The New York City congestion pricing plan, officially known as the Central Business District (CBD) Tolling Program, represented one of the most significant fiscal interventions in the history of American urban planning. At its core, the plan was never just about traffic management; it was a massive financial engine designed to solve a multi-generational funding crisis within the Metropolitan Transportation Authority (MTA). By placing a price on the scarcity of road space in lower Manhattan, the state aimed to create a sustainable revenue stream that would serve as the collateral for billions of dollars in infrastructure bonds.

Understanding the New York congestion pricing plan requires a deep dive into the intersection of macroeconomics, public finance, and urban infrastructure investment. It was a bold experiment in “value capture”—the idea that the economic activity of a city should fund the very systems that make that activity possible.

The Economic Rationale Behind the Manhattan Central Business District Tolling Program

The financial logic of congestion pricing is rooted in the concept of Pigouvian taxes—charges levied against private individuals or businesses for engaging in activities that create adverse side effects for society. In this case, the “negative externality” was traffic congestion, which costs the New York metropolitan economy an estimated $20 billion annually in lost productivity, wasted fuel, and increased delivery costs.

Revenue Generation for the MTA’s Capital Program

The primary fiscal objective of the plan was to generate $1 billion in gross annual revenue. While $1 billion is a substantial sum, its true value lay in its ability to be “leveraged.” In the world of municipal finance, steady revenue streams are used to back the issuance of bonds. The MTA planned to use the $1 billion in annual toll revenue to secure approximately $15 billion in municipal bonds.

This $15 billion was earmarked for the MTA’s 2020–2024 Capital Program. These funds were not intended for daily operations—like paying bus drivers or cleaning stations—but for massive, long-term investments. This included the modernization of 100-year-old signaling systems, the expansion of the Second Avenue Subway, and the accessibility upgrades (elevators and ramps) required by the Americans with Disabilities Act (ADA). From a business finance perspective, congestion pricing was the cornerstone of the MTA’s balance sheet.

The Cost of Congestion: Productivity and Time Value

Beyond the direct revenue for the MTA, the plan was designed to improve the “velocity” of the city’s economy. For businesses that rely on the movement of goods—plumbers, food wholesalers, and couriers—time is literally money. When a delivery truck is stuck in gridlock for two hours, the “opportunity cost” is the additional three or four deliveries that could have been made in that same window.

By reducing the number of private vehicles in the zone by an estimated 17%, the plan aimed to increase traffic speeds. For the commercial sector, the $24 to $36 toll for trucks was viewed by some economists as a net positive; the cost of the toll would be offset by the financial gain of avoiding hours of idling and driver wages spent in stationary traffic.

Fiscal Impact on Commuters and the Local Economy

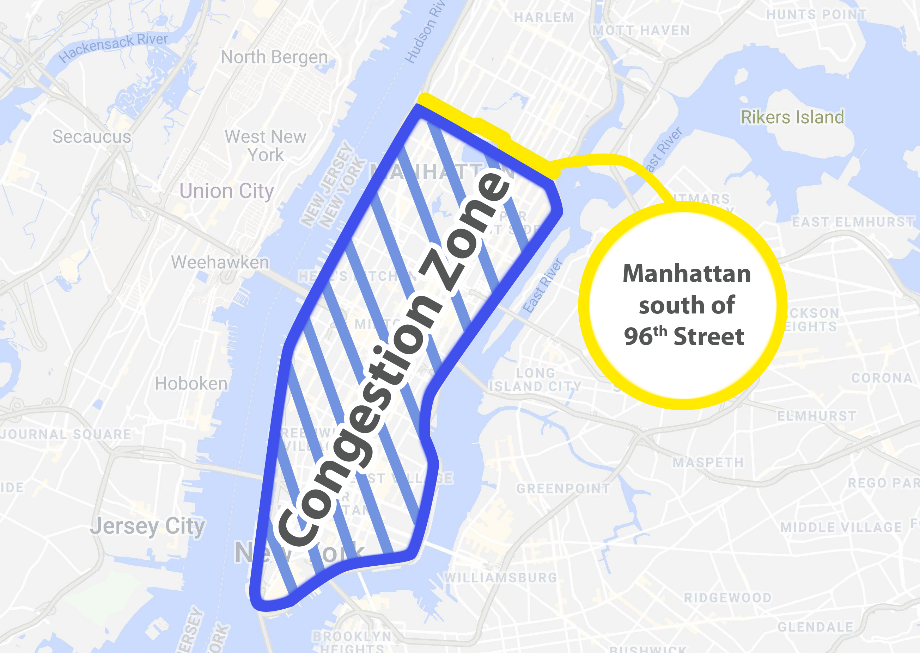

While the institutional benefits were clear, the microeconomic impact on individual commuters and small businesses created significant friction. The plan proposed a $15 base toll for passenger vehicles entering Manhattan south of 60th Street during peak hours. For a daily commuter, this represented a significant new line item in their personal budget.

The $15 Base Toll: Budgeting for the Daily Commute

For a professional commuting into the CBD five days a week, the congestion fee would total approximately $75 per week, or roughly $3,750 per year. This is a post-tax expense, meaning a commuter in a high-tax bracket would need to earn significantly more in gross income just to cover the cost of entering the city.

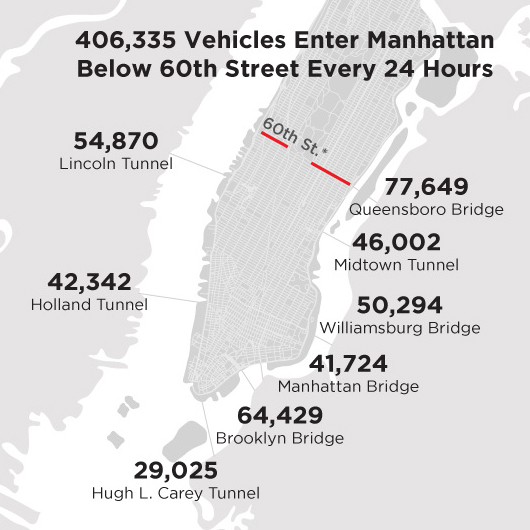

When combined with existing tolls (such as those for the Holland or Lincoln Tunnels) and the skyrocketing cost of parking in Manhattan, the “all-in” cost of driving became a luxury. The plan’s financial design was intentionally “regressive” in its pressure—aiming to price out those for whom the trip was not strictly necessary, thereby forcing a shift toward mass transit. However, critics argued that for low-income workers who live in “transit deserts” with no viable subway or bus options, the toll acted as an unavoidable tax on their livelihood.

Exemptions and the Financial Burden on Small Businesses

The financial complexity of the plan was further complicated by the debate over exemptions. Every group—from teachers and police officers to specialized contractors—sought a “financial carve-out.” From a fiscal management standpoint, every exemption granted reduced the $1 billion revenue target, potentially jeopardizing the $15 billion bond issuance.

Small businesses within the zone expressed concern regarding the “double-hit” to their finances. Not only would their suppliers likely pass the cost of the truck tolls down to them through higher delivery fees, but their customer base might shrink if discretionary shoppers chose to avoid the zone to save the $15 fee. This created a tension between the macro-goal of funding the subway and the micro-goal of maintaining a vibrant, accessible retail environment.

The $15 Billion Funding Void: Postponement and Financial Uncertainty

In June 2024, just weeks before the program was set to launch, the plan was placed on an “indefinite hiatus” by Governor Kathy Hochul. While the stated reasons were centered on the cost of living for everyday New Yorkers, the decision sent shockwaves through the financial markets and the MTA’s executive offices.

The Consequences for the 2020-2024 Capital Plan

The sudden removal of the congestion pricing revenue created an immediate $15 billion hole in the MTA’s capital budget. Infrastructure projects are not easily paused; they involve long-term contracts, specialized labor, and procurement cycles that span years. The delay forced the MTA to “de-prioritize” dozens of projects.

Financially, this is a disaster for long-term asset management. Delaying a $100 million signal upgrade today often results in a $200 million emergency repair five years from now. Furthermore, the MTA had already spent over $500 million on the physical infrastructure of the plan—installing the gantries, cameras, and software required to process the tolls. Without the revenue flowing in, that $500 million represents a “sunk cost” with no immediate ROI (Return on Investment).

Alternative Funding Sources and the “Taxation” Debate

With the $15 billion gap looming, the conversation has shifted toward alternative revenue streams. Proposals have included a new payroll tax on New York City businesses or diverting general fund tax revenue. However, these options lack the “user-pays” logic of congestion pricing.

From a business finance perspective, a payroll tax is a tax on employment, whereas congestion pricing is a tax on consumption (specifically, the consumption of road space). Investors and credit rating agencies, such as Moody’s and Standard & Poor’s, have closely monitored this situation. The MTA’s credit rating is tied to its ability to demonstrate a clear, reliable path to funding its obligations. The political instability surrounding the congestion pricing revenue has introduced a “risk premium” to the MTA’s financial outlook.

Lessons in Urban Macroeconomics and Future Financial Stability

The New York congestion pricing plan serves as a masterclass in the challenges of modernizing urban financial systems. It highlights the difficulty of transitioning from a 20th-century model of “free” roads to a 21st-century model of priced infrastructure.

Value Capture and Long-Term Infrastructure Investment

The plan’s legacy, regardless of its current status, is the formalization of “value capture” in the New York discourse. It forced a public realization that the “free” road is a myth; it is paid for through congestion, pollution, and the slow decay of the transit system. By attempting to put a price on the CBD, the city was attempting to treat its streets like a valuable utility—similar to electricity or water—where usage is metered to ensure the sustainability of the network.

For other global cities watching New York, the lesson is one of financial courage versus political reality. London, Stockholm, and Singapore have successfully implemented similar “Money-first” approaches to traffic, resulting in more reliable transit systems and more efficient local economies.

The Path Forward: Balancing the Books

As New York grapples with its $15 billion deficit, the congestion pricing plan remains the only “shovel-ready” financial solution on the table. Whether it is eventually implemented in its original form or modified with a lower base toll (e.g., $9 instead of $15), the underlying economic reality remains: the city’s transit infrastructure requires a massive infusion of capital that the current tax structure cannot provide.

In the final analysis, the New York congestion pricing plan was a sophisticated financial instrument designed to securitize the city’s most congested assets. It represented a shift toward a more corporate style of municipal management—where revenue must be identified before debt is incurred, and where the users of a system are the primary investors in its future. Until a comparable $15 billion funding mechanism is identified, the ghost of congestion pricing will continue to haunt the city’s balance sheets and the MTA’s long-term viability.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.