For many homeowners, the greatest source of wealth isn’t sitting in a savings account or a 401(k); it is built into the four walls of their primary residence. As property values rise, so does your home equity—the difference between what your home is worth and what you owe on your mortgage. One of the most flexible ways to access this wealth is through a Home Equity Line of Credit, or HELOC.

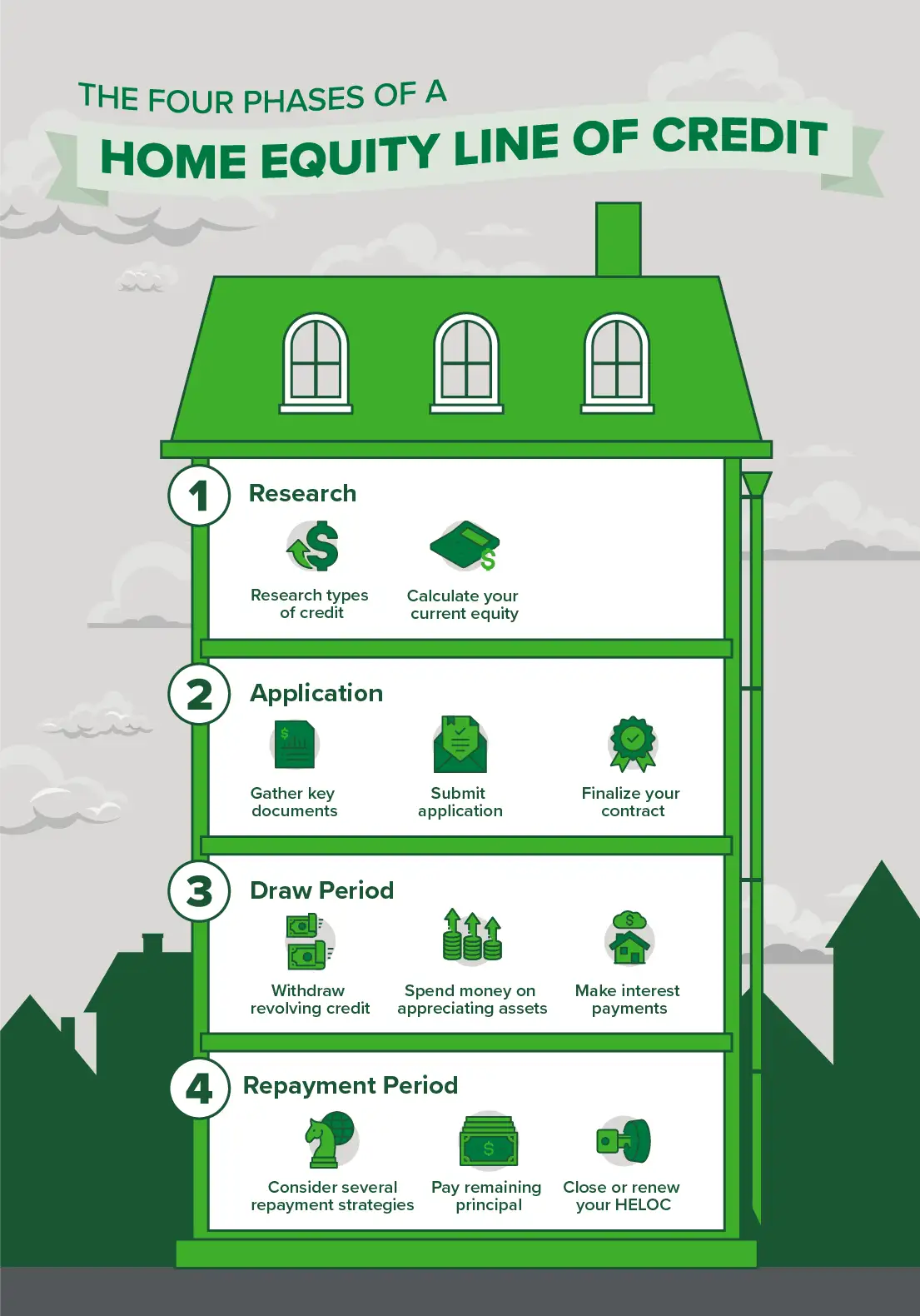

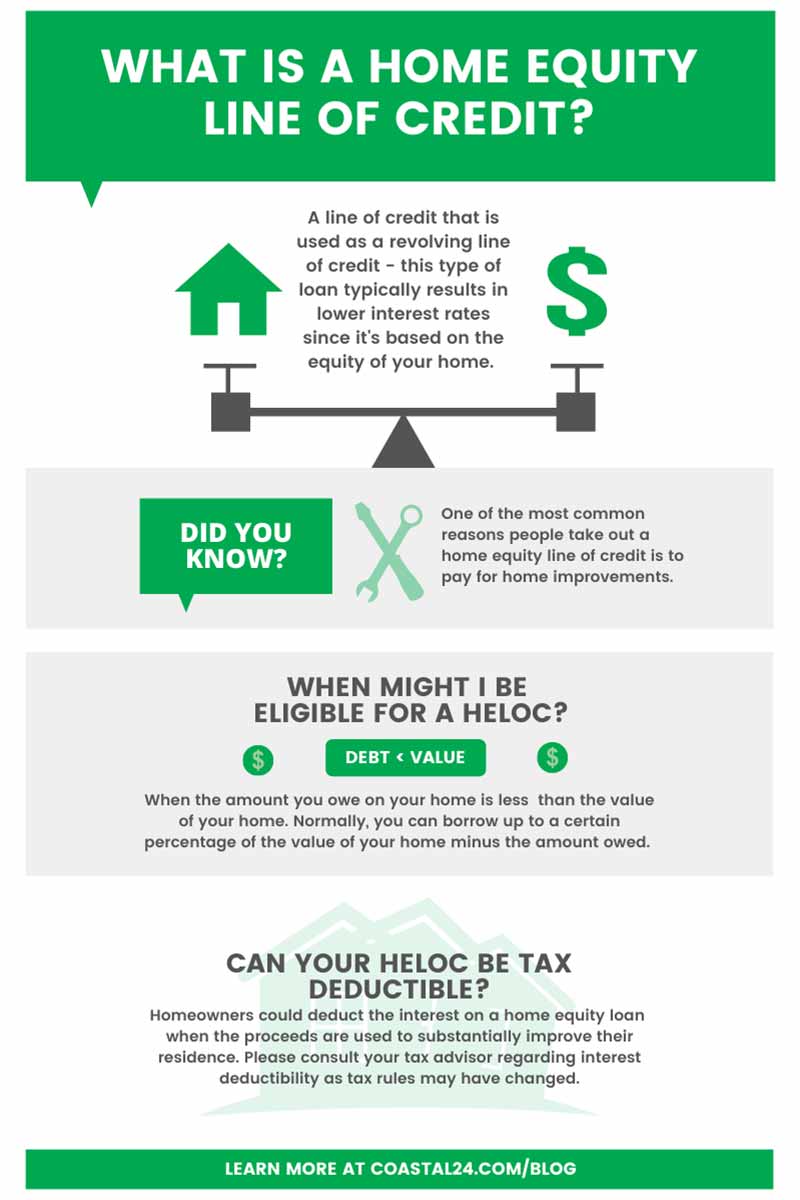

A HELOC functions much like a credit card but is secured by your home. It provides a revolving line of credit that you can draw from as needed, pay back, and draw from again during a specific “draw period.” Because it is a secured loan, the interest rates are typically much lower than those of unsecured personal loans or credit cards. However, with great flexibility comes significant responsibility. Understanding the most effective and financially sound ways to utilize a HELOC is essential for any homeowner looking to improve their financial position.

1. High-ROI Home Improvements and Renovations

The most traditional and often the smartest use of a HELOC is reinvesting that money back into the asset that secured it. When you use a HELOC to improve your home, you aren’t just spending money; you are potentially increasing the market value of your property.

Increasing Property Value

Not all home improvements are created equal. Using a HELOC for a luxury swimming pool might provide personal enjoyment, but it rarely offers a 1:1 return on investment (ROI). On the other hand, strategic renovations like kitchen remodels, bathroom updates, or adding usable square footage (such as a finished basement or an Accessory Dwelling Unit) can significantly boost your home’s resale value. By using a HELOC for these projects, you are essentially using your equity to create more equity.

Tax Advantages of Home Improvements

Under current IRS regulations, the interest paid on a HELOC may be tax-deductible if the funds are used specifically to “buy, build, or substantially improve” the home that secures the loan. This makes a HELOC one of the most tax-efficient ways to finance a renovation compared to a personal loan or a high-interest credit card, where interest is never deductible.

Maintaining Asset Integrity

Sometimes, the best use of a HELOC isn’t for a “want” but for a “need.” Major maintenance issues—such as a failing roof, a dated HVAC system, or structural repairs—can lead to a rapid decline in property value if left unaddressed. A HELOC provides a ready source of capital to tackle these expensive but necessary repairs before they become catastrophic financial burdens.

2. Strategic Debt Consolidation

In an era of rising interest rates, carrying high-interest consumer debt can be a significant barrier to wealth accumulation. A HELOC can serve as a powerful tool for debt restructuring, allowing you to fold high-interest liabilities into a single, lower-interest monthly payment.

Eliminating High-Interest Credit Card Debt

The average interest rate on credit cards often hovers between 18% and 25%. In contrast, HELOC rates, while variable, are typically in the single digits or low double digits. By drawing on a HELOC to pay off high-interest credit cards, you can save thousands of dollars in interest charges and shorten the timeline to becoming debt-free. This process effectively converts “bad debt” (high-interest, non-deductible) into “structured debt” (lower-interest, potentially more manageable).

Consolidating Personal and Student Loans

Beyond credit cards, many individuals carry personal loans or private student loans with unfavorable terms. A HELOC allows you to streamline your finances by consolidating these various payments into one. This not only simplifies your monthly budgeting but also improves your cash flow, as the lower interest rate reduces the total monthly outflow of capital.

The Psychology of Debt Management

While consolidation is a brilliant mathematical move, it requires discipline. The danger of using a HELOC for debt consolidation is “reloading”—the habit of clearing credit card balances only to run them up again. To use a HELOC successfully for this purpose, a homeowner must pair the financial move with a strict budget to ensure they don’t increase their total debt load.

3. Investing in Future Growth and Education

A HELOC isn’t just for fixing what you have; it can be a launchpad for future financial growth. Because it offers a large lump sum of capital with flexible repayment terms, it can be used to fund endeavors that have the potential to yield a higher return than the interest rate of the loan.

Financing Higher Education

While federal student loans often offer protections like income-driven repayment, they may not cover the full cost of attendance, or the interest rates for private student loans might be prohibitively high. Using a HELOC to fund a child’s college education or a professional degree for yourself can be a savvy move. Education is an investment in human capital that generally leads to higher lifetime earnings, making it a justifiable use of home equity.

Capital for Small Business and Side Hustles

Many successful entrepreneurs used their homes to bootstrap their businesses. If you have a solid business plan and need capital for inventory, equipment, or marketing, a HELOC can provide a lower-cost alternative to a business gestation loan or a high-interest SBA loan. Using equity to start a revenue-generating business can diversify your income streams and build long-term wealth.

Real Estate Investment Opportunities

Seasoned investors often use a HELOC on their primary residence to provide the down payment for an investment property. This “equity stripping” allows you to expand your real estate portfolio without needing to save for years to gather a 20% down payment. If the rental income from the new property covers both its own mortgage and the HELOC interest, you have effectively used your home to acquire a new cash-flowing asset.

4. Emergency Reserves and Life Milestones

Financial advisors often recommend having three to six months of expenses in a liquid savings account. However, in the event of a major life upheaval, a HELOC can act as a secondary emergency fund or a way to manage the costs of significant life milestones.

An Alternative Emergency Fund

While you should never rely solely on credit for emergencies, a HELOC provides a “safety net for the safety net.” If a homeowner faces a sudden job loss or a medical crisis that exceeds their cash savings, the draw period of a HELOC offers immediate access to funds. This can prevent the need to liquidate retirement accounts or stocks during a market downturn, which would otherwise result in taxes and lost growth potential.

Funding Major Life Events

Life is full of expensive milestones—weddings, milestone anniversaries, or the adoption of a child. While it is always preferable to save for these events in advance, a HELOC can bridge the gap. Because you only pay interest on what you actually draw, you can use the line of credit to manage the timing of expenses, paying it down as your cash flow allows.

Bridging the Gap in Retirement

For older homeowners, a HELOC can be a strategic tool during the early years of retirement. If the stock market is in a temporary decline, a retiree might choose to draw from a HELOC for living expenses rather than selling off shares of their portfolio at a loss. This allows the portfolio time to recover, preserving the long-term longevity of their retirement savings.

5. Critical Risks and Financial Discipline

While the uses for a HELOC are vast, it is not “free money.” It is a sophisticated financial instrument that requires a high level of fiscal responsibility. Before tapping into your equity, you must understand the inherent risks involved in the Money niche.

The Risk of Collateral

The most important factor to remember is that your home is the collateral. If you are unable to make the payments on a HELOC, the lender has the legal right to initiate foreclosure. Unlike a credit card, which is unsecured, a HELOC puts your primary shelter at risk. Therefore, it should never be used for frivolous spending or depreciating assets like luxury cars or expensive vacations.

Variable Interest Rates and Payment Shocks

Most HELOCs come with variable interest rates tied to the Prime Rate. This means that if the Federal Reserve raises interest rates, your monthly payment will increase. Furthermore, HELOCs eventually transition from a “draw period” (where you might only pay interest) to a “repayment period” (where you must pay both principal and interest). Homeowners must be prepared for the “payment shock” that occurs when the repayment phase begins.

Maintaining a Healthy Loan-to-Value (LTV) Ratio

Over-leveraging your home can be dangerous if property values in your area drop. If you draw 90% of your home’s value and the market dips by 15%, you could find yourself “underwater,” owing more than the home is worth. This limits your ability to sell or refinance. A conservative approach—using only what is necessary and leaving a cushion of equity—is the hallmark of a wise financial strategy.

Conclusion

A Home Equity Line of Credit is one of the most versatile tools in the personal finance toolkit. Whether you are using it to increase your property value through renovations, consolidate high-interest debt, or invest in a new business venture, a HELOC allows you to put your dormant equity to work.

However, its greatest strength—flexibility—is also its greatest risk. The key to successfully using a HELOC is to ensure that the purpose of the loan either increases your net worth, saves you more money in interest than it costs, or provides a necessary safety net during a crisis. By treating your home equity with the respect it deserves and maintaining a disciplined repayment plan, you can transform your home into a powerful engine for long-term financial stability and growth.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.