The year 1929 marks one of the most cataclysmic events in financial history: the Wall Street Crash, often regarded as the precipitating factor of the Great Depression. For investors, economists, and policymakers alike, understanding its causes remains a crucial, if sobering, exercise in financial literacy and risk management. Far from being a singular event, the 1929 crash was the culmination of a complex interplay of speculative fervor, structural economic weaknesses, policy missteps, and a fundamental breakdown of confidence. Delving into this historical moment offers invaluable insights into market dynamics, the perils of unchecked optimism, and the vital role of regulation in safeguarding financial stability.

The Roaring Twenties: An Era of Unchecked Optimism and Speculation

The decade leading up to the crash, known as the Roaring Twenties, was characterized by unprecedented economic growth, technological innovation, and a prevailing sense of optimism. Emerging from the shadow of World War I, the United States economy boomed, fueled by new industries and a burgeoning consumer culture. This era, however, also sowed the seeds of its own downfall through excessive speculation and a widespread disregard for fundamental economic principles.

The Allure of Easy Money and the Stock Market Boom

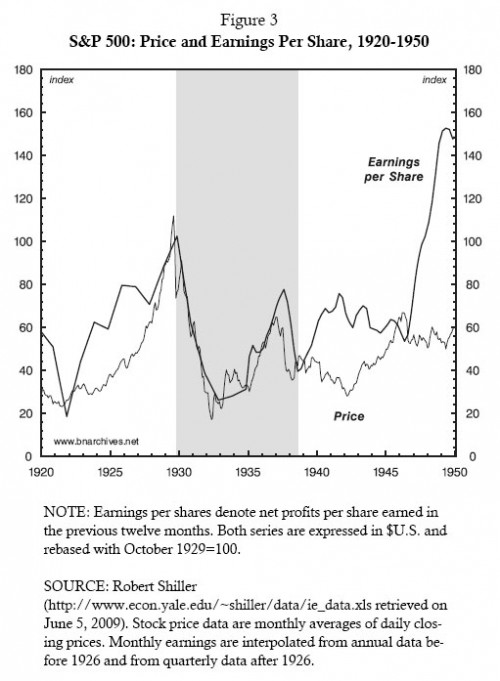

Following the end of World War I, America experienced a period of rapid industrial expansion. New technologies like the automobile, radio, and household appliances created entirely new industries, driving production and employment. Corporate profits soared, and the stock market became an increasingly attractive avenue for wealth creation. Ordinary citizens, alongside seasoned investors, were drawn into the market by stories of quick riches. The prevailing sentiment was that stocks could only go up, leading many to believe that the market offered a guaranteed path to prosperity. This bullish enthusiasm was often detached from the underlying value of the companies themselves, transforming the stock market into a speculative playground rather than a mechanism for capital allocation based on intrinsic worth. Banks, too, participated eagerly, lending generously to brokers who then extended credit to individual investors, creating a vast network of leveraged speculation.

Margin Buying and Speculative Bubbles

One of the most significant accelerants of the stock market boom was the widespread practice of buying on margin. This allowed investors to purchase stocks by putting down only a small percentage of the stock’s value (as little as 10% in some cases) and borrowing the rest from their broker. While margin buying amplified potential gains during an uptrend, it also exponentially increased risk. If stock prices fell, investors would receive a margin call, requiring them to deposit more money or sell their shares. The promise of outsized returns overshadowed the inherent dangers, drawing a growing number of individuals into the market, many of whom lacked a sophisticated understanding of financial risk. As more money, much of it borrowed, flowed into stocks, prices were artificially inflated, creating a classic speculative bubble that was detached from genuine economic output or corporate earnings.

The Federal Reserve’s Role (or Lack Thereof)

The Federal Reserve, established in 1913, was still a relatively young institution navigating its role in managing the nation’s monetary policy. During the speculative boom of the 1920s, the Fed’s actions were often inconsistent and, in hindsight, insufficient to curb the escalating speculation. While some officials recognized the dangers of the overheated market, the consensus was divided. Early attempts to tighten credit through interest rate hikes were timid and largely ineffective against the powerful speculative forces at play. Furthermore, the Fed was reluctant to directly intervene in the stock market, fearing that doing so would be seen as an overreach and potentially damage the broader economy. This hesitancy allowed the speculative bubble to grow unchecked for an extended period, ultimately contributing to the severity of the eventual collapse. Once the crash occurred, the Fed’s subsequent tightening of monetary policy in 1930 and 1931, arguably aimed at preserving the gold standard and limiting further bank failures, paradoxically worsened the contraction by constricting credit availability when it was most desperately needed.

Underlying Economic Fragilities and Structural Weaknesses

While the speculative frenzy in the stock market was the most visible sign of impending trouble, the American economy of the late 1920s harbored deep-seated structural weaknesses that made it particularly vulnerable to a shock. These underlying fragilities ensured that a market correction would not merely be a temporary setback but would cascade into a prolonged economic depression.

Agricultural Distress and Overproduction

Long before the urban centers experienced the market euphoria, the agricultural sector had been mired in a severe recession since the early 1920s. During World War I, American farmers expanded production to feed Europe. However, with the war’s end, European agriculture recovered, and demand for American produce plummeted. Farmers were left with vast surpluses, leading to a drastic fall in commodity prices. Despite technological advancements like tractors that increased efficiency, overproduction persisted, trapping many farmers in a cycle of debt and poverty. This widespread agricultural distress significantly reduced the purchasing power of a substantial segment of the American population, leading to a decrease in demand for manufactured goods and creating a fundamental imbalance in the economy. This sector’s struggles were a critical, yet often overlooked, contributing factor to the overall economic instability.

Unequal Distribution of Wealth

The prosperity of the Roaring Twenties was far from evenly distributed. While corporate profits and stock market gains soared, wages for many workers lagged, leading to a widening gap between the rich and the poor. A significant portion of the nation’s wealth and income was concentrated in the hands of a small percentage of the population. This unequal distribution had critical implications for the broader economy. With a large segment of the population having limited disposable income, aggregate consumer demand was insufficient to keep pace with the massive industrial output. Factories, geared for mass production, eventually faced flagging sales as average Americans could not afford to buy all the goods being produced. This created an inventory glut, leading to production cutbacks, layoffs, and further weakening of consumer spending, forming a vicious cycle that predated the stock market crash.

International Economic Instability and Tariffs

The global economic landscape post-World War I was fraught with instability. The war left European nations burdened with immense debts to the United States and entangled in a complex web of reparations payments from Germany. The flow of capital was often unsustainable, with American loans propping up European economies that struggled to recover. Adding to this fragility, the United States adopted increasingly protectionist trade policies, most notably the Smoot-Hawley Tariff Act of 1930. While enacted after the initial crash, the underlying sentiment of protectionism was already prevalent. These high tariffs were intended to protect American industries but instead provoked retaliatory tariffs from other countries, stifling international trade and exacerbating the global economic downturn. The collapse of international trade further dampened demand for American goods and contributed to a worldwide economic contraction, demonstrating the interconnectedness of global financial systems.

The Trigger and the Tipping Point: Black Thursday and Black Tuesday

The latent fragilities and speculative excesses reached their breaking point in October 1929. The weeks leading up to the definitive crash were marked by growing anxiety, subtle market corrections, and a gradual erosion of investor confidence. However, it was the rapid-fire events of Black Thursday and Black Tuesday that unleashed full-blown panic and shattered the illusion of endless prosperity.

Warning Signs and Investor Anxiety

Throughout 1929, subtle tremors began to shake the market. Interest rates had been rising, making margin borrowing more expensive. Production figures in some key industries began to slow, and reports of declining corporate earnings started to surface. Some astute investors and financial analysts, like Roger Babson, issued warnings about an impending crash, comparing the speculative fever to a financial house of cards. Yet, these voices were largely drowned out by the continued optimism and the prevailing “buy the dip” mentality. By late September and early October, the market started to experience more noticeable downward movements, particularly in utility and railroad stocks. These initial corrections, while concerning, were often dismissed as healthy adjustments, but they nonetheless stoked underlying investor anxiety.

The Panic Unleashed: October 24th and 29th

The fateful day of Thursday, October 24th, 1929, known as Black Thursday, saw an unprecedented volume of selling. The market opened with a sharp drop, and panic quickly set in as investors, many holding shares bought on margin, rushed to liquidate their holdings to cover margin calls or simply to stem their losses. The ticker tape ran hours behind, creating further chaos as investors were unaware of the current prices of their stocks. Leading bankers attempted to stem the tide by pooling funds and publicly buying large blocks of blue-chip stocks at inflated prices to restore confidence. While this effort temporarily stabilized the market on Friday, it proved to be a fleeting reprieve.

The true capitulation came on Tuesday, October 29th, 1929, Black Tuesday. This day witnessed the most devastating single-day decline in market history up to that point. Over 16 million shares were traded—a record that would stand for decades—as a frenzy of selling swept through Wall Street. There were virtually no buyers, and stock prices plummeted across the board, wiping out billions of dollars in wealth in a single session. The efforts of the bankers from Black Thursday were overwhelmed by the sheer scale of the panic. The market had officially crashed, signifying not just a correction, but a complete collapse of investor trust and speculative exuberance.

The Contagion Effect and Bank Runs

The immediate aftermath of the stock market crash was characterized by a severe contraction of credit and a wave of financial contagion. Many investors, having borrowed heavily to buy stocks, were ruined. Banks that had lent money to investors or brokers, or had invested their own funds in the stock market, faced massive losses. As the economic situation deteriorated, people began to lose faith in the banking system. Fears of bank insolvency led to widespread bank runs, where depositors rushed to withdraw their money. Without deposit insurance (which would come later), many banks lacked the reserves to meet these demands and were forced to close, wiping out the savings of millions of ordinary Americans. The collapse of the banking system starved businesses of crucial credit, leading to further bankruptcies, factory closures, and mass unemployment, pushing the economy deeper into what would become the Great Depression.

Lessons from the Abyss: Preventing Future Catastrophes

The 1929 crash and the subsequent Great Depression served as a stark, albeit painful, lesson for governments, financial institutions, and investors worldwide. The failures exposed during this period directly led to significant reforms aimed at preventing a recurrence of such a catastrophic economic collapse.

Regulatory Reforms and Investor Protection

One of the most profound outcomes of the crash was a fundamental rethinking of market regulation. Prior to 1929, the securities markets were largely unregulated, operating with little transparency and oversight. In response, the U.S. government enacted landmark legislation, including the Securities Act of 1933 and the Securities Exchange Act of 1934. These acts established the Securities and Exchange Commission (SEC), an independent agency tasked with regulating the securities industry, protecting investors, and maintaining fair and orderly markets. Key reforms included mandatory disclosure of financial information by public companies, prohibition of insider trading, and strict rules regarding margin requirements. The creation of the Federal Deposit Insurance Corporation (FDIC) in 1933 also stabilized the banking system by insuring depositors’ money, thereby preventing the panic-driven bank runs that plagued the early 1930s.

Monetary Policy Evolution and Central Bank Responsibilities

The Federal Reserve’s response to the 1929 crash and the subsequent depression was widely criticized, particularly its tightening of monetary policy in the early 1930s. This experience profoundly reshaped the understanding of central bank responsibilities. Modern central banks are now expected to act as a “lender of last resort” during financial crises, providing liquidity to prevent the collapse of the banking system. The Fed’s dual mandate, encompassing both maximum employment and price stability, also reflects a broader understanding of its role in macroeconomic management. Economic theory, particularly influenced by the work of John Maynard Keynes, emphasized the importance of counter-cyclical fiscal and monetary policies to stabilize the economy during downturns, moving away from the more laissez-faire approaches that characterized the pre-Depression era.

The Enduring Relevance for Modern Investors

Even today, nearly a century later, the lessons of the 1929 crash remain profoundly relevant for modern investors. The dangers of speculative bubbles, fueled by irrational exuberance and excessive leverage, are a recurring theme in financial history. Investors are constantly reminded of the importance of conducting thorough due diligence, understanding the fundamentals of their investments, and avoiding “herd mentality.” Diversification across different asset classes and geographies remains a critical strategy to mitigate risk. Furthermore, the role of emotion—greed during a boom and fear during a bust—is a powerful force in market movements, often leading to irrational decisions. A disciplined, long-term approach, coupled with a healthy skepticism towards get-rich-quick schemes, serves as a timeless defense against the kind of systemic risks that precipitated the 1929 collapse. The understanding that markets can, and do, correct sharply reminds all participants of the imperative for prudence and risk management in their financial decisions.

The 1929 crash was a multifaceted disaster, born from a complex interplay of speculative excess, deep-seated economic imbalances, and a series of policy missteps. It was not merely a stock market correction but a profound economic wound that took years to heal and reshaped the role of government in economic management. Its legacy continues to inform financial regulation, monetary policy, and investor behavior, serving as a powerful reminder of the fragility of financial systems when unchecked optimism and fundamental weaknesses converge.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.