In the intricate world of personal and business finance, few concepts hold as much significance and potential impact as loan interest rates. Far from being a mere numerical figure, an interest rate is the bedrock upon which the entire lending ecosystem is built, determining the true cost of borrowing and shaping the financial decisions of individuals, businesses, and even governments. Understanding what loan interest rates are, how they are determined, and their various forms is not just a matter of financial literacy; it is a critical skill for anyone looking to borrow money, manage debt, or invest wisely.

At its core, a loan interest rate is the percentage charged by a lender to a borrower for the use of assets, typically expressed as an annual percentage of the outstanding loan amount. It is essentially the “price” you pay to borrow money, compensating the lender for the risk they take in extending credit, the opportunity cost of not using their funds elsewhere, and the erosion of purchasing power due to inflation over time. For borrowers, this rate directly influences the total amount they will repay over the life of the loan, dictating the affordability of a mortgage, a car loan, or a business expansion. For lenders, it represents their primary source of revenue. Delving into the nuances of loan interest rates provides a foundational understanding of debt, investment, and the broader economic landscape.

The Fundamental Concept of Loan Interest Rates

To navigate the financial world effectively, one must first grasp the foundational principles behind loan interest rates. It’s more than just a number; it’s an economic mechanism that balances the needs of borrowers with the risks and rewards sought by lenders.

Defining Interest: The Cost of Borrowing

Interest, in its simplest form, is the charge for the privilege of borrowing money. When you take out a loan, whether it’s for a new home, a car, education, or to fund a business venture, you are essentially renting money from a financial institution or individual. The interest rate is the rental fee, typically expressed as a percentage of the principal (the original amount borrowed). This percentage is usually an annual rate, known as the Annual Percentage Rate (APR), though it can be broken down into monthly or daily rates for calculation purposes.

This cost isn’t arbitrary. It serves multiple purposes for the lender:

- Compensation for Risk: Lenders face the risk that a borrower might default on their payments. Higher-risk borrowers often face higher interest rates to compensate the lender for this increased probability of loss.

- Time Value of Money: A dollar today is worth more than a dollar tomorrow due to inflation and potential investment opportunities. Interest accounts for this lost opportunity cost for the lender.

- Operational Costs: Lenders incur expenses in originating, servicing, and collecting loans. A portion of the interest rate covers these administrative and operational overheads.

- Profit Margin: Like any business, financial institutions aim to make a profit. Interest rates are structured to ensure profitability after covering risks and costs.

Understanding interest as the explicit cost of accessing capital is the first step toward making informed financial decisions. It transforms a seemingly simple transaction into a sophisticated economic exchange.

Why Interest Rates Matter to Borrowers and Lenders

The significance of interest rates extends far beyond mere calculation; they are a critical determinant of financial health for both parties involved in a lending agreement.

For borrowers, interest rates directly impact:

- Affordability: A lower interest rate means lower monthly payments and a reduced total cost of borrowing, making loans more accessible and sustainable. Conversely, high rates can make essential purchases, like homes or cars, prohibitively expensive.

- Debt Burden: Over the lifetime of a loan, particularly long-term ones like mortgages, even a small difference in the interest rate can amount to tens of thousands of dollars in extra payments. This directly affects an individual’s or business’s disposable income and financial flexibility.

- Financial Planning: Interest rates influence decisions on when to borrow, how much to borrow, and whether to opt for fixed versus variable rate loans, impacting long-term financial strategies.

For lenders, interest rates are equally crucial:

- Profitability: They are the primary revenue stream. Setting competitive yet profitable rates is essential for financial institutions to thrive.

- Risk Management: Lenders use interest rates as a tool to manage credit risk. They can offer lower rates to highly creditworthy borrowers and higher rates to those deemed riskier, balancing their portfolio.

- Market Position: Offering attractive interest rates can help lenders attract more customers and gain market share, while uncompetitive rates can lead to a loss of business.

- Economic Impact: The collective lending decisions of financial institutions, driven by prevailing interest rates, can significantly influence economic activity, stimulating or dampening spending and investment.

The interplay between these factors highlights that interest rates are not static or arbitrary; they are dynamic economic indicators reflecting underlying market conditions, individual creditworthiness, and strategic financial objectives.

Key Factors That Influence Loan Interest Rates

The interest rate you are offered on a loan is not pulled from thin air. It is the result of a complex interplay of various factors, some specific to you as a borrower, others related to the loan itself, and still others reflecting the broader economic environment. Understanding these influences can empower you to secure more favorable lending terms.

Borrower-Specific Factors: Credit Score and Debt-to-Income Ratio

Your personal financial profile plays a pivotal role in determining the interest rate you qualify for. Lenders assess your ability and willingness to repay debt.

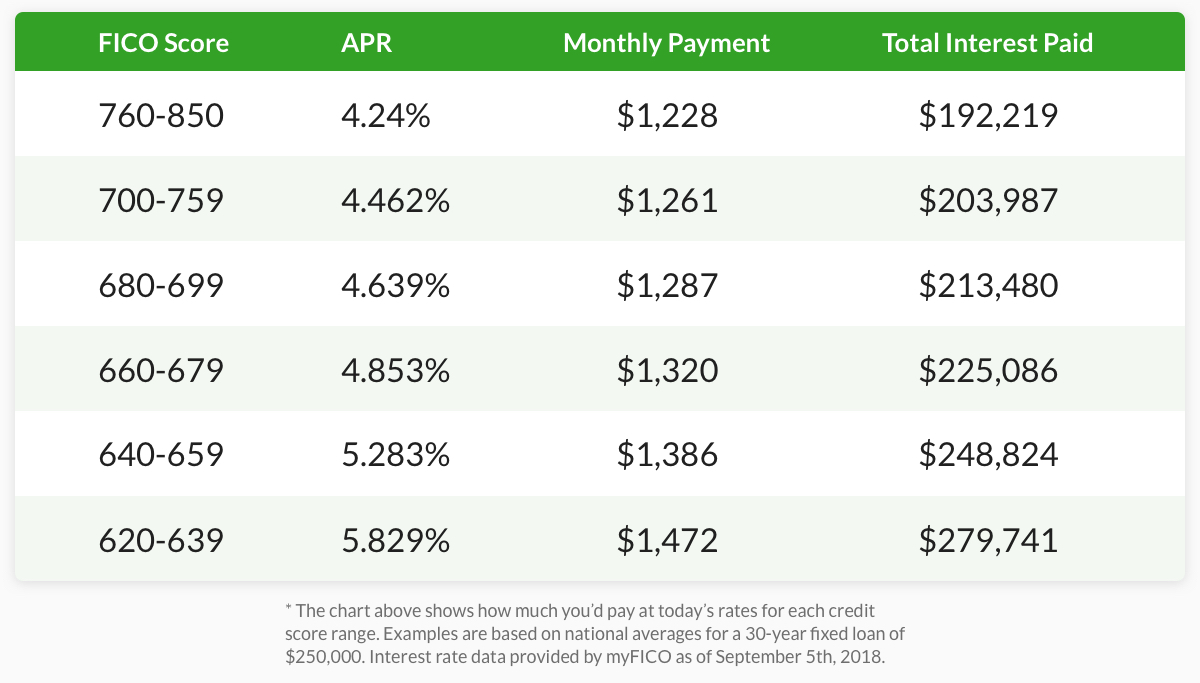

- Credit Score: This three-digit number (e.g., FICO or VantageScore) is arguably the most significant factor. It’s a numerical representation of your creditworthiness, derived from your credit history, including payment punctuality, total debt, length of credit history, and types of credit used. A higher credit score (typically above 720) indicates a lower risk to lenders, often translating into significantly lower interest rates. Conversely, a poor credit score suggests a higher risk of default, leading to higher rates or even loan rejection.

- Debt-to-Income (DTI) Ratio: This ratio compares your total monthly debt payments to your gross monthly income. A low DTI ratio signals that you have sufficient income to manage additional debt, making you a less risky borrower. Lenders typically prefer DTI ratios below 36%, though some may approve loans for higher ratios, often with less favorable terms.

- Employment Stability and Income: Lenders prefer borrowers with stable employment and a consistent income stream, as this indicates a reliable source of funds for repayment.

Loan-Specific Factors: Type of Loan, Term Length, and Collateral

Beyond your personal profile, the characteristics of the loan itself heavily influence the interest rate.

- Type of Loan: Different loan products inherently carry different levels of risk and thus different interest rates.

- Secured Loans (e.g., mortgages, auto loans): These loans are backed by collateral (an asset like a house or car) that the lender can seize if you default. The presence of collateral reduces the lender’s risk, resulting in lower interest rates.

- Unsecured Loans (e.g., personal loans, credit cards, student loans): These are not backed by collateral and are therefore riskier for lenders. As a result, they typically come with higher interest rates.

- Business Loans: Rates can vary widely based on the business’s revenue, age, industry, and the purpose of the loan.

- Loan Term Length: The duration over which you agree to repay the loan also affects the rate.

- Shorter-term loans generally carry lower interest rates because the lender’s money is tied up for a shorter period, reducing exposure to inflation and market fluctuations.

- Longer-term loans typically have higher interest rates to compensate the lender for the increased risk over a prolonged period and the greater impact of inflation on the value of future payments.

- Loan Amount: While not always a direct inverse relationship, very small loans or very large loans might have slightly different rate structures due to administrative costs or the scale of risk.

- Loan Purpose: The intended use of the funds can also subtly influence rates, particularly for specialized loans (e.g., specific student loan programs might have government-subsidized rates).

Economic & Market Factors: Central Bank Policies and Inflation

The broader economic environment casts a long shadow over interest rates, affecting all borrowers and lenders.

- Central Bank Policies (e.g., Federal Reserve in the US, ECB in Europe): Central banks set benchmark interest rates (like the federal funds rate in the US) that influence all other interest rates in the economy. When the central bank raises rates to combat inflation, commercial banks’ borrowing costs increase, and they, in turn, pass these higher costs on to consumers and businesses. Conversely, lowering rates can stimulate economic activity by making borrowing cheaper.

- Inflation: Inflation erodes the purchasing power of money over time. Lenders incorporate an inflation premium into interest rates to ensure that the money they are repaid in the future has roughly the same purchasing power as the money they lent out today. Higher expected inflation typically leads to higher interest rates.

- Economic Outlook: A strong economy with low unemployment and high consumer confidence might lead to slightly higher rates as demand for credit increases. Conversely, during economic downturns, central banks may lower rates to encourage borrowing and investment.

- Market Demand and Supply for Credit: If there’s high demand for loans but limited funds available from lenders, interest rates tend to rise. If there’s ample supply of funds and low demand, rates may fall.

- Lender-Specific Policies and Competition: Individual lenders also have their own internal risk assessment models, profit targets, and competitive strategies, which can lead to variations in rates offered for similar borrowers and loan types. Shopping around is crucial because different lenders will weigh these factors differently.

By understanding this complex tapestry of influencing factors, borrowers can proactively work to improve their financial standing and position themselves for the most favorable loan terms available.

Understanding Different Types of Loan Interest Rates

While the overarching concept of an interest rate remains consistent, its application and structure can vary significantly, leading to different types of rates that cater to diverse financial needs and risk appetites. The primary distinction lies between fixed and variable rates, each with its own set of advantages and disadvantages.

Fixed-Rate Loans: Stability and Predictability

A fixed-rate loan is characterized by an interest rate that remains constant throughout the entire term of the loan. This means your monthly principal and interest payments will stay the same from the first payment to the last, irrespective of market fluctuations.

- Advantages:

- Predictability: Borrowers know exactly what their payments will be, making budgeting and long-term financial planning much simpler.

- Protection from Rising Rates: If market interest rates increase, your fixed rate remains unchanged, saving you money compared to a variable-rate loan.

- Peace of Mind: The certainty of payments can reduce financial stress, especially for large, long-term commitments like mortgages.

- Disadvantages:

- Higher Initial Rates: Fixed rates are often slightly higher than initial variable rates because the lender takes on the risk of future interest rate increases.

- Missed Opportunity for Falling Rates: If market interest rates fall, you won’t benefit from the decrease unless you refinance your loan, which comes with its own costs.

- Less Flexible: Generally, fixed-rate loans offer less flexibility in terms of early repayment penalties, though this varies by lender and loan type.

Fixed-rate loans are particularly popular for mortgages, student loans, and some personal loans, where borrowers prioritize stability and predictable monthly expenses over the life of the debt.

Variable-Rate Loans: Flexibility and Potential Risk

Also known as adjustable-rate loans (ARMs for mortgages), variable-rate loans feature an interest rate that can change over the loan’s term. These rates are typically tied to a benchmark index (such as the prime rate, LIBOR, or SOFR) plus a margin set by the lender. As the benchmark index fluctuates, so does your interest rate and, consequently, your monthly payments.

- Advantages:

- Lower Initial Rates: Variable rates often start lower than fixed rates, making them attractive for borrowers seeking reduced initial payments or those who expect to pay off the loan quickly.

- Benefit from Falling Rates: If market interest rates decline, your loan payments will also decrease, saving you money.

- Flexibility: Some variable-rate products offer more flexibility for prepayment without penalties.

- Disadvantages:

- Payment Volatility: The biggest drawback is the uncertainty. Payments can increase significantly if market rates rise, potentially straining your budget.

- Budgeting Difficulty: Unpredictable payments make long-term financial planning challenging.

- Caps and Floors: While most variable-rate loans have caps (maximum interest rate) and floors (minimum interest rate) to limit volatility, rates can still rise substantially over time.

Variable-rate loans are common for mortgages (especially ARMs), some business lines of credit, and certain personal loans. They appeal to borrowers who are comfortable with risk, have a strong cash flow buffer, or anticipate declining interest rates.

APR vs. Interest Rate: The True Cost of Borrowing

It’s crucial to distinguish between a quoted interest rate and the Annual Percentage Rate (APR). While the interest rate is the percentage you pay on the principal, the APR represents the total annual cost of borrowing, including the interest rate plus any additional fees, charges, or discount points associated with the loan.

- Interest Rate: This is the base rate charged for the use of the principal amount. It’s the numerical percentage (e.g., 5%) that you apply to the loan balance to calculate the interest portion of your payment.

- APR (Annual Percentage Rate): The APR provides a more comprehensive picture of a loan’s cost. It’s a standardized way to compare loan offers from different lenders because it encapsulates not just the interest but also other mandatory costs like origination fees, closing costs, mortgage insurance, and other charges that the borrower must pay to get the loan. For example, a loan might have an interest rate of 4.5% but an APR of 4.8% due to associated fees.

Why is this distinction important? When comparing loan offers, always look at the APR, not just the interest rate. A loan with a slightly lower interest rate but high fees might end up being more expensive than a loan with a slightly higher interest rate but no fees. The APR allows for an apples-to-apples comparison of the true cost of borrowing across different lenders. This transparency is particularly valuable for complex loans like mortgages, where various fees can significantly impact the overall expense.

Calculating and Managing Your Loan Interest

Understanding how interest is calculated and implementing effective strategies to manage it can significantly impact your financial well-being. The seemingly complex world of loan interest becomes manageable once you grasp the underlying mechanics and available tools.

How Loan Interest Is Calculated: Simple vs. Compound Interest

The method of calculating interest fundamentally impacts the total amount you repay. There are two primary types:

-

Simple Interest: This is the easiest to understand. Simple interest is calculated only on the principal amount of a loan or deposit. It does not compound.

- Formula:

Simple Interest = Principal × Interest Rate × Time - Example: A $10,000 loan at 5% simple interest for 3 years would accrue $500 in interest per year ($10,000 * 0.05), totaling $1,500 over three years. Your payment breakdown would reflect this consistent interest charge.

- Use: Simple interest is common for short-term loans, some specific types of car loans, and sometimes for peer-to-peer lending.

- Formula:

-

Compound Interest: This is far more common for most consumer loans, including mortgages, credit cards, and many personal loans. Compound interest is calculated on the initial principal and also on the accumulated interest from previous periods. In essence, you earn (or pay) interest on interest.

- Example: If you have a $10,000 loan at 5% annual interest compounded annually, in year one you’d owe $500 in interest. In year two, the interest would be calculated on $10,500, not just the original $10,000. This snowball effect can dramatically increase the total amount paid over time, especially for long-term loans.

- Frequency of Compounding: Interest can be compounded annually, semi-annually, quarterly, monthly, or even daily. The more frequently interest is compounded, the faster your debt (or savings) grows. For loans, monthly compounding is typical.

- Amortization: For most installment loans (like mortgages and car loans), compound interest is applied through an amortization schedule. Early payments are heavily weighted toward interest, with a smaller portion going to the principal. As the principal decreases, the interest portion of each payment also decreases, and more goes towards the principal.

Understanding whether a loan uses simple or compound interest and its compounding frequency is vital for accurately assessing the true cost of borrowing.

Strategies to Secure Favorable Interest Rates

Proactive measures can significantly improve your chances of obtaining lower interest rates.

- Improve Your Credit Score: This is paramount. Pay bills on time, keep credit utilization low (below 30%), avoid opening too many new credit accounts at once, and regularly check your credit report for errors. A strong credit score signals reliability to lenders.

- Reduce Your Debt-to-Income Ratio: Before applying for a new loan, focus on paying down existing debts. A lower DTI ratio demonstrates that you can comfortably manage additional payments.

- Save for a Larger Down Payment: For secured loans like mortgages or auto loans, a larger down payment reduces the amount you need to borrow, thereby lowering the lender’s risk and potentially earning you a lower interest rate. It also signals your commitment.

- Shorten the Loan Term: If feasible for your budget, opt for a shorter repayment period. Lenders often offer lower rates on shorter-term loans because their risk exposure to market fluctuations and inflation is reduced.

- Provide Collateral (for secured loans): If appropriate for your financial situation, using an asset as collateral can significantly lower the interest rate on a loan, as it mitigates risk for the lender.

- Negotiate: Don’t be afraid to negotiate, especially if you have an excellent credit score or offers from multiple lenders. Lenders want your business and may be willing to match or beat a competitor’s rate.

The Long-Term Impact of Interest on Repayment

The impact of interest rates is magnified over the life of a loan. A seemingly small difference in the interest rate can translate into thousands, if not tens of thousands, of dollars saved or spent over decades.

- Total Cost of Loan: The cumulative interest paid can easily exceed the original principal amount, especially for long-term loans like 30-year mortgages. For example, a $300,000 mortgage at 4% interest over 30 years results in approximately $215,600 in interest paid, while at 5%, it jumps to around $279,000 – a difference of over $63,000.

- Monthly Payments: Higher interest rates lead to higher monthly payments, reducing your disposable income and potentially limiting your ability to save or invest.

- Financial Flexibility: Lower interest rates free up cash flow, providing greater flexibility in your budget, allowing you to pay down other debts, build an emergency fund, or invest for the future.

- Wealth Accumulation vs. Debt Accumulation: Understanding interest is critical for both borrowers and savers. While compound interest works against you when borrowing, it works for you when saving or investing. Managing interest effectively means minimizing its negative impact on your debts while maximizing its positive impact on your investments.

Proactively managing your interest rates through these strategies is a cornerstone of sound financial planning, enabling you to reduce your overall debt burden and achieve your financial goals more efficiently.

Navigating the Loan Landscape: Informed Borrowing Decisions

The world of lending can appear daunting, but armed with a thorough understanding of loan interest rates and their intricacies, you are well-equipped to make informed decisions that serve your financial best interests. The key lies in diligent research, comparison, and strategic action.

The Importance of Shopping Around and Comparing Offers

Perhaps the most critical step in securing a favorable loan is the act of shopping around. Just as you wouldn’t buy the first car or house you see, you shouldn’t accept the first loan offer that comes your way. Different lenders—banks, credit unions, online lenders, and even peer-to-peer platforms—have varying overheads, risk assessment models, and profit targets, leading to a wide range of interest rates and terms for the same borrower.

- Get Multiple Quotes: Apply for pre-qualification or full loan applications with at least 3-5 different lenders. This allows you to receive concrete offers based on your specific financial profile.

- Compare APRs, Not Just Interest Rates: As discussed, the APR provides the true total annual cost of borrowing. A lower interest rate might look appealing, but if it comes with high origination fees or other charges, its APR could be higher than a competitor’s offer.

- Scrutinize All Terms and Conditions: Beyond the interest rate and APR, carefully review loan terms, including:

- Repayment Schedule: How long is the loan term? Are payments fixed or variable?

- Prepayment Penalties: Will you be charged a fee if you pay off the loan early?

- Late Payment Fees: What are the penalties for missed or late payments?

- Escrow Requirements: For mortgages, are property taxes and insurance included in your monthly payment?

- Refinancing Options: What are the lender’s policies should you wish to refinance in the future?

- Leverage Competition: If you receive a better offer from one lender, don’t hesitate to ask another lender to match or beat it. Many financial institutions are willing to compete for good borrowers.

Taking the time to compare offers thoroughly can save you thousands of dollars over the life of a loan and ensure that you secure the most competitive terms available.

When to Consider Refinancing for Better Rates

Refinancing involves taking out a new loan to pay off an existing one, typically with the goal of securing more favorable terms. This strategy can be a powerful tool for managing your debt, especially when market conditions change or your financial situation improves.

- Falling Interest Rates: The most common reason to refinance is when prevailing market interest rates have dropped significantly since you took out your original loan. Even a small reduction in rate can lead to substantial savings, especially on large, long-term debts like mortgages.

- Improved Credit Score: If your credit score has significantly improved since you initially obtained your loan, you may now qualify for much better rates. Lenders will view you as a lower risk, making refinancing an attractive option.

- Switching from Variable to Fixed-Rate: If you have a variable-rate loan and anticipate interest rates rising, refinancing into a fixed-rate loan can provide stability and predictability for your future payments. Conversely, if rates are falling and you can tolerate more risk, refinancing from a high fixed-rate to a lower variable-rate might be considered, though this is less common.

- Shortening the Loan Term: Refinancing to a shorter term (e.g., from a 30-year to a 15-year mortgage) can save you a significant amount in total interest, even if the monthly payments increase slightly.

- Consolidating Debt: Refinancing can also be used to consolidate multiple high-interest debts (like credit card balances) into a single loan with a lower interest rate, simplifying payments and reducing overall interest costs.

However, refinancing isn’t always the right choice. It comes with its own costs, such as origination fees, closing costs, and appraisal fees. You must carefully weigh the potential savings against these upfront costs. A general rule of thumb for mortgages is that it’s often worthwhile if you can reduce your interest rate by at least 0.75% to 1.00% and plan to stay in the home long enough to recoup the refinancing costs. Always perform a break-even analysis to determine how long it will take for the savings to outweigh the costs.

In conclusion, loan interest rates are a cornerstone of the financial landscape, impacting every borrowing decision you make. By understanding what they are, the forces that shape them, the different forms they take, and how to effectively calculate and manage them, you transform from a passive borrower into an empowered financial decision-maker. Diligent research, strategic planning, and a commitment to improving your financial health are the keys to unlocking the most favorable loan terms and optimizing your financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.