The question “what are house interest rates today?” is perhaps the most frequent query in the world of personal finance and real estate. For potential homeowners, investors, and even those looking to refinance, the answer dictates much more than a monthly payment; it determines long-term wealth accumulation, purchasing power, and the overall feasibility of a property investment. In recent years, the mortgage market has transitioned from a period of historic lows to a more volatile and elevated environment, leaving many wondering how to navigate the current financial terrain.

Understanding mortgage rates requires looking beyond a single percentage point. It involves analyzing the intersection of macroeconomic policy, individual financial health, and the broader trends of the global economy. This guide provides an in-depth exploration of the factors driving today’s house interest rates and the strategies you can use to secure the best possible terms for your financial future.

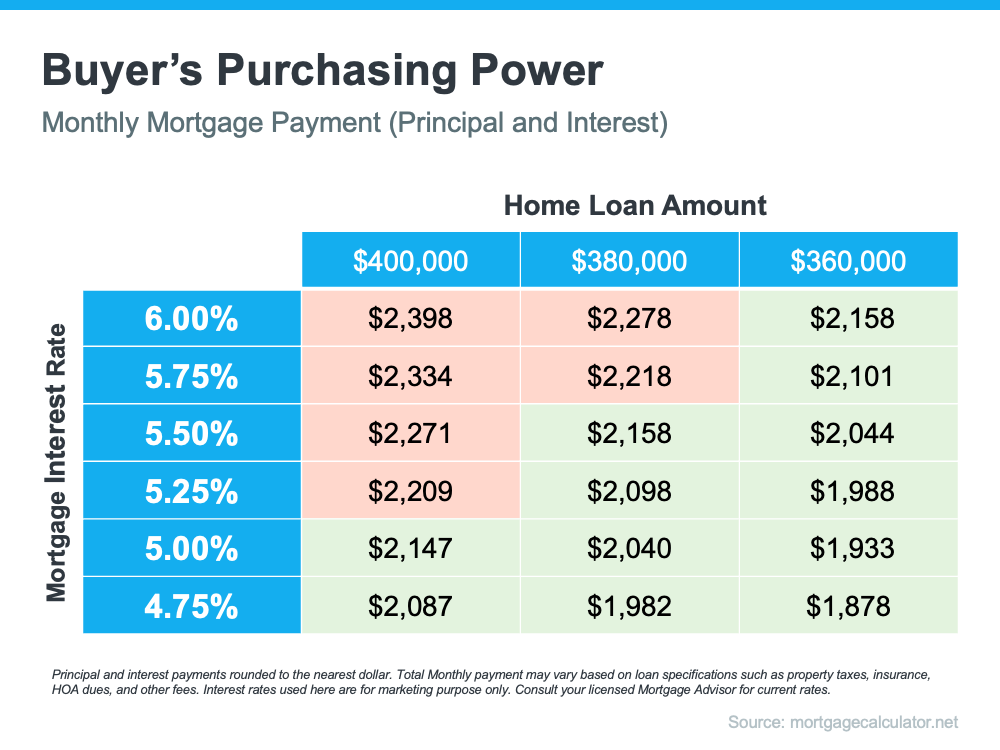

The Current State of Mortgage Interest Rates

To understand where interest rates are today, one must first look at where they have been. For much of the decade following the 2008 financial crisis, and especially during the global pandemic, borrowers enjoyed rates that frequently dipped below 3% or 4%. Today’s environment is starkly different, characterized by a “new normal” where rates often fluctuate between 6% and 8%. While these figures may seem high compared to the recent past, they are closer to the historical average of the last fifty years.

Historical Context vs. Today’s Reality

Perspective is vital in personal finance. During the 1980s, mortgage rates peaked at nearly 18%, making today’s rates look incredibly favorable. Conversely, for the “Zillennial” generation of buyers who entered the market during the COVID-19 era, a 7% rate feels like an insurmountable barrier. The transition from an era of “free money” to one of “expensive credit” has slowed the velocity of the housing market, as current homeowners with low-interest mortgages are hesitant to sell and trade up to a higher-rate loan. This “lock-in effect” has tightened inventory, keeping home prices high despite the increase in borrowing costs.

The Federal Reserve’s Role in Rate Movement

A common misconception is that the Federal Reserve sets mortgage rates directly. In reality, the Fed sets the “Federal Funds Rate,” which is the interest rate banks charge each other for overnight loans. However, mortgage rates are highly sensitive to the Fed’s signals. When the Federal Reserve raises rates to combat inflation, mortgage lenders typically follow suit to maintain their profit margins and account for the increased cost of capital. Today’s rates are a direct reflection of the Fed’s ongoing battle to stabilize the economy, with every announcement from the central bank causing immediate ripples in the mortgage industry.

Key Factors Influencing Your Personalized Rate

While the national average provides a benchmark, the rate a lender offers you personally is a reflection of your “risk profile.” Mortgage lenders are essentially in the business of pricing risk. The lower the perceived risk that you will default on the loan, the lower the interest rate they are willing to offer. Understanding the levers you can pull to lower your rate is essential for any savvy borrower.

Credit Score and Financial Health

Your credit score is the single most influential factor in determining your interest rate. A borrower with a “Very Good” to “Exceptional” FICO score (740 and above) will almost always secure a lower rate than someone in the “Fair” range. Even a 0.5% difference in your interest rate, caused by a lower credit score, can result in tens of thousands of dollars in extra interest payments over the life of a 30-year loan. Beyond the score, lenders look at your Debt-to-Income (DTI) ratio, which measures how much of your monthly income goes toward paying off debts. A lower DTI suggests you have the financial “breathing room” to handle a mortgage.

Loan-to-Value Ratio (LTV) and Down Payments

The Loan-to-Value ratio (LTV) is the amount of the loan compared to the appraised value of the property. If you put down 20%, your LTV is 80%. Generally, the more “skin in the game” you have, the more favorable your rate will be. A larger down payment reduces the lender’s risk because it provides a buffer if home values were to drop. Furthermore, reaching the 20% down payment threshold allows you to avoid Private Mortgage Insurance (PMI), which doesn’t lower your interest rate but does significantly lower your total monthly housing expense.

Loan Type: Fixed-Rate vs. Adjustable-Rate Mortgages (ARMs)

The structure of the loan itself dictates the rate. Fixed-rate mortgages offer stability; your interest rate remains the same for 15, 20, or 30 years. Adjustable-Rate Mortgages (ARMs), however, usually offer a lower “teaser” rate for an initial period (such as 5 or 7 years) before the rate begins to fluctuate based on market conditions. In a high-rate environment, some borrowers opt for ARMs with the intention of refinancing into a fixed-rate loan before the adjustment period begins, though this carries the risk that rates may be even higher in the future.

Economic Indicators to Watch

In the world of business finance, mortgage rates are influenced by the same forces that move the stock and bond markets. If you want to predict where house interest rates might go tomorrow, you need to keep an eye on a few specific economic indicators today.

Inflation and the Consumer Price Index (CPI)

Inflation is the enemy of fixed-income investments like mortgages. When inflation is high, the purchasing power of the future dollars a lender receives from your mortgage payments is eroded. To compensate for this, lenders demand higher interest rates. The Consumer Price Index (CPI) is the most-watched metric for inflation. When CPI reports show that inflation is “sticky” or rising, mortgage rates tend to climb. Conversely, if inflation cools, rates often follow suit as the market anticipates a more dovish stance from the Federal Reserve.

The 10-Year Treasury Yield

There is a strong historical correlation between the yield on the 10-Year U.S. Treasury note and the 30-year fixed-rate mortgage. While they do not move in perfect lockstep, they generally trend in the same direction. When investors are nervous about the economy, they often flock to the safety of government bonds, driving yields down. When the economy is seen as robust or inflationary, yields rise. By monitoring the 10-Year Treasury, potential homebuyers can get a “real-time” look at the direction mortgage rates are headed before they are officially updated by lenders.

Strategies for Securing the Best Rate in a High-Rate Environment

In a market where rates are elevated, being a passive borrower can be expensive. To optimize your personal finances, you must take a proactive approach to the mortgage application process. There are several tools and tactics available to help you trim your interest costs.

The Power of Rate Locks

Mortgage rates can change multiple times in a single day. Once you have found a home and a lender, one of the most important steps is the “rate lock.” This is a guarantee from the lender to honor a specific interest rate for a set period (usually 30 to 60 days) while your loan is processed. In a volatile market, failing to lock in a rate could result in your monthly payment increasing by hundreds of dollars between the time you apply and the time you close. Some lenders even offer “float-down” provisions, which allow you to lock in a rate but still take advantage if rates happen to drop before closing.

Buying Down the Rate with Mortgage Points

If you have extra cash on hand, you can “buy” a lower interest rate through mortgage points. One point typically costs 1% of the total loan amount and reduces your interest rate by about 0.25%. This is essentially “prepaid interest.” To determine if this is a smart financial move, you must calculate the “break-even point”—the amount of time it will take for the monthly savings to equal the upfront cost of the points. If you plan to stay in the home for a long time, buying points can save you a fortune over the life of the loan.

Comparison Shopping and Lender Negotiation

Many borrowers make the mistake of only talking to their primary bank. However, mortgage rates vary significantly between retail banks, credit unions, and independent mortgage brokers. By obtaining “Loan Estimates” from at least three different sources, you can compare not just the interest rate, but the closing costs and origination fees. You can often use a lower offer from one lender as leverage to negotiate better terms with another.

Long-Term Outlook: Should You Buy Now or Wait?

The ultimate question for many is whether to enter the market today or wait for rates to fall. In personal finance, timing the market is notoriously difficult and often counterproductive. The decision should be based more on your individual financial readiness than on speculative interest rate forecasts.

The “Marry the House, Date the Rate” Philosophy

A popular mantra in the current real estate market is “Marry the house, date the rate.” This suggests that if you find the right property, you should buy it now despite the high interest rate, with the intention of refinancing later when rates eventually drop. The logic is that you can change your interest rate in the future, but you cannot change the purchase price of the home. If you wait for rates to drop to 4%, competition may surge, driving home prices up and negating any savings from the lower rate.

Refinancing Opportunities in the Future

While “dating the rate” is a viable strategy, it requires a solid financial foundation. Refinancing is not free; it involves closing costs and requires that your home maintains its value. When considering a purchase today, ensure that you can comfortably afford the monthly payment at the current rate. If rates drop in two or three years, a refinance can serve as a powerful tool to increase your monthly cash flow or shorten your loan term. However, viewing a refinance as a “guarantee” rather than a “possibility” is a risky financial move.

In conclusion, while house interest rates today are higher than the historic lows of the past decade, they remain a manageable part of a well-structured financial plan. By understanding the economic forces at play, optimizing your credit profile, and employing strategic borrowing tactics, you can secure a mortgage that aligns with your long-term wealth-building goals. Real estate remains one of the most consistent paths to financial stability, provided you navigate the interest rate environment with diligence and insight.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.