In the complex world of accounting and business finance, the term “contra account” often surfaces as a point of confusion for small business owners, investors, and even students. At first glance, accounting seems to follow a rigid set of rules: assets go on one side, liabilities on the other, and everything must balance. However, the reality of financial reporting requires more nuance to provide a clear picture of a company’s health.

This is where contra accounts come into play. A contra account is a specialized ledger account that carries a balance opposite to the “normal” balance of its associated category. By design, these accounts are used to reduce the value of another account, allowing businesses to report net values while still maintaining a record of historical costs. Understanding contra accounts is essential for anyone looking to navigate balance sheets, optimize tax strategies, or perform deep-dive financial analysis.

Understanding the Fundamentals of Contra Accounts

To understand a contra account, one must first understand the concept of a “normal balance.” In double-entry bookkeeping, every account has either a debit (left-side) or a credit (right-side) normal balance. For example, asset accounts normally have debit balances, while liability and equity accounts normally have credit balances.

Definition and Purpose

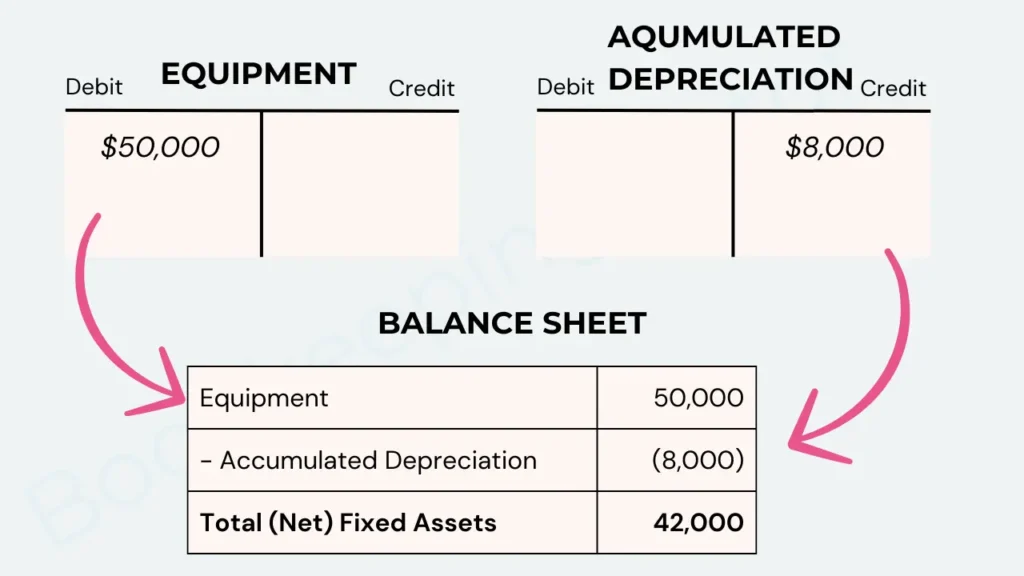

A contra account (the word “contra” literally meaning “against”) exists specifically to offset a related account. While it would be mathematically possible to simply subtract amounts directly from the main account, doing so would erase vital historical data. For instance, if a company bought a machine for $50,000, they want to keep that $50,000 figure on the books for historical reference. Instead of reducing that $50,000 every year as the machine wears out, they use a contra account to track the decrease in value.

The primary purpose of a contra account is to provide transparency. It allows stakeholders to see both the original cost (gross) and the adjustments (the contra) to arrive at the current value (net). This “book value” is what ultimately impacts the company’s bottom line and tax obligations.

The Normal Balance Rule (Debits vs. Credits)

The mechanics of a contra account are simple but counter-intuitive for beginners. A contra account’s normal balance is the inverse of the account it is paired with.

- Contra Asset: Since an asset’s normal balance is a debit, a contra asset’s normal balance is a credit.

- Contra Liability: Since a liability’s normal balance is a credit, a contra liability’s normal balance is a debit.

- Contra Revenue: Since revenue’s normal balance is a credit, a contra revenue’s normal balance is a debit.

- Contra Equity: Since equity’s normal balance is a credit, a contra equity’s normal balance is a debit.

By maintaining these “opposite” balances, the contra account effectively reduces the balance of the primary account when they are reported together on financial statements.

Common Types of Contra Accounts in Business Finance

Contra accounts are not rare outliers; they are fundamental components of GAAP (Generally Accepted Accounting Principles) and IFRS (International Financial Reporting Standards). They appear across different sections of the balance sheet and income statement.

Contra Asset Accounts: Depreciation and Bad Debt

The most frequent application of contra accounts is found in the asset section of the balance sheet.

- Accumulated Depreciation: When a business purchases a long-term asset like a vehicle or equipment, the value of that asset declines over time. Rather than lowering the original “Equipment” account, the business credits “Accumulated Depreciation.” On the balance sheet, the Equipment account minus the Accumulated Depreciation equals the “Net Book Value.”

- Allowance for Doubtful Accounts: Not every customer who buys on credit will pay their bill. To remain conservative and realistic, businesses estimate how much of their Accounts Receivable will go unpaid. This estimate is stored in the “Allowance for Doubtful Accounts,” a contra asset that reduces the total Accounts Receivable to a more realistic “Net Realizable Value.”

Contra Revenue Accounts: Returns and Discounts

On the income statement, contra revenue accounts help a business track the difference between its “Gross Sales” and “Net Sales.”

- Sales Returns and Allowances: When a customer returns a product or is given a partial refund for a defective item, the business debits this contra revenue account rather than reducing the Sales account directly. This allows management to see exactly how much revenue is being lost to returns—a key indicator of product quality or customer satisfaction.

- Sales Discounts: If a business offers a “2/10, n/30” discount (a 2% discount if paid within ten days), the amount of that discount is recorded in a Sales Discount account. This helps the finance team analyze whether the incentive is successfully speeding up cash flow.

Contra Liability and Contra Equity Accounts

While less common for small businesses, these are vital for corporate finance and investment analysis.

- Discount on Bonds Payable: This is a contra liability account. If a company issues bonds at a price below their face value, the “Discount” account reduces the carrying amount of the liability on the balance sheet.

- Treasury Stock: This is the most common contra equity account. When a corporation buys back its own shares from the open market, it doesn’t “delete” the equity. Instead, it records the cost in Treasury Stock. Since equity normally has a credit balance, Treasury Stock has a debit balance, thereby reducing total shareholders’ equity.

The Role of Contra Accounts in Financial Reporting and Analysis

For investors and financial analysts, contra accounts are not just technical entries; they are “truth-tellers” that reveal the reality behind the headline numbers.

Book Value vs. Market Value

Contra accounts are the bridge between historical cost and current book value. If an investor looks at a balance sheet and sees $1 million in “Fixed Assets,” they might be impressed. However, if they see an associated contra account of $900,000 in “Accumulated Depreciation,” they realize the equipment is old and likely near the end of its useful life. This insight is crucial for forecasting future capital expenditures (CapEx). Without the contra account, the investor would be blind to the age and condition of the company’s physical infrastructure.

Transparency and Investor Confidence

A business that hides its “Allowance for Doubtful Accounts” or “Sales Returns” by netting them directly into the primary accounts is often viewed with suspicion. Comprehensive reporting requires showing the gross numbers. High levels in contra revenue accounts can signal systemic issues: perhaps the marketing team is over-promising, or the manufacturing department is producing faulty goods. By separating these figures, management can identify and fix specific operational bottlenecks rather than just wondering why net income is lower than expected.

Practical Applications for Small Business Owners and Investors

Whether you are managing a side hustle or evaluating a stock for your portfolio, contra accounts provide actionable intelligence.

Tax Implications and Asset Management

For the small business owner, contra assets like Accumulated Depreciation are directly tied to tax strategy. Depreciation is a non-cash expense that reduces taxable income. By properly maintaining these contra accounts, business owners ensure they are following IRS guidelines (such as Section 179 deductions or MACRS depreciation) while keeping an organized ledger that can withstand an audit. It also assists in “Asset Tracking”—knowing when an asset is fully depreciated can trigger a decision to sell, upgrade, or replace equipment.

Identifying Red Flags in Financial Statements

From an investment perspective, the relationship between a primary account and its contra account can reveal a company’s financial health or aggressive accounting tactics.

- The Receivables Ratio: If “Accounts Receivable” is growing rapidly but the “Allowance for Doubtful Accounts” (the contra asset) is staying flat or shrinking, the company may be artificially inflating its reported assets. This could be a sign that they are struggling to collect cash but are unwilling to admit it on the balance sheet.

- The Treasury Stock Signal: A growing Treasury Stock account (contra equity) often indicates that a company is confident in its future and has excess cash to return to shareholders. Conversely, it could be a move to artificially boost Earnings Per Share (EPS) by reducing the number of shares outstanding.

Conclusion: Why Contra Accounts Matter

Contra accounts may seem like a redundant layer of bookkeeping, but they are the guardians of financial clarity. They allow for the preservation of historical data while presenting an honest, adjusted view of a company’s current value. For the professional in the money niche—whether an accountant, a business owner, or a savvy investor—mastering these accounts is a prerequisite for financial literacy. By looking beyond the “net” and into the “contra,” you gain the ability to see the true story behind the numbers, leading to better-informed decisions and more robust financial growth.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.