For homeowners, real estate investors, and financial planners, California’s property tax system represents one of the most significant and complex recurring expenses in a financial portfolio. Unlike many states where property taxes are reassessed annually based on current market values, California operates under a unique set of rules established decades ago. Understanding these nuances is not just a matter of compliance; it is a critical component of long-term wealth management and cash flow planning.

This guide explores the financial mechanisms governing California property taxes, the impact of historical legislation, and the strategies homeowners can use to manage their tax liabilities effectively.

The Foundation of California Real Estate: Proposition 13 and Tax Rates

To understand property taxes in California, one must first understand Proposition 13. Passed by voters in 1978, this landmark “taxpayer revolt” legislation fundamentally changed the landscape of personal finance in the Golden State by providing predictability to property owners.

How Proposition 13 Limits Tax Increases

Before 1978, property taxes were often volatile, rising sharply as home values increased. Proposition 13 stabilized this by capping the maximum amount of any ad valorem tax on real property at 1% of the full cash value. More importantly, it limited the increase in the assessed value of a property to no more than 2% per year, provided the property does not change ownership or undergo new construction.

From a financial planning perspective, this creates a “locked-in” advantage for long-term owners. A homeowner who purchased a property in the 1990s may pay taxes based on an assessed value far below the current market rate, allowing for significant capital preservation over time.

Base Year Values and Reassessments

The “base year value” is the fulcrum upon which the California tax system balances. When a property is purchased, the sales price typically becomes the new base year value. This value is then adjusted annually by an inflation factor (the California Consumer Price Index), capped at 2%.

A reassessment occurs only upon a “change in ownership” or “completion of new construction.” This means that even if a neighbor’s house doubles in value, your tax bill remains tethered to your original purchase price plus the modest 2% annual adjustment. For investors, this makes California real estate a unique asset class where the tax burden becomes a smaller percentage of the asset’s value the longer it is held.

The Standard 1% Ad Valorem Rate

While the base rate is capped at 1%, the actual “effective” tax rate on a property bill is usually slightly higher. This is because the 1% represents the general levy, but local jurisdictions are permitted to add “voter-approved indebtedness” to the bill. These are typically bonds for schools, parks, or infrastructure. Consequently, most Californians see an effective tax rate ranging from 1.1% to 1.25%, depending on their specific municipality.

Additional Assessments: Mello-Roos and Special Taxes

While Proposition 13 governs the base tax, many modern California developments are subject to additional layers of taxation that can significantly impact a buyer’s monthly carrying costs.

Understanding Mello-Roos Community Facilities Districts

Formally known as the Community Facilities Act of 1982, Mello-Roos allows local governments and school districts to establish Community Facilities Districts (CFDs). These districts can issue bonds to fund public improvements—such as streets, sewers, and police protection—and then levy a special tax on the property owners within that district to repay the debt.

Mello-Roos is most common in newer developments (built after 1980) and can add several thousand dollars to an annual tax bill. Unlike the ad valorem tax, Mello-Roos is not based on the value of the home but rather on formulas like square footage or lot size. For a financial strategist, identifying whether a property is in a Mello-Roos district is vital for determining the true “all-in” cost of ownership.

Direct Levies and Special Assessments

In addition to Mello-Roos, property owners may notice “Direct Levies” on their tax bills. These are non-value-based charges for specific services, such as weed abatement, lighting maintenance, or sewer services. While usually smaller than the base tax, these assessments are mandatory and contribute to the total annual financial obligation.

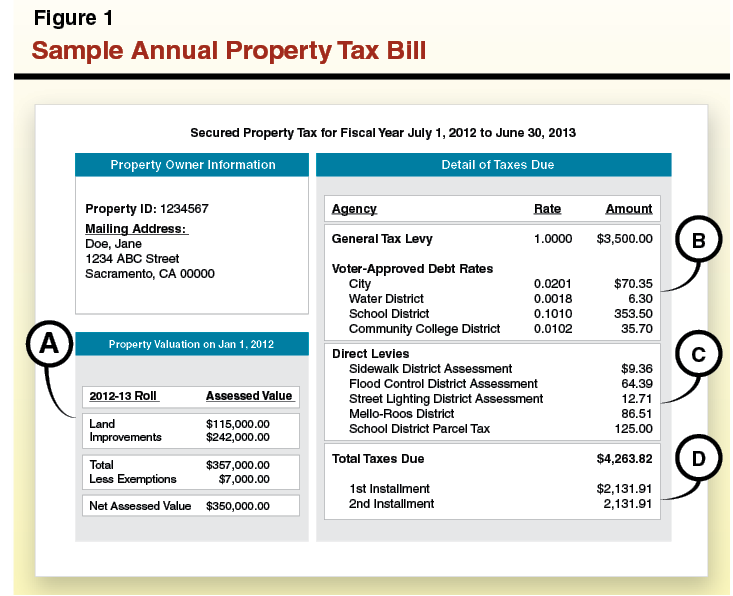

How to Read Your Property Tax Bill

A California property tax bill is divided into several sections. The first section details the assessed value of the land and improvements (the structures). The second section lists the 1% general tax levy. The third section, often the most confusing, lists the various voter-approved bonds and special assessments. Reviewing this document annually is essential to ensure that no errors have occurred in the assessment and that all applicable exemptions have been applied.

Calculating Your Liability: Assessment Timelines and Payments

Effective financial management requires a keen understanding of the California tax calendar. Failing to account for these dates can lead to heavy penalties that erode investment returns.

The Lien Date and Fiscal Year Cycles

In California, the property tax year (fiscal year) runs from July 1st to June 30th of the following year. However, the “lien date”—the date on which the taxes for the upcoming fiscal year become a lien on the property—is January 1st. This timing is crucial for those buying or selling property, as taxes are often prorated in escrow based on these cycles.

Supplemental Tax Bills Explained

One of the most common financial surprises for new California homeowners is the “Supplemental Tax Bill.” When a property is purchased, the County Assessor must reassess the property at its new market value. However, the regular tax bill is often already in the system based on the previous owner’s lower value.

The Supplemental Bill covers the difference between the old tax rate and the new tax rate for the remainder of the fiscal year. Because these bills are mailed separately and are not always paid by a mortgage lender’s impound account, homeowners must set aside additional liquid capital to cover these one-time costs.

Important Deadlines: December and April

California property taxes are paid in two installments. An easy mnemonic used by professionals is “No Darn Fooling Around” (NDFA):

- November 1st: First installment is due.

- December 10th: First installment becomes delinquent after 5:00 PM.

- February 1st: Second installment is due.

- April 10th: Second installment becomes delinquent after 5:00 PM.

Missing these deadlines results in an immediate 10% penalty, a significant financial blow that can be easily avoided through automated payments or careful budgeting.

Exemptions, Exclusions, and Savings Strategies

To optimize a financial position, property owners should leverage every available legal mechanism to reduce their taxable basis or postpone payments.

The Homeowners’ Exemption

California offers a modest “Homeowners’ Exemption” for those who occupy a property as their principal residence. This exemption reduces the assessed value by $7,000, resulting in a modest savings of approximately $70 to $80 per year. While the amount is small, it is a permanent reduction that requires only a one-time filing.

Parent-to-Child and Grandparent-to-Grandchild Transfers (Prop 19)

The rules regarding the transfer of property between generations were significantly altered by Proposition 19, which took effect in 2021. Previously, parents could transfer a primary residence and up to $1 million of other property to their children without a tax reassessment.

Under current law, the “Intergenerational Transfer Exclusion” is much more restrictive. For the tax basis to remain stable, the property must be the principal residence of the transferor and become the principal residence of the transferee within one year. Additionally, there is a cap on the amount of value that can be excluded from reassessment. Navigating Prop 19 requires sophisticated estate planning to ensure that a family’s real estate wealth is not diminished by a massive tax hike upon inheritance.

Property Tax Postponement for Seniors and Disabled Citizens

The State Controller’s Office offers a Property Tax Postponement (PTP) Program. This allows seniors (62+), the blind, or disabled individuals with a limited income to defer payment of property taxes on their primary residence. The deferred taxes become a lien on the property and are repaid when the owner moves, sells the home, or passes away. This is a vital financial tool for retirees who are “house rich but cash poor.”

The Financial Impact of Property Taxes on Real Estate Investment

For the serious investor, property taxes are not just a bill; they are a variable in a complex Return on Investment (ROI) equation.

Incorporating Taxes into ROI Calculations

When analyzing a potential real estate acquisition in California, the “pro forma” tax calculation should always be based on the purchase price, not the current owner’s tax bill. Investors must also account for the 2% annual increase and any local bonds. In high-tax areas with heavy Mello-Roos, the total tax burden can exceed 1.5% of the asset’s value, which can significantly compress cap rates and net cash flow.

The Role of Impound Accounts in Mortgage Planning

Many lenders require “impound” or escrow accounts, where a portion of the monthly mortgage payment is set aside to pay property taxes and insurance. From a cash management perspective, some investors prefer to waive impounds (if the loan-to-value ratio allows) to maintain control over their cash for a longer period, earning interest on those funds before the December and April deadlines. However, this requires disciplined budgeting to ensure the large lump-sum payments are available when due.

Conclusion

California’s property tax system is a double-edged sword. While Proposition 13 provides unparalleled long-term stability and protection against rising market values, the complexity of Mello-Roos, supplemental bills, and the recent changes brought by Proposition 19 require constant vigilance. By viewing property taxes through a financial lens—as a manageable expense that can be optimized through strategic planning—California property owners can better protect their equity and ensure their real estate investments continue to serve their broader financial goals.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.