Credit Default Swaps (CDS) are a complex financial instrument that has played a significant role in global financial markets, often sparking both intrigue and controversy. At their core, they function as a form of insurance against the risk of a borrower defaulting on their debt obligations. While the concept may sound straightforward, the mechanics, implications, and historical context of CDS are multifaceted and warrant a detailed examination. Understanding CDS is crucial for anyone seeking a deeper insight into modern finance, corporate debt markets, and the interconnectedness of financial institutions.

The Anatomy of a Credit Default Swap

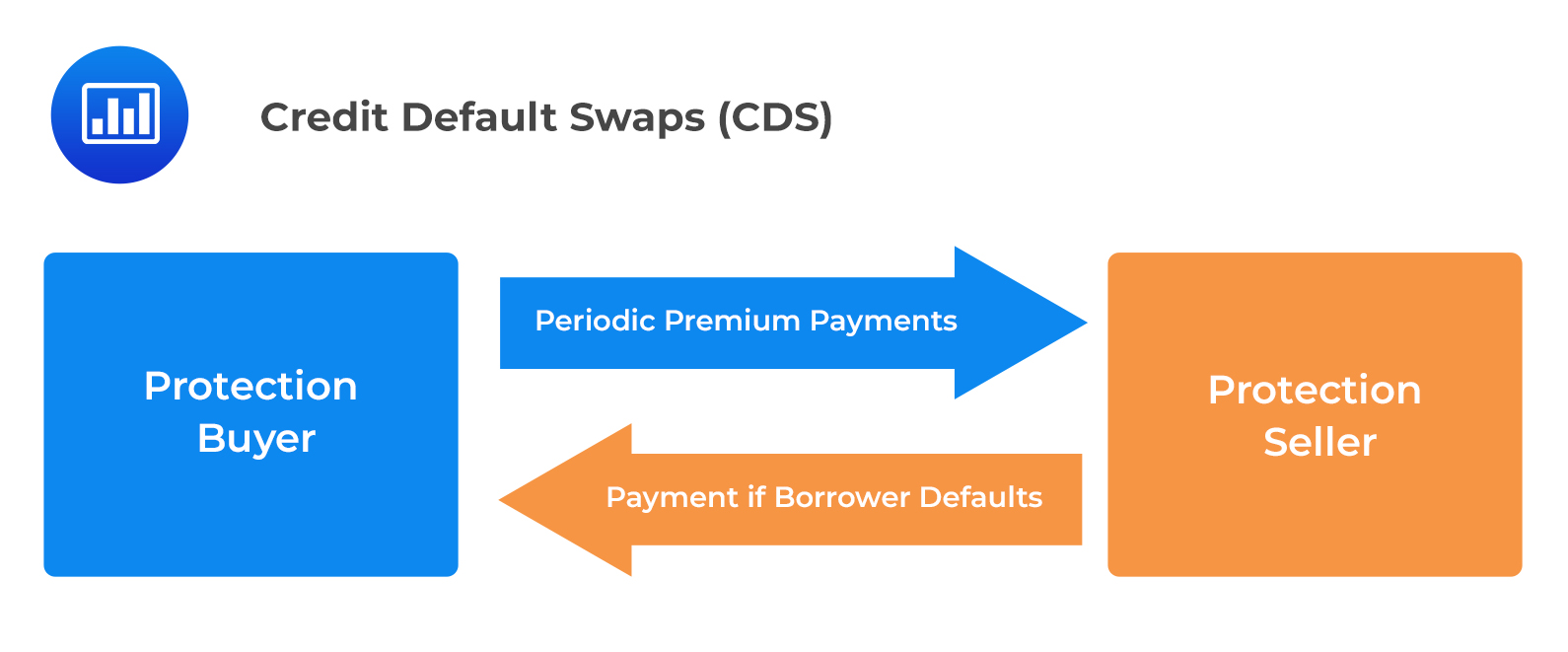

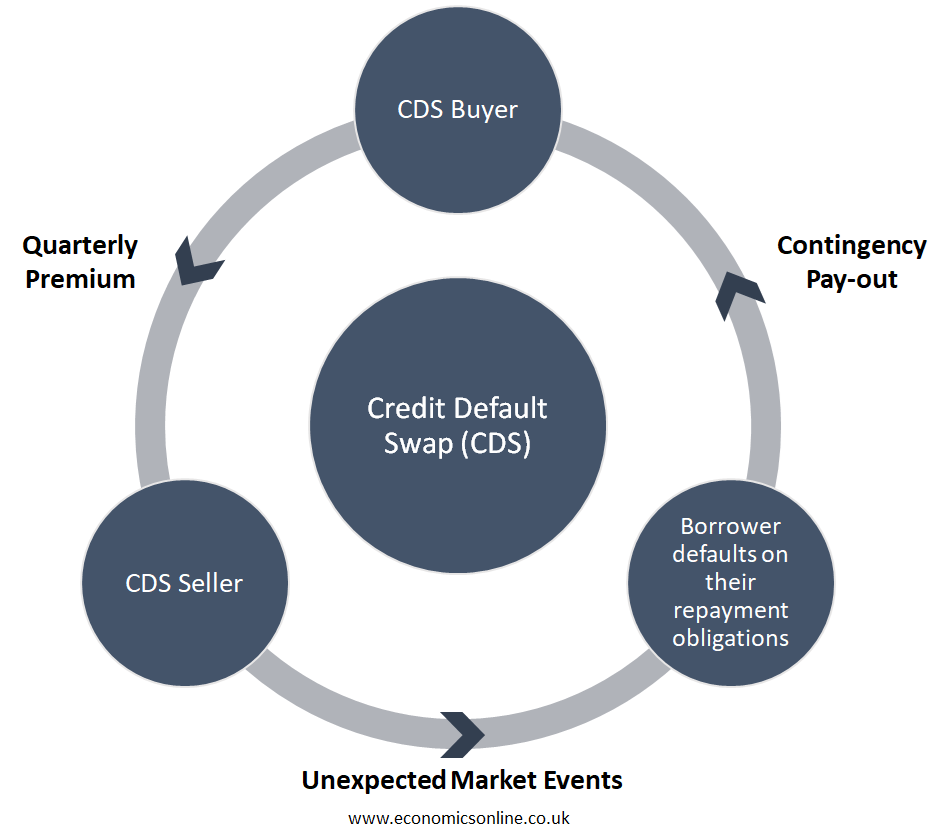

A Credit Default Swap is a bilateral contract between two parties: a protection buyer and a protection seller. The protection buyer makes periodic payments, akin to insurance premiums, to the protection seller. In return, the protection seller agrees to compensate the protection buyer if a specified “credit event” occurs concerning a particular debt instrument, typically a bond or loan. This credit event usually signifies a default, bankruptcy, or failure to make timely payments by the issuer of the underlying debt.

Parties Involved and Their Motivations

The relationship between the protection buyer and protection seller is driven by distinct motivations, each seeking to manage or profit from credit risk.

The Protection Buyer: Hedging and Speculation

The primary motivation for a protection buyer is to hedge against the risk of default. For instance, an investor holding a portfolio of corporate bonds might purchase CDS to protect against the possibility of one or more of those bond issuers defaulting. By paying the CDS premium, the bondholder transfers the credit risk to the protection seller. This allows them to maintain exposure to the potential upside of the bond while mitigating the downside risk of a credit event.

Beyond hedging, CDS can also be used for speculative purposes. An investor who believes a particular company or sovereign entity is likely to default can buy CDS protection without actually owning the underlying debt. This is known as “naked” CDS. If a default occurs, the protection buyer profits from the payout received from the protection seller, which is typically linked to the face value of the defaulted debt. This speculative aspect has been a source of considerable debate, as it can potentially amplify market volatility and create incentives for individuals to profit from financial distress.

The Protection Seller: Premium Income and Risk Appetite

The protection seller, conversely, takes on the credit risk in exchange for the premium payments. These sellers are typically financial institutions such as investment banks, insurance companies, or specialized hedge funds. Their decision to sell protection is usually based on their assessment of the creditworthiness of the underlying entity and their own risk appetite.

Protection sellers aim to generate income from the premiums collected. They are essentially betting that the credit event they are insuring against will not occur. If the underlying debt performs as expected and no default materializes, the protection seller keeps the premiums, which can be a lucrative source of revenue, especially if they have sold a large volume of CDS contracts. However, if a credit event does occur, the protection seller faces a potentially significant payout, which can lead to substantial losses.

Key Terms and Conditions

Several critical terms and conditions define a CDS contract:

Reference Entity and Reference Obligation

The reference entity is the entity whose creditworthiness is being insured against. This could be a corporation (e.g., General Electric) or a sovereign government (e.g., the Italian Republic). The reference obligation is the specific debt instrument (e.g., a particular bond issuance) issued by the reference entity that the CDS contract is linked to. The contract specifies which debt instruments are covered by the CDS.

Credit Events

A credit event is the trigger that obligates the protection seller to make a payment to the protection buyer. Common credit events include:

- Bankruptcy: The reference entity files for bankruptcy.

- Failure to Pay: The reference entity fails to make a scheduled interest or principal payment on its debt.

- Restructuring: The terms of the debt are significantly altered in a way that is detrimental to the creditors, often to avoid a default.

The precise definition of a credit event is crucial and can be subject to interpretation, which has led to disputes in the past.

Premium Payments and Payout

The premium payment, often referred to as the spread, is the regular fee paid by the protection buyer to the protection seller. It is usually expressed in basis points (hundredths of a percent) of the notional amount of the CDS contract. A higher spread generally indicates a higher perceived risk of default by the reference entity.

Upon the occurrence of a credit event, the protection seller must compensate the protection buyer. There are two primary settlement methods:

- Physical Settlement: The protection buyer delivers the defaulted reference obligation to the protection seller, who then pays the protection buyer the full face value of that obligation.

- Cash Settlement: The parties determine the market value of the defaulted debt. The protection seller pays the protection buyer the difference between the face value of the debt and its market value. This method is more common today.

The Role of Credit Default Swaps in Financial Markets

Credit Default Swaps emerged as a significant innovation in the financial world, offering new ways to manage and transfer credit risk. Their impact has been profound, influencing market liquidity, pricing of debt, and the stability of the financial system.

Enhancing Market Liquidity and Price Discovery

One of the primary benefits proponents attribute to CDS is their ability to enhance liquidity in the debt markets. By providing a mechanism to hedge credit risk, CDS can make investors more willing to buy and hold corporate bonds. This increased demand can lead to tighter credit spreads (the difference in yield between corporate bonds and risk-free government bonds), effectively lowering borrowing costs for companies.

Furthermore, the pricing of CDS can serve as a valuable indicator of market sentiment regarding the creditworthiness of an entity. A rising CDS spread suggests that the market perceives an increased risk of default, providing early warning signals to investors and regulators. This “price discovery” function can lead to more efficient allocation of capital.

Transferring and Concentrating Credit Risk

CDS facilitate the transfer of credit risk from those who originate it (e.g., banks that make loans) or hold it (e.g., bond investors) to those willing to assume it. This transfer can be beneficial, allowing for a more efficient distribution of risk across the financial system. For instance, banks can use CDS to reduce their exposure to specific borrowers, freeing up capital to lend to other businesses.

However, this risk transfer mechanism can also lead to the concentration of risk. If a few large financial institutions become significant protection sellers, and a widespread credit event occurs, these institutions could face massive losses, potentially destabilizing the entire financial system. This was a concern highlighted during the 2008 global financial crisis.

The Dark Side: Systemic Risk and Speculation

The role of CDS in the 2008 financial crisis brought their potential downsides into sharp focus. The collapse of the housing market led to widespread defaults on mortgage-backed securities, many of which were insured by CDS. Institutions that had sold vast amounts of CDS protection, such as American International Group (AIG), found themselves facing billions of dollars in payouts they could not afford. The interconnectedness of these contracts meant that the failure of one institution could cascade through the system, threatening the stability of others.

The speculative use of “naked” CDS also contributed to the crisis. Investors who did not own the underlying debt could bet on its default, potentially exacerbating market downturns. Critics argued that this allowed for excessive risk-taking and created an incentive for some to profit from economic distress. The sheer volume of CDS traded, often over-the-counter (OTC) without central clearing, meant that the extent of exposure was opaque, making it difficult to assess the true systemic risk.

Regulation and Evolution of Credit Default Swaps

The events of 2008 prompted significant regulatory reforms aimed at mitigating the risks associated with CDS. The goal was to increase transparency, reduce counterparty risk, and prevent future systemic crises.

Post-Crisis Regulatory Reforms

Following the financial crisis, regulators worldwide implemented measures to bring more oversight to the CDS market. Key reforms included:

Central Clearing and Exchange Trading

A significant shift has been towards mandating that many standardized CDS contracts be cleared through central clearinghouses. Central clearinghouses act as intermediaries, stepping in between buyers and sellers to guarantee trades. This reduces counterparty risk, the risk that one party to a contract will default. By novating trades, the clearinghouse becomes the buyer to every seller and the seller to every buyer, ensuring that even if one party fails, the trade is still completed.

Furthermore, efforts have been made to move CDS trading onto regulated exchanges or electronic trading platforms, rather than solely relying on bilateral, over-the-counter negotiations. This increased transparency in pricing and trading activity allows for better monitoring by regulators and market participants.

Capital Requirements and Reporting

Regulators also strengthened capital requirements for financial institutions that deal in CDS. This means that banks and other entities selling protection must hold more capital reserves to absorb potential losses. Enhanced reporting requirements have also been introduced, providing regulators with better data on the volume, participants, and exposures within the CDS market.

Ongoing Debates and Future of CDS

Despite regulatory efforts, debates surrounding CDS continue. Some argue that further restrictions are needed, particularly on speculative naked CDS, while others contend that the market, with its new regulatory framework, now plays a valuable role in risk management.

The future of CDS will likely involve continued adaptation to regulatory environments and evolving market needs. While the instruments themselves are complex, their underlying purpose of managing and transferring credit risk remains a fundamental aspect of modern finance. Understanding their mechanics and implications is essential for navigating the intricate landscape of global financial markets and appreciating the ongoing efforts to balance innovation with financial stability.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.