The dream of instant wealth has captivated humanity for centuries, and in the modern era, few avenues offer the tantalizing promise of life-altering riches quite like the lottery. From the humble convenience store counter to online platforms, the allure of striking it rich with a single ticket is a powerful motivator. For many, simply knowing “what are the current lottery jackpots” is more than just idle curiosity; it’s a quick mental calculation of dreams, possibilities, and perhaps, a small, justifiable splurge on a ticket. This article delves into the world of lottery jackpots, not just as a fleeting fantasy, but from a practical financial perspective, exploring how to track them, understanding the odds, and the critical financial considerations that come with such immense potential winnings.

The Allure and Reality of Multi-Million Dollar Dreams

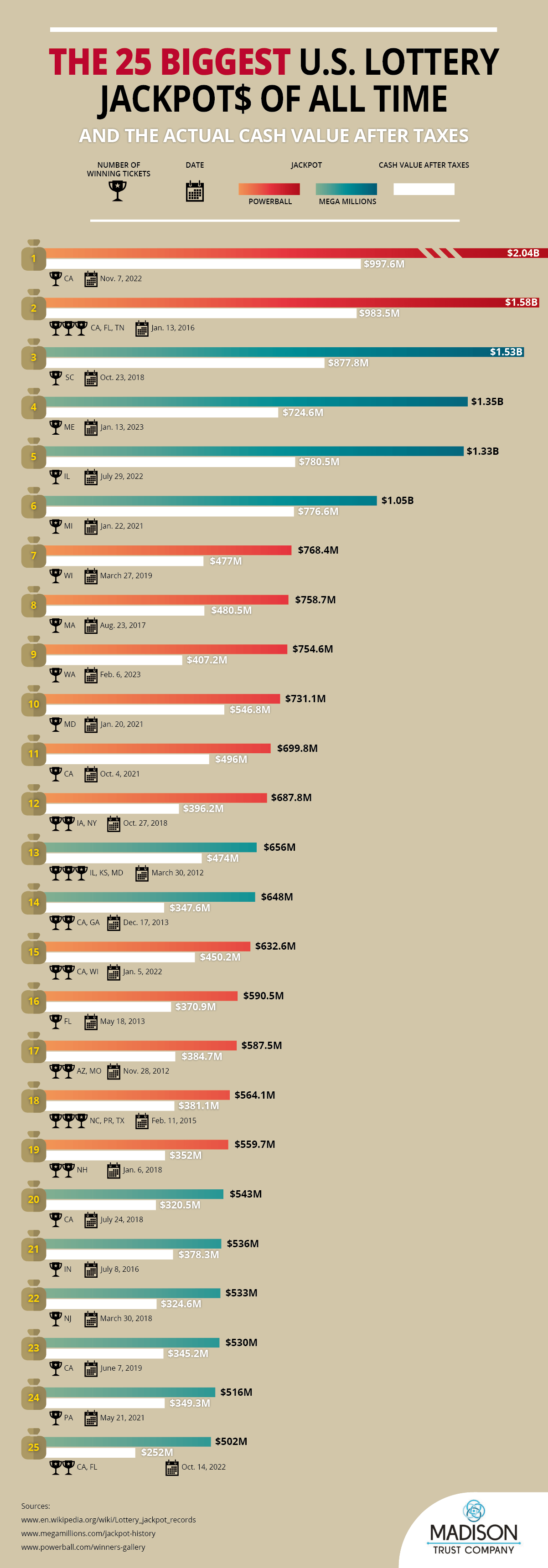

The sheer scale of top lottery jackpots often makes headlines, fueling water cooler conversations and inspiring countless purchases. These aren’t just small sums; they represent astronomical figures capable of transforming not just an individual’s life, but potentially generations of a family.

Tracking the Titans: Powerball and Mega Millions

In the United States, two names dominate the national lottery landscape: Powerball and Mega Millions. These multi-state lotteries are renowned for their staggering jackpots, which frequently climb into the hundreds of millions and, on occasion, even exceed a billion dollars.

- Powerball: Played in 45 states, the District of Columbia, Puerto Rico, and the U.S. Virgin Islands, Powerball draws happen three times a week (Mondays, Wednesdays, and Saturdays). Its jackpot starts at a respectable $20 million and grows with each draw where no one wins the top prize. The structure involves picking five white balls from a drum of 69 and one red Powerball from a drum of 26.

- Mega Millions: Similarly, Mega Millions is offered in 45 states, the District of Columbia, and the U.S. Virgin Islands, with draws held on Tuesdays and Fridays. Its jackpot also starts at $20 million, rollovers increasing its value significantly. Players select five numbers from 1 to 70 and one Mega Ball number from 1 to 25.

Tracking the current jackpots for these behemoths is straightforward. Official lottery websites (e.g., Powerball.com, MegaMillions.com) are the most accurate sources, updated immediately after each draw. Reputable news outlets, financial news sites, and dedicated lottery apps also provide real-time jackpot figures. The thrill lies in watching these numbers swell, particularly after a long streak of rollovers, creating a palpable excitement as they approach record-breaking levels. Understanding the current jackpot means not just seeing a number, but grasping the potential scale of its financial impact.

Beyond the Giants: State-Specific and International Lotteries

While Powerball and Mega Millions capture the lion’s share of national attention, a vibrant ecosystem of state-specific lotteries offers additional opportunities, often with more favorable (though still long) odds for substantial wins. States like California (e.g., SuperLotto Plus), New York (e.g., New York Lotto), Florida (e.g., Florida Lotto), and others run their own draw games with jackpots that, while typically smaller than the national games, can still reach tens of millions of dollars. These local games cater to regional players and sometimes offer better secondary prizes or different game formats.

Beyond national and state borders, the lottery phenomenon is global. European lotteries like EuroMillions and Eurojackpot, or even specific national lotteries in countries like Canada, Australia, or the UK, can also feature impressive jackpots. While primarily designed for residents of those regions, the existence of such international games underscores the universal appeal of lottery-based wealth. For most players, however, focusing on accessible state and national lotteries is the practical approach to pursuing their jackpot dreams. The key takeaway is that “current lottery jackpots” isn’t a singular figure; it’s a dynamic landscape of opportunities, varying by location and game type, each with its own set of rules and potential rewards.

Understanding the Odds: A Financial Perspective

While the prospect of winning a massive jackpot is exhilarating, a grounded financial perspective requires a clear understanding of the statistical realities involved. The lottery is often described as a “tax on the mathematically challenged,” a somewhat harsh but stark reminder of the long odds.

The Statistical Truth

Let’s be unequivocally clear: the odds of winning a major lottery jackpot are astronomically low. To put it into perspective:

- Mega Millions: The odds of winning the grand prize are approximately 1 in 302.5 million.

- Powerball: The odds of hitting the jackpot are roughly 1 in 292.2 million.

These numbers are so vast they are often difficult to comprehend. To illustrate, you are far more likely to:

- Be struck by lightning (approximately 1 in 1.2 million in any given year).

- Be attacked by a shark (approximately 1 in 3.7 million over a lifetime).

- Be dealt a royal flush in poker on your first five cards (approximately 1 in 649,740).

- Even become a movie star (approximately 1 in 1.5 million).

Understanding these odds is crucial for maintaining a healthy financial perspective. Playing the lottery should not be confused with a sound investment strategy or a reliable path to financial security. It is, by definition, a game of chance where the probabilities heavily favor the house (the lottery organizers). From a purely mathematical standpoint, the statistical truth reveals that while possible, a jackpot win is an incredibly improbable event.

Expected Value and Rational Play

In finance and economics, the concept of “expected value” (EV) is used to determine the average outcome of a decision if it were to be repeated many times. For the lottery, the expected value is calculated by multiplying the probability of each outcome by its payoff, and then summing those values.

For nearly all lottery drawings, the expected value of a single ticket is negative. This means that, on average, for every dollar you spend on a lottery ticket, you can expect to get back less than a dollar. For example, if a ticket costs $2, and the EV is -$1.95, it means you’re statistically “losing” $1.95 for every ticket purchased. The only times EV might approach or slightly exceed zero (which is still not a good investment, just a “fair” bet) are when jackpots reach unprecedented, record-breaking levels, and even then, factors like multiple winners splitting the prize significantly dilute the EV.

Rational financial play, therefore, dictates that the lottery is not a method for wealth creation. Instead, it should be viewed as a form of entertainment. Just as one might spend money on a movie ticket or a concert, a lottery ticket can be purchased for the small thrill of the possibility, but with the full understanding that the money is highly unlikely to be recouped. Financial planners universally advise against relying on the lottery for retirement, debt repayment, or any other serious financial goal. Consistent saving, smart investing, and diligent budgeting are the bedrock of true financial growth, offering an expected value that is consistently positive over time.

Managing Expectations and Potential Windfalls

Should the impossible happen and you find yourself holding a winning lottery ticket, the journey is far from over. In fact, it’s just beginning, and it immediately transitions from a game of chance to a series of critical financial and legal decisions. Mismanaging a large windfall can lead to devastating consequences, as many past winners have unfortunately discovered.

Lump Sum vs. Annuity: A Critical Financial Decision

One of the first and most significant choices a mega-jackpot winner faces is how to receive their winnings: as a lump sum or an annuity.

-

Lump Sum (Cash Option): This option provides a single, immediate payment of the prize, but it is always a smaller amount than the advertised jackpot. The advertised jackpot represents the total value of an annuity paid over decades. When you choose the cash option, you receive the present value of that annuity. For example, a $500 million jackpot might have a cash option of around $250 million to $300 million before taxes.

- Pros: Immediate access to a large sum, which can be invested, used to pay off all debts, or fund large purchases. Allows the winner control over the investment strategy.

- Cons: Higher immediate tax burden (as the entire amount is taxed in one year). Risk of impulsive spending and quick depletion if not managed wisely. Requires significant financial discipline and expertise.

-

Annuity Payments: This option distributes the jackpot over a period, typically 29 years, paid out in 30 annual installments (the first payment is immediate, followed by 29 more). These payments usually increase by a certain percentage each year to account for inflation.

- Pros: Provides a stable, long-term income stream, protecting against immediate overspending. Spreads out the tax burden over many years. Offers a guaranteed income for decades.

- Cons: Less flexibility; the money is tied up. Inflation can erode the purchasing power of later payments, even with annual increases. If not structured correctly, could limit immediate investment opportunities.

The choice between a lump sum and an annuity is highly personal and depends on various factors, including the winner’s age, financial literacy, investment goals, and risk tolerance. It is absolutely imperative to consult with an independent financial advisor, an attorney, and a tax professional before claiming the prize to understand the full implications of each option.

The Taxman Cometh: Understanding Lottery Winnings Taxation

Regardless of whether a lump sum or an annuity is chosen, lottery winnings are subject to significant taxation. This is a critical factor often overlooked by those dreaming of the jackpot.

- Federal Income Tax: Lottery winnings are considered ordinary income by the IRS and are subject to federal income tax. For large jackpots, winnings will almost certainly push the recipient into the highest federal income tax bracket. The IRS typically withholds a mandatory 24% on winnings over $5,000, but the actual tax liability will be higher, potentially reaching 37% for the top bracket. This means a substantial portion of the winnings will be owed to the federal government.

- State and Local Taxes: In addition to federal taxes, many states also impose taxes on lottery winnings. State tax rates vary widely, from 0% in some states (e.g., California, Florida, Texas, Washington) to over 10% in others (e.g., New York, Maryland). Some cities may also have local income taxes. It’s crucial to understand the tax laws in the state where the ticket was purchased, as that typically dictates state tax liability, even if the winner resides elsewhere.

The combination of federal and state taxes can easily reduce a multi-million dollar jackpot by 40% or even more. This reality shock is why financial planning is paramount. Winners must budget for this tax burden, especially with the lump sum option, where a huge sum is taxed at once. A qualified tax advisor can help navigate the complexities, potentially identifying strategies (though limited for lottery winnings) to optimize the financial outcome post-tax. Understanding “what are the current lottery jackpots” must always be paired with the knowledge of how much of that theoretical sum will actually end up in your bank account after Uncle Sam and state governments take their share.

Responsible Participation and Alternative Financial Strategies

Given the overwhelming odds and significant tax implications, playing the lottery should always be approached with a sense of financial responsibility. It’s an indulgence, not an investment, and there are far more reliable paths to building genuine wealth.

Playing Responsibly: Budgeting for Entertainment

For many, playing the lottery is a harmless diversion—a small expenditure for a big dream. The key is to treat it as such: a form of entertainment, akin to buying a movie ticket or a magazine.

- Set a Strict Budget: Allocate a small, predetermined amount of discretionary income that you are comfortable losing. This budget should be so small that its loss would have absolutely no impact on your essential living expenses, savings, or debt repayment goals. Once that budget is spent for the week or month, stop playing.

- Avoid Chasing Losses: Never spend more than your budget to try and recoup previous losses. This is a hallmark of problem gambling.

- Don’t Overextend: Resist the urge to buy more tickets when jackpots reach record highs if it means exceeding your budget. The odds remain virtually unchanged regardless of the jackpot size.

- Recognize Problem Gambling Signs: If you find yourself spending more than you can afford, feeling guilty after playing, borrowing money to gamble, or experiencing negative impacts on your relationships or work due to gambling, seek help immediately. Resources like the National Council on Problem Gambling (ncpgambling.org) are available.

Responsible participation ensures that the dream of a jackpot remains a lighthearted fantasy rather than a financial pitfall. It’s about enjoying the “what if” without compromising your actual financial well-being.

Beyond the Lottery: Building Real Wealth

While keeping an eye on “what are the current lottery jackpots” can be fun, a genuine and sustainable path to financial security and wealth creation lies in time-tested, proven strategies that involve effort, discipline, and sound financial principles.

- Emergency Fund: Before any investing or speculative play, build a robust emergency fund covering 3-6 months of living expenses. This provides a crucial safety net.

- Debt Management: Prioritize paying off high-interest debt, such as credit card balances. The guaranteed return from eliminating high-interest debt far surpasses any lottery odds.

- Consistent Saving and Investing: This is the true engine of wealth.

- Retirement Accounts: Maximize contributions to 401(k)s, IRAs, and other tax-advantaged retirement vehicles.

- Diversified Investments: Invest regularly in a diversified portfolio of stocks, bonds, and other assets appropriate for your risk tolerance and time horizon. Compound interest is a powerful force that works silently over decades.

- Real Estate: Consider strategic real estate investments as a long-term asset and potential income stream.

- Skill Development and Side Hustles: Focus on increasing your earning potential through education, skill development, or by starting a side business. Generating active income is a direct and controllable way to build wealth.

- Budgeting and Financial Planning: Create a detailed budget, track your spending, and work with a financial advisor to develop a comprehensive financial plan tailored to your goals.

In conclusion, while the question “what are the current lottery jackpots” sparks imaginations and offers a momentary escape, a responsible financial outlook dictates that these games are primarily for entertainment. True financial freedom and stability are achieved not by hoping for a miraculous win, but through diligent planning, consistent saving, smart investing, and disciplined money management. The journey to wealth is a marathon, not a sprint won by a lottery ticket.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.