The thought of an IRS audit can send a shiver down anyone’s spine. It conjures images of scrutiny, paperwork mountains, and the potential for unexpected tax bills. But how likely is it, really, to find yourself in the auditor’s crosshairs? Understanding the odds of an IRS audit is crucial, not just to alleviate anxiety, but also to inform your financial practices and ensure you’re minimizing unnecessary risk. While the IRS conducts audits to ensure compliance with tax laws, the process isn’t random; several factors influence the likelihood of an audit, and a proactive approach can significantly reduce your chances.

The IRS’s auditing resources are finite, meaning they must prioritize where they allocate their time and expertise. This prioritization is driven by a desire to maximize tax revenue collection and ensure fairness within the tax system. Therefore, audits are more likely to be triggered by certain behaviors, complexities, or red flags than by simply picking names out of a hat. For the average taxpayer, the probability of being audited is relatively low. However, for individuals and businesses with more complex financial situations, a history of audits, or those engaging in specific types of transactions, the odds can increase. This article will delve into the factors that influence IRS audit rates, explore what types of taxpayers are more likely to be audited, and offer actionable advice on how to stay off the IRS’s radar.

Understanding the IRS Audit Landscape

The IRS audit process is designed to verify the accuracy of tax returns filed by individuals and businesses. It’s not a punitive measure in itself, but rather a compliance mechanism. The IRS uses a variety of methods to select returns for audit, with a significant portion being determined by computer algorithms that identify potential discrepancies or inconsistencies. These algorithms, often referred to as the Discriminant Information Function (DIF) system, score tax returns based on various factors. Returns with higher DIF scores are more likely to be selected. These scores are developed through statistical analysis of past audits, identifying patterns that are associated with underreporting of income or overstating deductions.

Who is the IRS Targeting?

While the overall audit rate for individual taxpayers remains low, the IRS does focus its resources on specific areas and types of filers. These include:

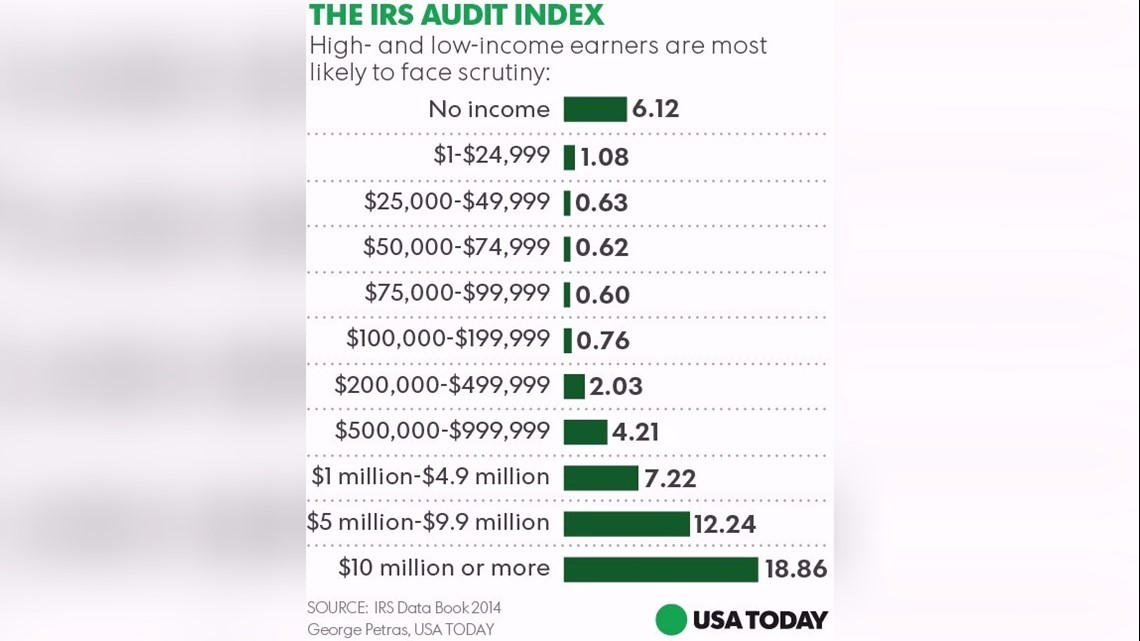

- High-Income Individuals: Taxpayers with higher Adjusted Gross Incomes (AGIs) generally face a higher audit probability. This is because their tax returns are often more complex, involve a wider range of investments and deductions, and represent a larger potential for tax revenue. The IRS dedicates significant resources to auditing these individuals to ensure compliance with intricate tax laws applicable to substantial wealth.

- Businesses and Self-Employed Individuals: Businesses, particularly those with significant revenue or complex accounting practices, are more frequently audited than individual wage earners. This is due to the greater potential for errors or intentional misstatements in business expenses, deductions, and income reporting. Self-employed individuals, who often claim a variety of business expenses, are also more closely monitored.

- Cash-Intensive Businesses: Businesses that primarily operate on cash transactions, such as restaurants, retail stores, or service providers, are at a higher risk of audit. The nature of cash transactions makes it easier to underreport income, and the IRS actively seeks to identify such instances.

- Taxpayers with Foreign Income or Assets: The IRS has increased its focus on individuals and entities with international financial dealings. This includes reporting requirements for foreign bank accounts, foreign earned income, and various international investments. Non-compliance in these areas can trigger an audit.

- Taxpayers Claiming Large or Unusual Deductions: While claiming legitimate deductions is a cornerstone of tax planning, unusually large deductions or deductions that appear out of proportion to income can raise a red flag. For example, claiming a home office deduction on a tax return that doesn’t reflect significant business activity, or claiming an unusually high charitable contribution, could prompt further review.

The IRS also uses Information Matching Programs. This involves comparing the information reported on your tax return with information reported by third parties, such as your employer (W-2s), banks (1099s for interest and dividends), and brokerage firms. If there’s a discrepancy, it can lead to an automated notice or, in some cases, an audit.

Factors That Increase Your Audit Risk

Beyond demographic and business-related factors, specific actions or omissions on your tax return can significantly elevate your chances of an IRS audit. Understanding these triggers is paramount to proactive tax planning.

Heading3: Red Flags on Your Tax Return

Certain elements on your tax return are more likely to catch the IRS’s attention. These are often indicators of potential errors, omissions, or aggressive tax positions.

- Discrepancies in Income Reporting: This is perhaps the most significant red flag. Failing to report all sources of income, whether from employment, investments, side hustles, or freelance work, is a common reason for an audit. The IRS’s information matching programs are highly effective at catching underreported income. For instance, if you received a 1099 for freelance work but did not report that income on your tax return, the IRS will likely flag it.

- Excessive or Unsubstantiated Deductions: While taking legitimate deductions is encouraged, claiming deductions that seem disproportionate to your income or are not well-documented can be problematic. This includes deductions for business expenses, charitable contributions, or medical expenses. The IRS expects you to have receipts and records to support all claims. Aggressively claiming deductions without proper substantiation is a clear invitation for scrutiny.

- Business Use of Your Home: The home office deduction, while legitimate for those who qualify, is often a point of interest for auditors. The IRS scrutinizes these deductions to ensure they are not being used to improperly deduct personal expenses. Strict rules apply, and claiming this deduction without meeting all criteria can lead to an audit.

- Complex Transactions or Investments: Engaging in intricate financial transactions, such as those involving cryptocurrency, complex derivatives, or offshore accounts, can increase your audit risk. These areas are often subject to specific reporting requirements and can be more prone to errors or omissions.

- High Volume of Deductions: While not an automatic trigger, a tax return with an exceptionally high number of deductions compared to similar income levels might prompt further investigation. This suggests a potential for overstating or fabricating deductions.

- Claiming Losses That Seem Unrealistic: Significant losses, particularly those related to business activities or investments, can be a trigger. The IRS wants to ensure these losses are legitimate and not being used to artificially reduce taxable income. They may look for evidence of a true business intent or a genuine investment strategy.

Heading3: History of Audits and Past Issues

If you’ve been audited in the past and found to have significant discrepancies, you may be placed on a list for future audits. The IRS considers taxpayers with a history of non-compliance or substantial tax adjustments as higher risk. They may be subject to more frequent audits to ensure ongoing compliance. This doesn’t mean every past audit will lead to another, but it does increase the probability. Similarly, if you’ve had issues with tax debt or payment arrangements, this could also influence future IRS attention.

Minimizing Your Audit Risk: Proactive Strategies

While you can’t completely eliminate the possibility of an IRS audit, you can significantly reduce your chances by adopting careful and conscientious tax practices. This involves not only understanding the rules but also meticulously documenting your financial activities.

Heading3: The Power of Diligent Record-Keeping

This is the cornerstone of audit-proof tax preparation. The IRS requires you to keep records that support the income, deductions, and credits you claim on your tax return.

- Organize and Retain Documentation: This includes receipts for all expenses, bank statements, canceled checks, investment statements, records of income (W-2s, 1099s, invoices), and any other relevant financial documents. Consider using digital tools for organization, such as cloud storage or dedicated accounting software.

- Keep Records for the Required Period: The IRS generally recommends keeping tax records for at least three years from the date you filed your return or the due date of the return, whichever is later. For certain assets like property, you may need to keep records for longer, even after you sell them.

- Specific Record-Keeping for Deductions: For common areas of audit focus, such as business expenses or the home office deduction, meticulous record-keeping is even more critical. Maintain detailed logs, receipts, and any other documentation that clearly substantiates your claims. This could include mileage logs for business travel, or documentation proving your home office is your principal place of business.

Heading3: Leveraging Technology for Accuracy and Compliance

In today’s digital age, technology offers powerful tools to enhance tax preparation accuracy and streamline record-keeping, thereby reducing audit risk.

- Tax Preparation Software: Reputable tax preparation software can guide you through the tax filing process, helping to avoid common errors and flag potentially questionable deductions. Many programs include built-in checks for accuracy and completeness.

- Accounting Software for Businesses: For self-employed individuals and businesses, accounting software is invaluable. It helps track income and expenses in real-time, generates financial reports, and ensures that all transactions are properly recorded and categorized. This organization makes it much easier to justify deductions during an audit.

- Digital Record-Keeping Apps: Numerous apps are available that allow you to scan and store receipts digitally, categorize expenses, and even track mileage. This not only makes record-keeping more convenient but also ensures your documentation is easily accessible and well-organized.

- Financial Dashboards and Aggregators: Tools that aggregate your financial information can provide a clear overview of your income and spending, helping you identify any discrepancies or unacknowledged income sources.

Heading3: Professional Guidance and Prudent Tax Planning

While technology is a powerful ally, professional tax advice remains invaluable for navigating complex tax laws and optimizing your tax strategy.

- Consult a Tax Professional: A qualified tax advisor, such as a Certified Public Accountant (CPA) or an Enrolled Agent (EA), can provide expert guidance on tax laws, help identify legitimate deductions and credits you might be eligible for, and ensure your tax return is prepared accurately and compliantly. They can also advise on how to document your financial activities effectively.

- Avoid Aggressive Tax Positions: While it’s beneficial to utilize all legal tax advantages, avoid taking aggressive or questionable tax positions that lack clear legal precedent or sufficient substantiation. It’s better to be conservative and ensure your claims are well-supported.

- Understand Reporting Requirements: Familiarize yourself with all relevant tax reporting requirements, especially if you engage in complex financial activities, have foreign income, or operate a business. Non-compliance with reporting obligations is a significant audit trigger.

In conclusion, while the odds of an IRS audit for the average individual are low, they are not zero. By understanding the factors that increase audit risk – from income complexities and unusual deductions to inadequate record-keeping – you can take proactive steps to minimize your exposure. Embracing meticulous documentation, leveraging modern technology, and seeking professional guidance are your strongest defenses. A well-prepared and accurately filed tax return, supported by robust records, is the most effective way to ensure peace of mind and avoid the unwelcome attention of an IRS audit.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.