In the complex landscape of risk management and business finance, most consumers and business owners are familiar with the “standard” insurance market. These are the household names that provide auto, home, and general liability coverage—companies regulated strictly by state insurance departments to ensure rate consistency and consumer protection. However, not every risk fits neatly into a standardized box. When a business faces unique hazards, high-capacity requirements, or a history of significant losses, the standard market often steps back.

This is where “surplus lines” of insurance come into play. Often referred to as the “safety valve” of the insurance industry, the surplus lines market provides a critical financial infrastructure for risks that are too great or too unusual for traditional carriers to handle. For the modern entrepreneur, CFO, or high-net-worth investor, understanding how this market operates is essential for maintaining comprehensive financial security.

The Fundamentals of Surplus Lines Insurance

To understand surplus lines, one must first understand the distinction between “admitted” and “non-admitted” insurance carriers. This distinction is the bedrock of insurance regulation and financial protection in the United States.

Admitted vs. Non-Admitted Carriers

An “admitted” carrier is a company that has been formally licensed by a state’s department of insurance. These companies must follow state regulations regarding how they price their policies and what their policy forms contain. The primary benefit for the policyholder is the safety net: if an admitted carrier goes bankrupt, the state’s “guaranty fund” steps in to pay outstanding claims.

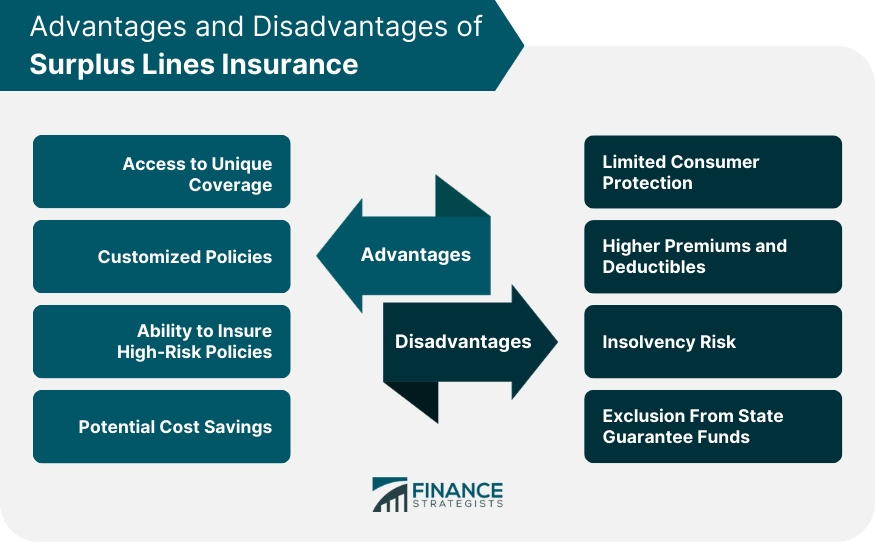

A surplus lines carrier is “non-admitted.” This does not mean they are unregulated or illegal; rather, it means they are not bound by the same rate and form regulations as admitted carriers. This freedom allows them to take on risks that admitted carriers cannot or will not touch. While they are not backed by state guaranty funds, surplus lines carriers are generally required to be financially stable and are often monitored by the state through “white lists” or eligibility requirements.

The Role of Flexibility in Financial Risk

The core value proposition of surplus lines is flexibility. Because they are not restricted by standardized pricing models, surplus lines insurers can tailor a policy to a specific, idiosyncratic risk. This is a vital component of business finance. If a company cannot find insurance, it cannot operate, secure loans, or satisfy contractual obligations. The surplus lines market ensures that even the most complex financial risks have a path to coverage, albeit often at a higher price point.

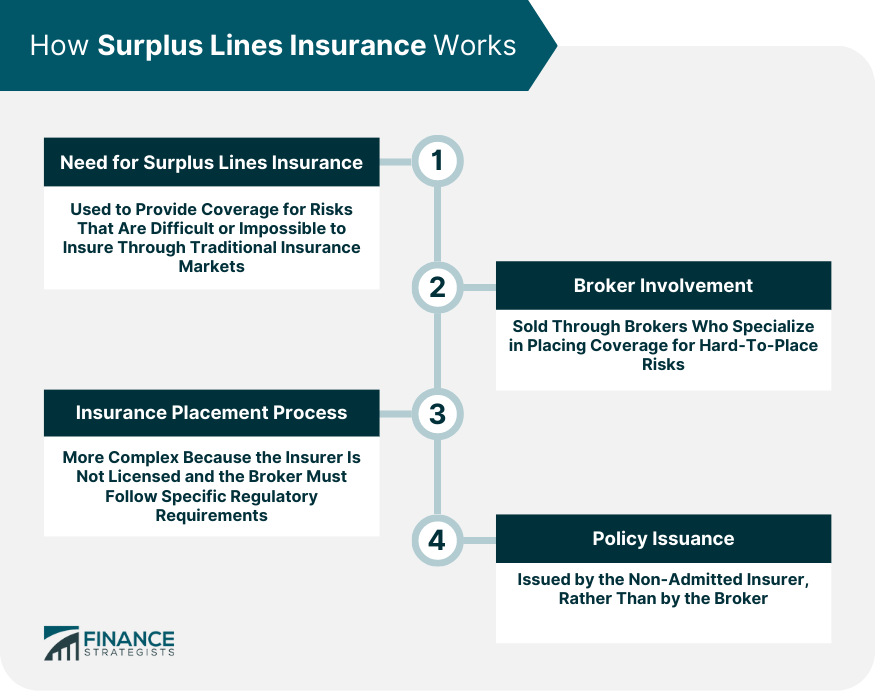

Why Businesses and Individuals Need the Surplus Lines Market

The necessity of the surplus lines market arises when the “admitted” market reaches its limit. This usually happens in three specific scenarios: high-risk operations, unique or emerging hazards, and capacity constraints.

High-Risk and High-Liability Operations

Certain industries are inherently more dangerous or prone to litigation than others. For example, a demolition company, a commercial roofing contractor, or a manufacturer of hazardous chemicals may find that standard carriers are unwilling to offer coverage due to the high probability of a catastrophic claim. In these instances, the surplus lines market provides the necessary liability coverage that allows these businesses to remain solvent and compliant with federal and state laws.

Unique, Unusual, or Emerging Risks

We live in an era of rapid technological and social change, and the insurance industry often struggles to keep up. When new risks emerge—such as the initial rise of cyber liability, the legalization of cannabis businesses, or the development of autonomous vehicles—standard insurers often lack the historical data needed to price these risks accurately. Surplus lines carriers act as the industry’s innovators. They design experimental policy forms and pricing structures for these emerging markets, providing a financial cushion for pioneers in new industries.

Capacity and Catastrophe-Prone Risks

Sometimes the risk isn’t “weird,” it’s just “big.” In areas prone to natural disasters, such as coastal Florida (hurricanes) or California (wildfires), the standard market may hit its “capacity.” An admitted carrier can only take on a certain amount of total risk in one geographic area before it threatens its own solvency. When standard carriers stop writing policies in these regions to protect their balance sheets, surplus lines carriers step in to provide the excess capacity needed to protect property values and regional economies.

The Regulatory Landscape and the “Diligent Effort” Search

Because surplus lines insurance lacks the protection of state guaranty funds, the regulatory framework is designed to ensure that these policies are used only when necessary. This is managed through a process known as the “diligent effort” search.

The Requirement for a Diligent Search

In most jurisdictions, a broker cannot simply place a client with a surplus lines carrier because it is faster or cheaper. By law, the broker must first attempt to place the risk with admitted carriers. Usually, the broker must receive declinations from three different admitted insurers before they are legally allowed to seek coverage in the surplus lines market. This ensures that the consumer is prioritized for the protections of the admitted market whenever possible.

The Role of the Surplus Lines Broker

Navigating this market requires specialized expertise. Most standard insurance agents do not have direct access to surplus lines carriers. Instead, they work through a “Wholesale Broker” or a “Surplus Lines Broker.” These professionals are licensed specifically to handle non-admitted placements. They act as the intermediary, ensuring that the financial health of the surplus lines carrier is sound and that the policy language provides the specific protection the client requires.

Understanding the Lack of Guaranty Fund Protection

One of the most important financial considerations for any business owner utilizing surplus lines is the absence of a guaranty fund. If a surplus lines insurer becomes insolvent, there is no state-backed pool of money to pay claims. Consequently, checking the “A.M. Best” or “Standard & Poor’s” financial strength rating of a surplus lines carrier is not just a formality—it is a critical step in financial due diligence. Most sophisticated buyers look for an “A” rating or higher to ensure the carrier has the capital reserves to meet its long-term obligations.

Navigating the Costs and Procurement Process

From a business finance perspective, surplus lines insurance is generally more expensive and administratively intensive than standard insurance. However, the cost of being uninsured is infinitely higher.

Pricing, Fees, and Premium Taxes

Surplus lines policies are not just priced based on the risk; they also carry additional financial burdens. Because these carriers do not pay the same state taxes as admitted companies, the responsibility for “Premium Tax” falls on the policyholder. This tax, which varies by state (usually between 2% and 6%), is added to the total cost of the policy. Additionally, surplus lines brokers often charge “inspection fees” or “policy fees” to cover the cost of the extensive underwriting required for unique risks.

The Underwriting Process

Unlike a standard auto policy that can be quoted in minutes, surplus lines underwriting is a meticulous process. The carrier will often require supplemental applications, engineering reports, and detailed financial statements. They want to understand the “story” behind the risk. For a business, this means maintaining impeccable records. The more data a business can provide regarding its safety protocols, loss history, and financial stability, the more leverage it has to negotiate better terms in the surplus lines market.

Strategic Value in a Financial Portfolio

While it might seem like a last resort, surplus lines insurance is actually a strategic tool for sophisticated financial planning. It allows businesses to pursue “high-alpha” opportunities—ventures that carry high risk but also high potential reward—by offloading the catastrophic financial downside to a carrier that understands that specific niche. By utilizing the surplus lines market, a company can venture into new territories, develop new products, and operate in volatile environments with the confidence that their balance sheet is protected against ruinous loss.

Conclusion

The surplus lines market is a vital engine of the global economy, providing the financial backstop for innovation, high-risk industries, and catastrophe-prone regions. While it operates with less direct oversight than the admitted market, its freedom to innovate and price risk accurately ensures that insurance remains available even when conditions are at their most challenging.

For those managing business finances or personal wealth, the surplus lines market should not be viewed with apprehension. Instead, it should be recognized as a sophisticated financial instrument. By working with expert brokers, performing due diligence on carrier ratings, and understanding the regulatory requirements of the “diligent search,” you can secure your financial future against the risks that standard insurance simply cannot handle. In the world of money and risk, the surplus lines market is the ultimate safety net, ensuring that no risk is truly uninsurable.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.