In the dynamic world of personal finance, understanding the cost of borrowing is paramount, especially when it comes to significant purchases like a new or used vehicle. Auto loan interest rates are not static; they fluctuate constantly, influenced by a complex interplay of global economic trends, central bank policies, and individual financial health. For anyone contemplating a vehicle purchase, asking “what are vehicle interest rates right now?” is not just a casual inquiry—it’s the first step towards making a financially sound decision.

The current climate for vehicle interest rates is shaped by a period of significant economic adjustment. Following an era of historically low rates, central banks worldwide have been actively engaged in monetary tightening to combat inflation. This aggressive stance has had a ripple effect across all forms of lending, including auto loans. While the broad direction might be clear, the specific rate you qualify for can vary dramatically, hinging on factors ranging from your credit score to the type of vehicle you choose and even the specific lender you engage with. This article will delve into the present state of vehicle interest rates, exploring the forces that drive them, the personal factors that dictate your eligibility, and actionable strategies to secure the most favorable terms for your next car purchase.

Understanding the Current Landscape of Vehicle Interest Rates

The journey to understanding today’s auto loan rates begins with a look at the broader economic environment and how it translates into the borrowing costs you encounter at dealerships and financial institutions.

The Impact of Federal Reserve Policy

At the heart of the U.S. financial system, the Federal Reserve (the Fed) plays a pivotal role in setting the tone for interest rates. Through its Federal Open Market Committee (FOMC), the Fed targets the federal funds rate, which is the benchmark rate banks use to lend to each other overnight. When the Fed raises this rate, it signals a general increase in borrowing costs across the economy. Banks, in turn, pass these higher costs on to consumers in the form of increased interest rates for various loans, including auto loans.

In recent years, the Fed has undertaken a series of aggressive rate hikes aimed at cooling down an overheated economy and bringing inflation under control. While these hikes have slowed down considerably, or even paused, in recent periods, their cumulative effect means that current auto loan rates remain significantly higher than they were a few years ago. Each FOMC meeting and subsequent announcement can cause shifts in market expectations, which in turn influence the rates offered by lenders. Therefore, staying abreast of Fed decisions is crucial for understanding the prevailing interest rate environment.

Key Economic Indicators Affecting Rates

Beyond direct Fed action, several broader economic indicators contribute to the volatility and direction of vehicle interest rates:

- Inflation: Persistent inflation often prompts the Fed to maintain higher interest rates to curb consumer spending and cool price increases. When inflation remains elevated, lenders typically demand higher rates to compensate for the erosion of purchasing power over the life of the loan.

- Consumer Confidence and Spending: A robust economy with high consumer confidence generally leads to increased demand for vehicles. While strong demand can sometimes support higher prices, it can also lead to more competitive lending if lenders are eager to capture market share. Conversely, if consumer confidence wanes, lenders might become more cautious, potentially adjusting rates or lending criteria.

- Employment Data: A strong job market, characterized by low unemployment and wage growth, suggests economic stability and consumers’ ability to repay debts. This can, paradoxically, give the Fed more leeway to keep rates higher if inflation concerns persist. A weakening job market, however, might signal an economic slowdown, potentially leading to future rate cuts to stimulate activity.

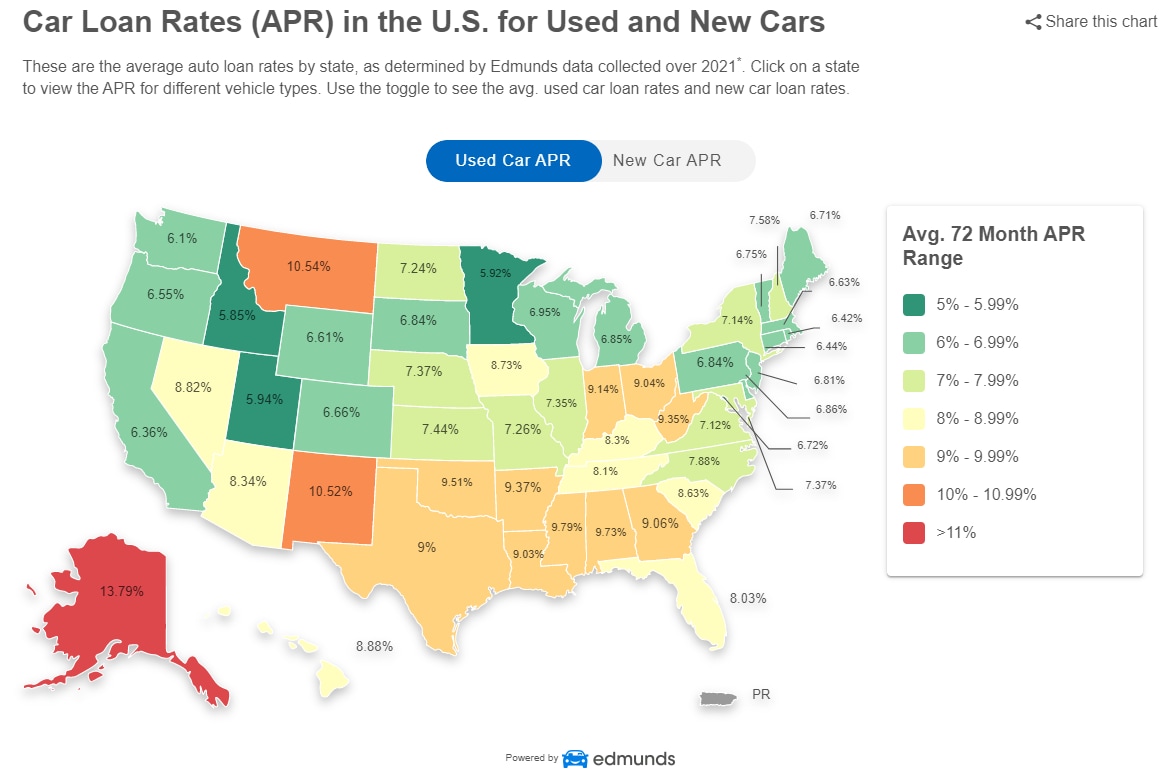

Average Rates: New vs. Used Vehicles

Generally speaking, interest rates for used vehicle loans tend to be higher than those for new vehicles. This disparity arises from several factors. Used cars typically carry a higher risk for lenders due to their unknown history, potential for mechanical issues, and faster depreciation. The loan terms for used cars are also often shorter, which, while reducing total interest paid, can lead to higher monthly payments.

Currently, for borrowers with excellent credit (FICO score 780+), new car loan rates might range from approximately 6% to 9%, though promotional rates from manufacturers can sometimes dip lower. For used cars, those with excellent credit might see rates anywhere from 7% to 11%. As credit scores decrease, these rates can climb significantly, potentially reaching 15% or even higher for individuals with fair or poor credit. It’s important to remember these are broad averages; actual rates are subject to individual lender policies and current market conditions.

Factors That Influence Your Specific Auto Loan Rate

While macroeconomic conditions set the overall interest rate framework, your personal financial profile plays an equally critical role in determining the exact rate you’ll be offered. Lenders assess various factors to gauge your creditworthiness and the risk associated with lending to you.

The Crucial Role of Your Credit Score

Your credit score is arguably the most significant factor in securing a favorable auto loan rate. Lenders use it as a snapshot of your financial reliability and your history of managing debt. Generally, credit scores fall into tiers:

- Excellent (780+): Borrowers in this category are considered low-risk and typically qualify for the lowest available interest rates.

- Good (670-779): These borrowers still qualify for competitive rates, though they might be slightly higher than those with excellent credit.

- Fair (580-669): Individuals in this range will likely face higher interest rates due to a perceived moderate risk.

- Poor (Below 580): Borrowers with poor credit are considered high-risk and will often be subject to the highest interest rates, if approved at all.

A difference of even 50-100 points in your credit score can translate into several percentage points difference in your interest rate, significantly impacting the total cost of your loan over its lifetime.

Loan Term Length: Short vs. Long

The length of your auto loan (the term) also directly impacts the interest rate. Shorter loan terms, such as 36 or 48 months, generally come with lower interest rates. Lenders perceive less risk over a shorter period, as there’s less time for economic conditions to change or for the vehicle to depreciate substantially. However, shorter terms result in higher monthly payments.

Conversely, longer loan terms (e.g., 72 or 84 months) often come with higher interest rates. While longer terms make monthly payments more affordable by stretching the repayment period, the total amount of interest paid over the life of the loan can be considerably greater. This is a trade-off many borrowers face: lower monthly payments versus a higher total cost of ownership.

Down Payment and Trade-In Value

The amount of money you put down upfront, either through a cash down payment or the equity from a trade-in vehicle, directly influences your loan-to-value (LTV) ratio. A larger down payment reduces the principal amount you need to borrow, which decreases the lender’s risk. A lower LTV often translates to a better interest rate.

Having a significant down payment also demonstrates financial discipline and commitment, which lenders appreciate. If you have positive equity in a trade-in, it functions similarly to a cash down payment, reducing the amount you need to finance and potentially lowering your interest rate.

Lender Type and Competition

The type of lender you choose can also impact the interest rate you receive. Auto loans are available from a variety of sources:

- Banks: Large national and regional banks offer a range of auto loan products.

- Credit Unions: Often known for offering competitive rates and more personalized service due to their member-owned structure.

- Captive Finance Companies: These are financing arms owned by car manufacturers (e.g., Toyota Financial Services, Ford Credit). They frequently offer promotional rates, including 0% APR deals, for specific models, especially new vehicles.

- Online Lenders: A growing segment offering quick approvals and competitive rates, often specializing in different credit profiles.

Shopping around and comparing offers from multiple types of lenders can lead to discovering the best rates, as each lender has different risk assessments and pricing models.

Strategies for Securing the Best Possible Auto Loan Rate

Given the current interest rate environment, being proactive and strategic about your auto loan is more important than ever. Here are actionable steps you can take to position yourself for the most favorable terms.

Improving Your Credit Score Before Applying

Since your credit score is such a critical determinant of your interest rate, taking steps to improve it before applying for a loan can save you thousands of dollars over the life of the loan.

- Pay Bills On Time: Payment history is the most significant factor in your credit score. Ensure all your credit card, loan, and utility bills are paid by their due dates.

- Reduce Existing Debt: Lowering your credit utilization ratio (the amount of credit you’re using compared to your total available credit) can quickly boost your score. Pay down credit card balances and other revolving debts.

- Check Your Credit Report for Errors: Obtain free copies of your credit report from Equifax, Experian, and TransUnion. Dispute any inaccuracies, as these can negatively impact your score.

- Avoid New Credit Applications: Limit applications for new credit cards or loans in the months leading up to your car purchase, as each application can temporarily ding your score.

Shopping Around for Loan Offers

Never take the first loan offer you receive, especially from a dealership. Instead, treat loan shopping with the same diligence as car shopping.

- Get Pre-Approved: Apply for pre-approval from several lenders (banks, credit unions, online lenders) before visiting a dealership. Pre-approval gives you a solid offer with a specific interest rate, empowering you to negotiate with confidence. It also lets you know exactly what you can afford, separating the financing from the vehicle price.

- Compare APRs (Annual Percentage Rates): When comparing offers, focus on the APR, which includes not only the interest rate but also any fees associated with the loan, providing a true total cost of borrowing.

- Understand the “Shopping Window”: Multiple credit inquiries for the same type of loan within a short period (typically 14-45 days, depending on the scoring model) are usually grouped as a single inquiry, minimizing the impact on your credit score. This allows you to shop around without significant penalty.

The Power of Negotiation Beyond the Sticker Price

While you might focus heavily on negotiating the vehicle’s price, don’t overlook the opportunity to negotiate the interest rate offered by the dealership’s finance department.

- Leverage Pre-Approvals: If the dealership’s finance department can beat your pre-approved rate, they may earn your business. If not, you have a solid backup.

- Be Prepared to Walk Away: If a deal doesn’t feel right, or the interest rate is unacceptably high, be willing to walk away. There are always other vehicles and other lenders.

- Negotiate the Whole Deal: Focus on the “out-the-door” price and the total cost of the loan, not just the monthly payment. A lower monthly payment over a longer term with a higher interest rate can cost you much more in the long run.

Understanding the Total Cost of Ownership

Beyond the interest rate and monthly payment, consider the total cost of owning the vehicle. This holistic view helps put the loan into perspective.

- Insurance: Get quotes for insurance on the specific vehicle you’re considering, as some models are significantly more expensive to insure.

- Maintenance and Fuel: Factor in anticipated maintenance costs and fuel efficiency, especially with fluctuating gas prices.

- Calculate Total Interest Paid: Use an online auto loan calculator to see how much interest you’ll pay over the life of the loan at different rates and terms. This stark figure can highlight the financial impact of a seemingly small difference in interest percentage.

Navigating Special Financing and Future Rate Projections

The landscape of auto finance also includes special offers and requires an eye toward future economic shifts that could impact your financial decisions.

Manufacturer Incentives and Promotional Rates

Car manufacturers often offer incentives to boost sales, especially for new models or to clear out older inventory. These can include:

- 0% APR Offers: These are highly attractive but typically reserved for buyers with excellent credit and usually for shorter loan terms (e.g., 36 or 48 months). While enticing, compare them carefully against cash back offers, as sometimes taking a rebate and financing at a slightly higher rate with your own lender can be a better deal, particularly if you prefer a longer loan term.

- Cash Back Offers: These are direct rebates that reduce the vehicle’s purchase price. You can use this to lower the amount you need to finance.

- Special Lease Deals: While not a loan, leasing offers can also provide competitive monthly payments and access to new vehicles without the long-term commitment of ownership.

Always read the fine print on these offers, as they may have strict eligibility requirements or hidden limitations.

When to Refinance Your Auto Loan

If you’ve already financed a vehicle, the current interest rate environment might make you wonder about refinancing. Refinancing can be a smart move in several scenarios:

- Improved Credit Score: If your credit score has significantly improved since you initially financed your vehicle, you might qualify for a much lower interest rate now.

- Lower Market Rates: While current rates are generally higher than a few years ago, if the market shifts downward, refinancing could be beneficial.

- Change in Financial Situation: If you have more disposable income now, you might refinance to a shorter term to save on total interest. Conversely, if you need to lower your monthly payments, a longer term (with potentially higher interest) might be an option, though often not ideal.

Refinancing involves applying for a new loan to pay off your existing auto loan. It’s essential to compare the new loan’s APR and fees against your current loan’s remaining term and interest to determine if the savings are substantial enough to justify the effort.

What the Future Holds for Auto Loan Rates

Predicting future interest rates with certainty is impossible, but economists and financial analysts constantly provide projections based on prevailing trends and anticipated policy changes.

- Federal Reserve Stance: The primary driver for future rates will continue to be the Federal Reserve’s response to inflation and economic growth. If inflation is tamed, the Fed may consider cutting rates, which would eventually trickle down to auto loans. If inflation proves persistent, rates could remain elevated.

- Economic Growth: A strong economy might allow for sustained higher rates, while a recessionary environment could prompt rate cuts to stimulate borrowing and spending.

- Market Competition: The competitive landscape among lenders can also influence rates. Fierce competition might lead to lenders offering slightly better rates to attract customers, even in a higher-rate environment.

For consumers, the best strategy is to stay informed about economic news and Fed announcements. While it’s tempting to try and time the market, focusing on your personal financial health—especially your credit score—is the most reliable way to ensure you’re always in a strong position to secure the best rates available, regardless of market fluctuations.

Conclusion

Understanding “what are vehicle interest rates right now” is more than just knowing a number; it’s about comprehending the forces that shape that number and, more importantly, recognizing the levers you can pull to influence the rate you receive. In today’s economic climate, marked by elevated interest rates stemming from inflation-fighting monetary policies, being an informed and prepared borrower is crucial.

From the macroeconomic influence of the Federal Reserve and broader economic indicators to the personal impact of your credit score, loan term, and down payment, myriad factors converge to determine your auto loan’s cost. By actively working to improve your credit, diligently shopping around for pre-approvals, and understanding the total cost beyond just the monthly payment, you empower yourself to navigate the complexities of vehicle financing. The journey to a new car should be exciting, and by taking control of your financial strategy, you can ensure that excitement isn’t overshadowed by an unfavorable loan. Be informed, be prepared, and drive away with confidence in your financial decision.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.