigate these competing financial desires, often making tough decisions that satisfy neither party perfectly but protect the long-term viability of the fund.

Communicating with Beneficiaries

Effective communication is the best defense against litigation. A proactive trustee keeps beneficiaries informed about the status of the trust’s assets and explains the reasoning behind distribution decisions. When a request for funds is denied, a professional trustee explains why based on the trust’s constraints. By treating beneficiaries with respect and providing clear financial information, the trustee builds a relationship of confidence that helps the trust function smoothly for decades.

Types of Trustees: Choosing the Right Financial Steward

When setting up a trust, one of the most significant financial decisions a grantor makes is who will serve as the trustee. This choice has a direct impact on the management fees, investment performance, and the overall longevity of the assets.

Individual vs. Corporate Trustees

An individual trustee is often a family member or a trusted friend. The advantage is that they know the family dynamics and usually don’t charge high fees. However, individuals may lack financial expertise and are subject to the “three Ds”: death, disability, or divorce, which can disrupt trust management.

On the other hand, a corporate trustee—such as a bank’s trust department or a specialized trust company—offers professional investment management, permanent existence, and total impartiality. While they charge a percentage of the assets as a fee (typically 0.5% to 1.5% annually), their expertise in tax planning and asset protection often pays for itself by preventing costly mistakes and maximizing market returns.

The Role of Successor Trustees

Wealth management is a long game. Many trusts are designed to last for generations. Therefore, a trustee must ensure there is a clear succession plan. A successor trustee is the “understudy” who takes over if the primary trustee can no longer serve. A responsible trustee helps prepare the successor by maintaining organized digital and physical files, ensuring a seamless transition of power that doesn’t trigger financial loss or legal hurdles for the beneficiaries.

Professional Fees and Compensation

Being a trustee is a job, and in the world of finance, work is compensated. Most states have laws allowing trustees to collect “reasonable compensation.” For individual trustees, this might be a small annual stipend or an hourly rate. For professionals, it is usually a tiered fee based on the total value of the assets under management. Understanding these costs is vital for beneficiaries, as these fees are paid directly out of the trust’s assets. A trustee must ensure that their fees—and the fees of any advisors they hire—are transparent and justified by the value they provide to the trust.

Conclusion: The Trustee as the Guardian of Financial Legacies

What do trustees do? They serve as the legal and financial guardians of a person’s life work. By blending the roles of an investment manager, an accountant, a legal compliance officer, and a family mediator, they ensure that wealth is not just earned, but preserved and purposefully distributed.

In the realm of personal finance, the trustee is the ultimate safeguard against the erosion of assets through taxes, poor market timing, or impulsive spending. Their role is one of immense responsibility and significant influence. For the grantor, a good trustee provides peace of mind that their wishes will be honored. For the beneficiary, the trustee provides the financial security and support intended by their loved ones. Ultimately, the work of a trustee is about more than just numbers on a balance sheet; it is about the disciplined management of capital to provide for the future, ensuring that a financial legacy survives and thrives across generations.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.