In the modern economic landscape, your credit score is more than just a three-digit number; it is a vital indicator of your financial reliability and a primary gatekeeper to your future purchasing power. Whether you are looking to secure a mortgage for a first home, lease a vehicle, or even apply for a premium credit card with travel rewards, your credit score sits at the center of the decision-making process.

A high credit score translates to lower interest rates, which can save you tens of thousands of dollars over the life of a loan. Conversely, a poor score can lead to rejections or predatory lending terms that stall your financial progress. Improving your credit score is not an overnight task, but rather a strategic journey that requires an understanding of credit mechanics, disciplined habits, and the right financial tools. This guide provides a deep dive into the actionable steps you can take to elevate your score and secure your financial future.

Understanding the Mechanics of the Credit Score System

Before you can effectively improve your credit score, you must understand the architecture of the system that evaluates you. Most lenders rely on the FICO score or the VantageScore, both of which weigh different aspects of your financial behavior to determine your risk level.

The Components of a FICO Score

The Fair Isaac Corporation (FICO) score is the industry standard used by the vast majority of lenders. It is calculated using five distinct categories of data. Payment history is the most significant factor, accounting for 35% of your score. This is followed by credit utilization (30%), length of credit history (15%), credit mix (10%), and new credit inquiries (10%). Understanding these weights is crucial because it allows you to prioritize your efforts. For instance, focusing on paying down a balance yields a higher return on your score than opening a new type of account.

Why Credit Scoring Models Vary

It is common for consumers to notice slight discrepancies between the scores they see on different platforms. This happens because there are multiple versions of FICO and VantageScore, and lenders may pull data from any of the three major credit bureaus: Equifax, Experian, and TransUnion. Some bureaus might have information that others do not, such as a recent collection account or a specific inquiry. To maintain a high score across the board, you must ensure that your positive financial behavior is consistent and that you are monitoring all three reports regularly.

Immediate Tactical Steps to Boost Your Score

If you need to see a movement in your score within a few months, you must focus on the “big two” categories: payment history and credit utilization. These represent 65% of your total score and are the areas where you have the most direct control.

Payment History: The Gold Standard

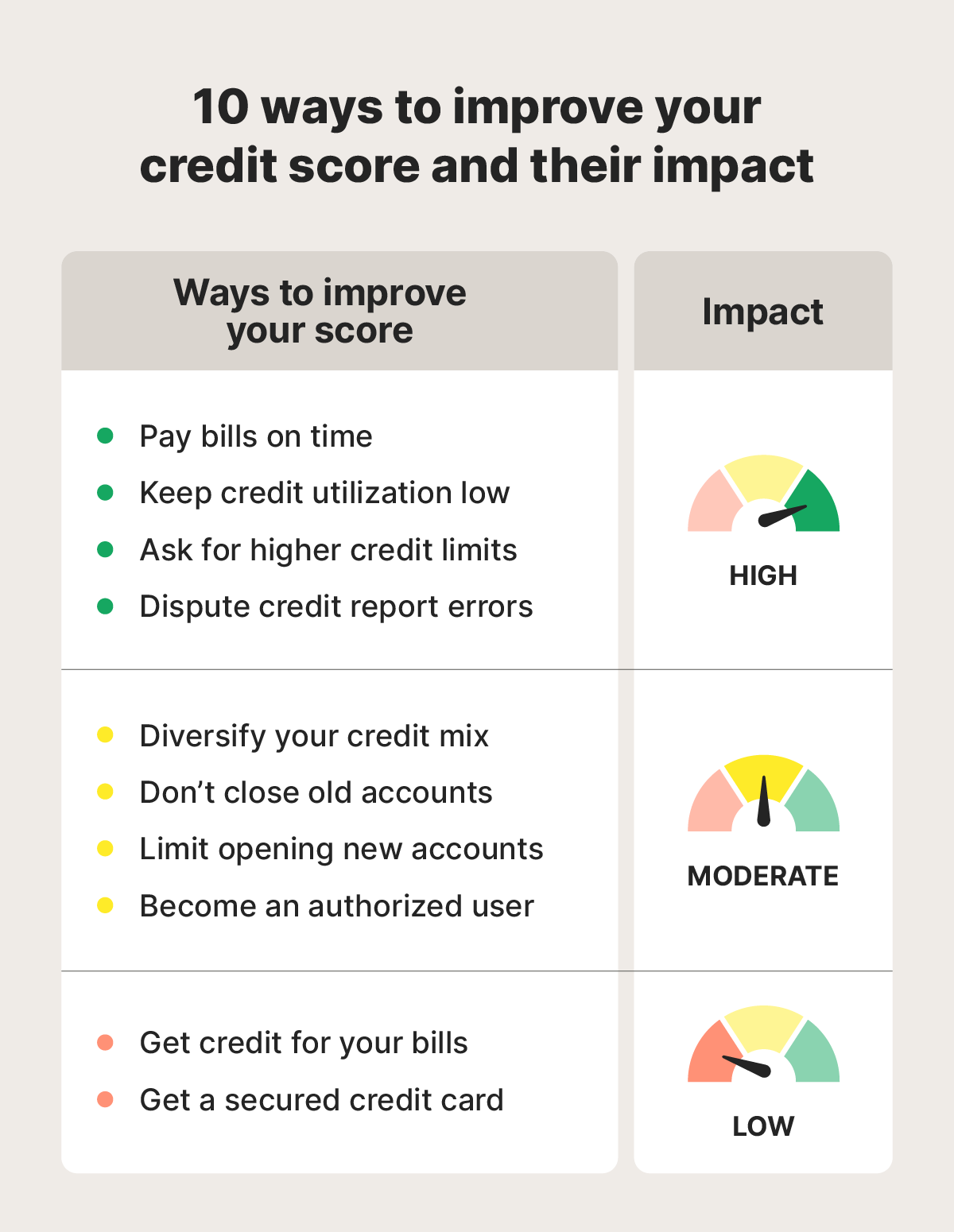

Nothing damages a credit score faster than a missed or late payment. Even a single 30-day delinquency can cause a score to plummet by 50 to 100 points, depending on your starting position. To improve your score, you must ensure that every current account is paid on time.

If you have missed payments in the past, the best course of action is to get current and stay current. While the “late” mark remains on your report for seven years, its impact diminishes over time as you replace it with a string of positive, on-time payments. Consider setting up automatic payments for at least the minimum amount due on every account to safeguard against forgetfulness.

Strategic Debt Management and Credit Utilization

Credit utilization refers to the amount of revolving credit you are currently using compared to your total available limit. Financial experts generally recommend keeping this ratio below 30%, though those with the highest scores often keep it under 10%.

To improve this ratio quickly, you can use two strategies. First, make extra payments throughout the month to lower your balance before the statement closing date—the date the bank reports your balance to the bureaus. Second, you can request a credit limit increase on your existing cards. If your limit increases while your spending stays the same, your utilization ratio drops instantly. However, only pursue this if you have the discipline not to see the higher limit as an excuse for more spending.

Long-Term Strategies for Sustained Growth

While tactical fixes can provide a quick bump, long-term financial health is built on the foundation of credit age and diversity. These factors demonstrate to lenders that you can manage different types of debt over a significant period.

The Importance of Credit Age and Mix

The length of your credit history accounts for 15% of your score. This includes the age of your oldest account, the age of your newest account, and the average age of all your accounts. For this reason, it is almost always a mistake to close old credit card accounts, even if you no longer use them. Keeping them open adds to your average age and increases your total available credit, which helps your utilization ratio.

Furthermore, lenders like to see a “credit mix.” This means having a combination of revolving credit (like credit cards) and installment loans (such as auto loans, student loans, or mortgages). If you only have credit cards, successfully managing a small personal loan can diversify your profile and potentially boost your score by demonstrating versatility in handling debt.

Limiting New Credit Inquiries

Every time you apply for credit, a “hard inquiry” is placed on your report, which can temporarily shave a few points off your score. While one inquiry is negligible, several inquiries in a short period can signal financial distress to lenders. To improve and protect your score, be selective about applying for new credit. If you are shopping for a specific loan, such as a mortgage or auto loan, try to do all your rate-shopping within a 14-to-45-day window; most modern scoring models will treat multiple inquiries for the same purpose within this timeframe as a single event.

Advanced Tools and Monitoring for Financial Health

In the digital age, several financial tools and legal protections are available to help consumers manage and repair their credit scores more efficiently than in the past.

Leveraging Credit Boosting Apps and Services

Innovative financial tools now allow you to get credit for bills that weren’t traditionally reported. Services like Experian Boost allow you to link your bank account to your credit report to include on-time payments for utilities, phone bills, and streaming services. For renters, services that report your monthly rent payments to the bureaus can be a powerful way to build credit without taking on new debt. These tools are particularly beneficial for “thin-file” consumers who have limited traditional credit history.

Identifying and Disputing Inaccuracies on Your Report

Statistics suggest that a significant percentage of credit reports contain errors, ranging from incorrect personal information to accounts that don’t belong to the consumer. Under the Fair Credit Reporting Act (FCRA), you have the right to dispute inaccurate information.

You should pull your free credit report from AnnualCreditReport.com and scrutinize it for any discrepancies. If you find a debt that isn’t yours or a late payment that you actually paid on time, file a formal dispute with the credit bureau. They are legally required to investigate and remove the item if it cannot be verified, which can lead to a substantial and immediate increase in your score.

Creating a Sustainable Financial Roadmap

Improving your credit score is not just about manipulating numbers; it is about fostering a healthy relationship with money. A high credit score is a byproduct of sound financial planning and disciplined execution.

Building Habits for Permanent Stability

The final step in improving your credit score is to automate your success. This involves creating a robust budget that ensures you never live beyond your means. By maintaining an emergency fund, you reduce the risk of having to rely on high-interest credit cards when unexpected expenses arise.

View your credit score as a financial asset that needs to be nurtured. Check your score monthly through your bank’s app or a free monitoring service. When you see the numbers rise, let it serve as motivation to continue your path toward financial freedom. With patience and persistence, you can transform your credit profile from a liability into one of your greatest financial strengths.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.