Navigating the landscape of healthcare in retirement can be one of the most significant financial challenges an individual faces. For millions of Americans, Medicare serves as the cornerstone of their health insurance coverage once they turn 65, or if they have certain disabilities. However, Medicare is not a monolithic entity; it’s a complex system divided into distinct parts, each covering different services and carrying unique financial implications. Understanding “what are Medicare Parts A, B, C, D” is not just about knowing acronyms; it’s about making informed financial decisions that can significantly impact your healthcare costs and access to necessary services throughout your later years.

This comprehensive guide will demystify the various components of Medicare, providing a clear breakdown of what each part covers, its associated costs, and how they collectively shape your healthcare financial strategy. By the end, you’ll have a clearer picture of how to optimize your Medicare choices to align with your personal financial situation and health needs.

Navigating the Fundamentals: Original Medicare (Parts A & B)

At its core, Medicare is structured around two primary components, often referred to as “Original Medicare”: Part A and Part B. These two parts provide essential hospital and medical insurance, laying the foundation for most beneficiaries’ healthcare coverage.

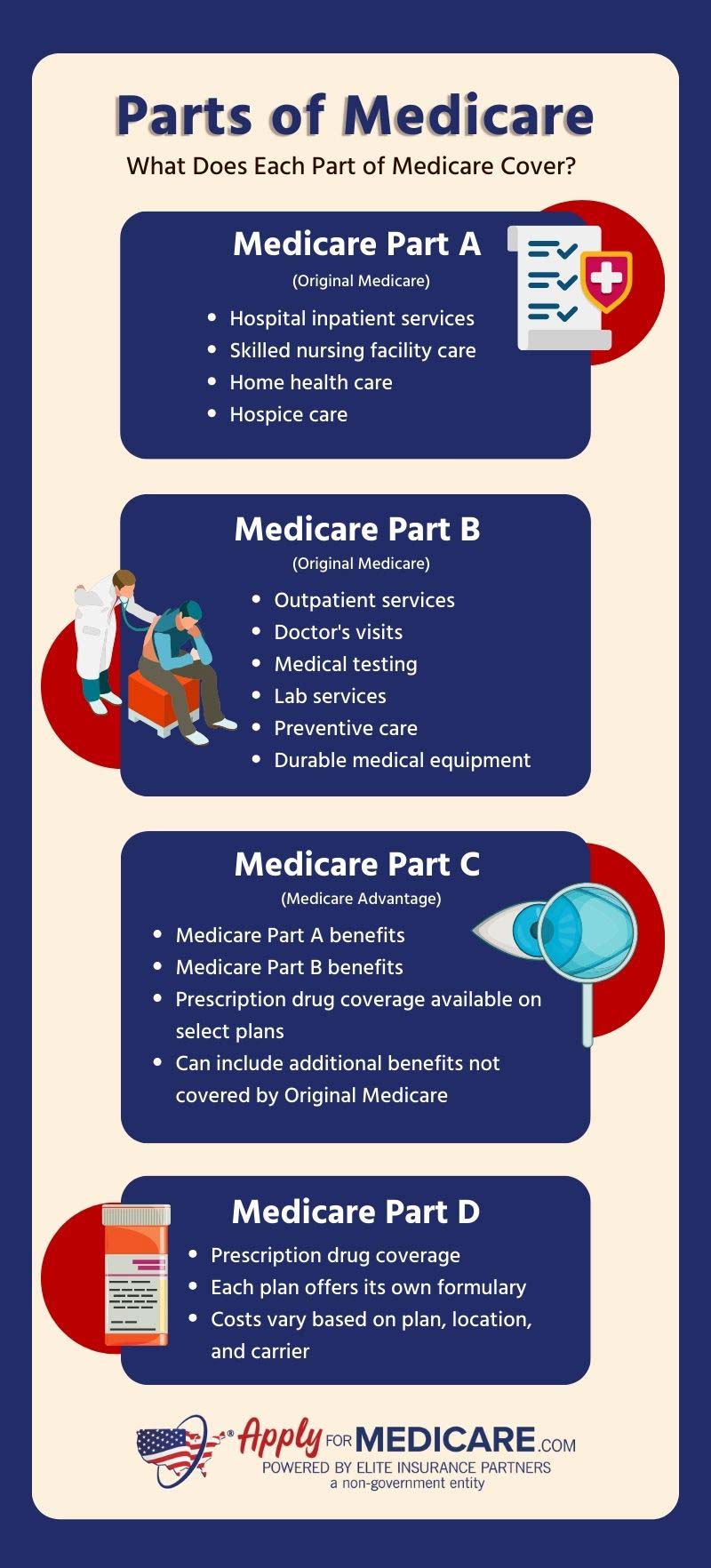

Medicare Part A: Hospital Insurance

Medicare Part A is primarily your hospital insurance. It helps cover the costs associated with inpatient care in hospitals, including semi-private rooms, meals, nursing services, and drugs administered during your stay. Beyond acute hospital care, Part A also extends to other crucial services designed to support recovery and long-term care needs.

-

Coverage Details:

- Inpatient Hospital Stays: Covers care received in a hospital after a formal admission, typically for up to 90 days per benefit period, with additional “lifetime reserve days” available.

- Skilled Nursing Facility (SNF) Care: Covers a limited stay in an SNF if it follows a qualifying hospital stay and you require skilled nursing or therapy services. This is not for long-term custodial care.

- Hospice Care: Provides coverage for terminally ill patients who choose comfort care over curative treatment, including services, medications, and support for family members.

- Some Home Health Care: Covers medically necessary skilled nursing care, physical therapy, occupational therapy, and speech-language pathology services provided in your home.

-

Cost Implications:

For most individuals, Medicare Part A is premium-free. This applies if you or your spouse paid Medicare taxes for at least 10 years (40 quarters) while working. If you don’t meet this threshold, you may have to pay a monthly premium, which can be substantial. Even if premium-free, Part A involves a deductible for each benefit period (which restarts after 60 days out of a hospital or SNF). Coinsurance applies for extended hospital or SNF stays. Understanding these costs is crucial for budgeting, as a single hospital stay can incur significant out-of-pocket expenses if you don’t have supplemental coverage.

Medicare Part B: Medical Insurance

Medicare Part B is your medical insurance, covering a broader range of outpatient services, doctor’s visits, and preventive care that Part A does not. It’s often the most frequently used part of Medicare for routine healthcare needs.

-

Coverage Details:

- Doctor’s Visits: Covers medically necessary services from doctors and other healthcare providers, including specialists, for diagnosing and treating health conditions.

- Outpatient Care: Includes services received in hospital outpatient departments, clinics, emergency rooms (if not admitted), and ambulatory surgical centers.

- Preventive Services: Covers a wide array of preventive care, such as flu shots, various screenings (e.g., for cancer, diabetes), and annual wellness visits, often with no cost-sharing.

- Durable Medical Equipment (DME): Covers equipment prescribed by a doctor for use in the home, such as wheelchairs, walkers, oxygen equipment, and hospital beds.

- Other Services: Includes certain ambulance services, mental health services, lab tests, X-rays, and some home health services not covered by Part A.

-

Cost Implications:

Unlike Part A, Medicare Part B typically comes with a standard monthly premium, which is deducted directly from your Social Security benefit. This premium can be higher for individuals with higher incomes (Income-Related Monthly Adjustment Amount, or IRMAA). In addition to the premium, Part B has an annual deductible. After meeting the deductible, you typically pay 20% of the Medicare-approved amount for most services, with no annual out-of-pocket maximum. This 20% coinsurance for unlimited services can pose a significant financial risk, highlighting the need for careful financial planning or additional coverage.

The Gaps in Original Medicare

While Parts A and B provide fundamental coverage, they are not exhaustive. Original Medicare does not cover everything, leaving several significant “gaps” that beneficiaries must address to avoid potentially crippling out-of-pocket costs. These gaps include:

- No Out-of-Pocket Maximum: As mentioned, there’s no limit to what you could pay in coinsurance for Part B services.

- Prescription Drugs: Original Medicare generally does not cover outpatient prescription drugs.

- Routine Vision, Dental, and Hearing Care: Standard eye exams, eyeglasses, dental cleanings, dentures, and hearing aids are typically not covered.

- Long-Term Custodial Care: Services like help with bathing, dressing, and eating, whether at home or in a facility, are generally not covered.

Recognizing these gaps is the first step in understanding why many beneficiaries opt for additional Medicare coverage, leading us to Parts C and D.

Expanding Your Options: Medicare Part C (Medicare Advantage)

For those seeking a more integrated and potentially broader scope of benefits beyond Original Medicare, Part C, known as Medicare Advantage, offers an alternative pathway. These plans are offered by private insurance companies approved by Medicare, providing a “one-stop shop” for many beneficiaries.

Understanding Medicare Advantage Plans

Medicare Advantage plans essentially bundle your Part A, Part B, and often Part D benefits into a single plan. They must cover all the services that Original Medicare covers, but they can (and typically do) offer additional benefits.

- How It Works: Instead of Medicare paying directly for your services, Medicare pays a fixed amount each month to the private insurance company providing your Medicare Advantage plan. You then receive your benefits through that private plan.

- Bundled Benefits: Most Medicare Advantage plans include prescription drug coverage (Part D) and often offer extra benefits not covered by Original Medicare, such as routine vision, dental, and hearing care, gym memberships, and even transportation to doctor appointments. Some plans also offer telehealth services and over-the-counter allowances.

Key Considerations for Part C

Choosing a Medicare Advantage plan involves weighing various factors, especially concerning access to care and cost predictability.

- Network Restrictions: Many Medicare Advantage plans are Health Maintenance Organizations (HMOs) or Preferred Provider Organizations (PPOs), which means you may need to use doctors and hospitals within the plan’s network to receive the lowest costs. HMOs typically require a referral from a primary care doctor to see a specialist.

- Cost Structure: While many Medicare Advantage plans have low or even $0 monthly premiums (beyond your Part B premium), they come with their own deductibles, copayments, and coinsurance for various services. However, a significant advantage is that all Medicare Advantage plans have an annual out-of-pocket maximum. Once you reach this limit, the plan pays 100% of your covered services for the rest of the year, providing a crucial financial safety net not found in Original Medicare.

- Advantages and Disadvantages:

- Advantages: Often lower monthly premiums, bundled benefits (including Part D and extras), and an out-of-pocket maximum.

- Disadvantages: May have network restrictions, require referrals, and choices can be limited by your geographic area.

Essential Prescription Drug Coverage: Medicare Part D

For those sticking with Original Medicare (Parts A & B) or supplementing it with a Medigap policy, Medicare Part D becomes an indispensable component of their financial healthcare strategy. Part D provides crucial coverage for outpatient prescription drugs, a cost area that can quickly escalate without proper planning.

The Role of Part D Plans

Medicare Part D plans are offered by private insurance companies approved by Medicare. You can get Part D in two ways: as a standalone Prescription Drug Plan (PDP) if you have Original Medicare, or as part of a Medicare Advantage Plan (MAPD).

- How It Works: These plans help cover the cost of prescription drugs. Each plan has a formulary, which is a list of drugs it covers, organized into tiers with different cost-sharing levels.

- Coverage Stages: Part D plans typically involve several coverage stages, which can impact your out-of-pocket costs throughout the year:

- Deductible: An initial amount you pay out-of-pocket before your plan starts to pay.

- Initial Coverage Limit: Once you meet your deductible, you and your plan share costs for covered drugs until you reach this limit.

- Coverage Gap (Donut Hole): Historically a significant concern, the coverage gap meant you paid a higher percentage for your drugs once your total drug costs (what you and your plan have paid) reached a certain threshold. Thanks to the Affordable Care Act, beneficiaries now pay no more than 25% for brand-name and generic drugs while in the donut hole.

- Catastrophic Coverage: After your out-of-pocket costs (including deductible, copayments, and the discounted amount you pay in the donut hole) reach a certain limit, you enter catastrophic coverage, where you pay a very small coinsurance or copayment for your drugs for the rest of the year.

Choosing the Right Part D Plan

Selecting a Part D plan requires careful consideration, as the “best” plan is highly individualized based on your specific medication needs.

- Formularies: Ensure your current and anticipated medications are covered by the plan’s formulary. Check for any restrictions, such as prior authorization or step therapy.

- Premiums, Deductibles, Copayments: Compare the monthly premiums, the plan’s deductible, and the copayments/coinsurance for your specific drugs across different tiers.

- Importance of Comparing Plans Annually: Drug costs, plan formularies, and premiums can change year to year. It is highly recommended to review and compare Part D plans during the Annual Enrollment Period (October 15 – December 7) to ensure your plan still offers the most cost-effective coverage for your needs.

Making Informed Financial Decisions: Beyond the ABCDs

Understanding Parts A, B, C, and D is foundational, but effective Medicare financial planning extends beyond these basic definitions. It involves considering supplemental options, understanding enrollment timelines, and integrating healthcare costs into your broader retirement financial strategy.

Medicare Supplement Insurance (Medigap)

For those with Original Medicare (Parts A & B), Medicare Supplement Insurance, commonly known as Medigap, is a critical tool for managing out-of-pocket expenses. Medigap policies are sold by private companies and help cover some of the “gaps” in Original Medicare.

- What it Covers: Medigap policies help pay for costs like Part A and B deductibles, copayments, and coinsurance, including the 20% coinsurance for Part B services that has no annual limit. Some plans also cover emergency healthcare costs when traveling outside the U.S.

- Why it’s Important for Financial Predictability: By covering many of the costs not paid by Original Medicare, Medigap policies offer greater financial predictability and peace of mind. They significantly reduce the risk of unexpected, high healthcare bills.

- How it Differs from Medicare Advantage: It’s crucial to understand that you cannot have a Medigap policy if you are enrolled in a Medicare Advantage Plan. Medigap policies work with Original Medicare, not as an alternative to it. If you have a Medigap policy, your Medigap insurance will pay its share after Medicare pays its share of your bill.

Enrollment Periods and Penalties

Timing is everything when it comes to Medicare enrollment. Missing key deadlines can result in permanent late enrollment penalties, significantly increasing your monthly premiums for the rest of your life.

- Initial Enrollment Period (IEP): A 7-month window surrounding your 65th birthday – it starts three months before your birth month, includes your birth month, and continues for three months after. This is when most people first enroll in Medicare Parts A and B, and often Part D.

- General Enrollment Period (GEP): If you miss your IEP and aren’t eligible for a Special Enrollment Period, you can enroll in Parts A and/or B during the GEP (January 1 to March 31 each year), with coverage starting July 1. However, late enrollment penalties may apply.

- Special Enrollment Periods (SEPs): Available for individuals who delay enrollment due to specific life events, such as being covered by group health insurance through current employment. These allow you to enroll without penalty outside of the standard periods.

- Late Enrollment Penalties:

- Part B: If you don’t sign up for Part B when you’re first eligible and don’t qualify for an SEP, your monthly premium may increase by 10% for each full 12-month period you could have had Part B but didn’t. This penalty is generally permanent.

- Part D: If you don’t join a Medicare drug plan when you first become eligible and don’t have other credible prescription drug coverage (e.g., from an employer), you may pay a late enrollment penalty that is added to your monthly premium for as long as you have Part D.

The Financial Impact and Long-Term Planning

Medicare is an indispensable part of retirement planning, but it’s not a complete solution. Healthcare costs in retirement are a major concern for many, and understanding Medicare is the first step toward managing them effectively.

- Budgeting for Healthcare Costs in Retirement: Even with Medicare, out-of-pocket expenses for premiums, deductibles, copayments, and services not covered can be substantial. It’s essential to factor these costs into your retirement budget, allocating funds specifically for healthcare.

- Considering Future Health Needs and Rising Costs: Healthcare costs tend to rise over time, and your health needs may increase with age. When making Medicare decisions, consider your long-term health outlook and how your chosen coverage will adapt to evolving needs and costs.

- The Importance of Professional Financial Advice: Given the complexity of Medicare and its profound impact on personal finances, consulting with a qualified financial advisor or a Medicare specialist can be invaluable. They can help you navigate the myriad options, understand the fine print, and make choices that align best with your unique financial situation and health goals.

In conclusion, Medicare Parts A, B, C, and D are more than just insurance components; they are crucial elements of your financial well-being in retirement. By understanding their nuances, making timely enrollment decisions, and strategically choosing supplemental coverage, you can effectively manage healthcare costs and secure access to the care you need, fostering a more financially secure and healthier future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.