The term “checks” can evoke a variety of images, from the familiar paper document used for transactions to the rigorous evaluation of systems and ideas. In the realm of personal finance and business operations, checks represent a tangible and historically significant method of transferring funds. While the digital age has introduced a plethora of faster and more convenient payment methods, understanding the mechanics and relevance of checks remains crucial for many individuals and businesses, especially in specific financial contexts. This exploration delves into the world of financial checks, uncovering their fundamental purpose, the processes involved, and their enduring, albeit evolving, role in the modern financial landscape.

The Fundamental Mechanics of a Financial Check

At its core, a financial check is a written order, typically from a bank account holder (the drawer), instructing a financial institution (the drawee bank) to pay a specific sum of money to a designated person or entity (the payee). This seemingly simple instrument carries significant legal weight and relies on a complex interplay of parties and processes to function effectively.

Components of a Check: The Anatomy of a Transaction

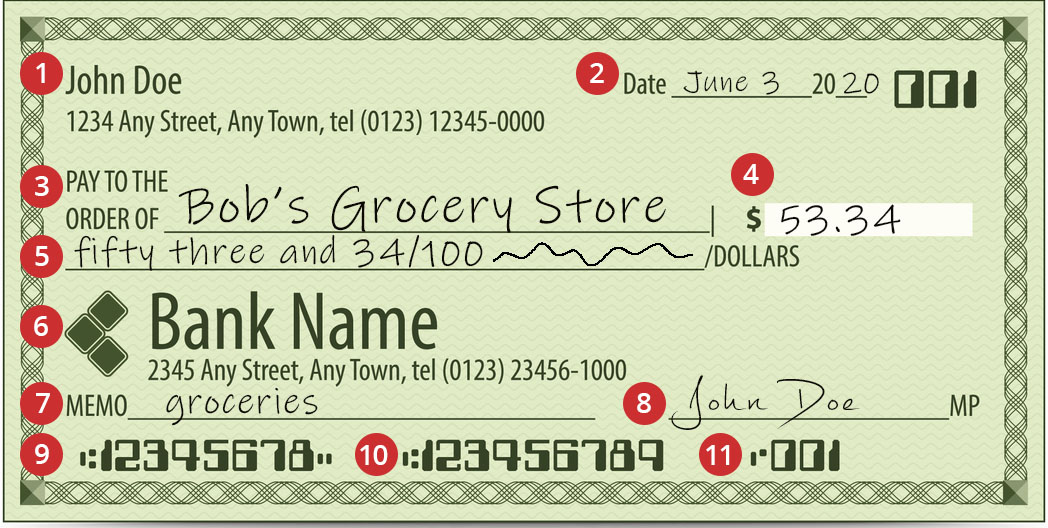

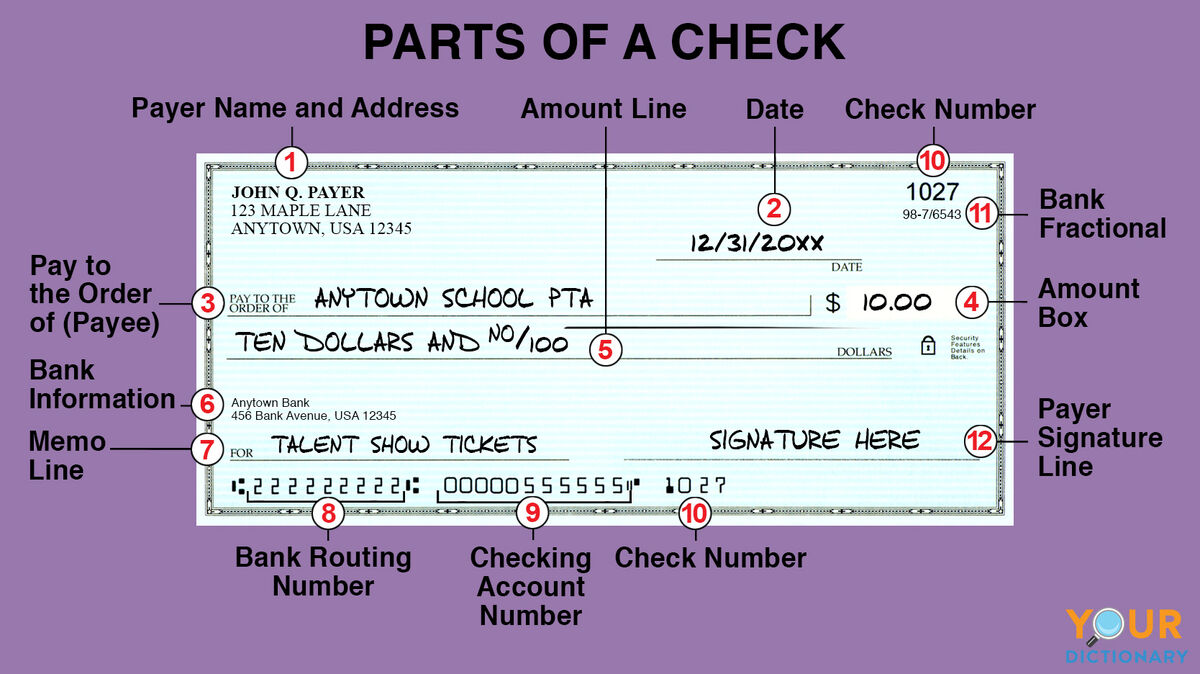

Every physical check, regardless of its issuer or recipient, is adorned with several key pieces of information that are essential for its validity and processing. Understanding these components is fundamental to grasping how a check works.

- Check Number: Usually found in the upper right-hand corner, this sequential number helps with record-keeping for both the account holder and the bank. It allows for easy tracking of individual checks written and cleared.

- Date: The date the check is written is crucial. It determines when the check is valid for deposit or cashing. Post-dating a check (writing a future date) doesn’t legally obligate the bank to hold it until that date; it can often be cashed or deposited immediately, though it might be a signal of intent between the parties involved.

- Payee Name: This is the name of the individual or organization to whom the money is to be paid. Accuracy here is paramount; a misspelling can lead to complications.

- Numeric Amount: The amount of money to be paid is written in numerals in a designated box. This provides a clear and unambiguous monetary value.

- Written Amount: The same amount as the numeric amount is written out in words. This serves as a crucial safeguard. In cases of discrepancy between the numeric and written amounts, the written amount is legally considered the correct one, preventing potential fraud or errors.

- Memo Line: This space is optional and used by the drawer to add a note about the purpose of the check, such as “Rent – June” or “Invoice #1234.” It’s for personal reference and has no legal bearing on the payment itself.

- Signature Line: The drawer’s signature is the most critical element, authorizing the payment. Without a valid signature, the check is void.

- Bank Name and Address: This identifies the financial institution on which the check is drawn.

- Account Number (or Routing Number): Typically found at the bottom of the check, along with the routing number, these identify the specific bank and the drawer’s account from which the funds will be debited. The routing number is a nine-digit code that identifies the financial institution, while the account number identifies the specific account.

The Journey of a Check: From Drawer to Depositor

The process of a check clearing is a multi-step operation involving the drawer, the payee, and multiple banking institutions.

- Issuance and Delivery: The drawer writes a check, fills in all the necessary details, signs it, and gives it to the payee.

- Deposit or Cashing: The payee then deposits the check into their own bank account or attempts to cash it at a bank.

- Bank Processing (Payee’s Bank): If deposited, the payee’s bank receives the check. They will typically place a hold on the funds for a certain period, allowing time for the check to clear.

- Clearinghouse or Direct Exchange: The payee’s bank then sends the check to a clearinghouse or directly to the drawer’s bank. Clearinghouses are facilities that facilitate the exchange of checks between different banks.

- Drawer’s Bank Processing: The drawer’s bank receives the check and verifies the signature, checks for sufficient funds in the drawer’s account, and confirms the routing and account numbers.

- Debit and Credit: If all is in order, the drawer’s bank debits the amount from the drawer’s account and sends the funds to the payee’s bank. The payee’s bank then credits the payee’s account.

- Return (Non-Sufficient Funds or Other Issues): If there are insufficient funds in the drawer’s account (a “bounced” or “returned” check), the check is returned to the payee’s bank, and the payee may incur fees. Other reasons for return can include a stop payment order, a forged signature, or an illegible check.

Why Do Checks Still Matter in the Digital Age?

Despite the pervasive rise of electronic payment methods like debit cards, credit cards, online transfers, and mobile payment apps, checks continue to hold a place in the financial ecosystem. Their continued relevance stems from a combination of user preference, specific transaction types, and legacy systems.

User Preferences and Accessibility

For some individuals, particularly those who are less technologically inclined or who prefer a tangible record of their transactions, checks offer a familiar and comfortable method of payment. This can include older demographics or individuals who have historically relied on checks for budgeting and financial management. Furthermore, in certain situations, like paying for services at a small local business or a community event, a check might still be the most readily accepted form of payment.

Specific Transaction Scenarios

Certain financial transactions still lend themselves to the use of checks, often due to legal requirements or the nature of the payment.

- Rent and Mortgage Payments: While many landlords and mortgage companies offer online payment portals, some still prefer or require checks, especially for individual homeowners or smaller rental agencies. This can also provide a physical record for both parties.

- Business-to-Business Transactions: In some B2B relationships, especially with smaller businesses or those in traditional industries, checks remain a common payment method. This can be due to established accounting practices, terms of service, or a lack of integration with newer payment systems.

- Government Payments and Disbursements: While many government agencies have moved towards direct deposit, some still issue payments via check, such as tax refunds or benefit disbursements, particularly for individuals who have not opted for electronic transfer.

- Large Purchases and Down Payments: For significant transactions like buying a car or a home, a cashier’s check or a certified check is often required. These are guaranteed forms of payment issued by a bank, offering a higher level of security than a personal check.

The Role of Alternative and Hybrid Payment Methods

The evolution of payment systems has also seen the rise of “checks” in a digital or hybrid form, bridging the gap between traditional paper checks and fully electronic transactions.

- Electronic Checks (e-checks): An e-check is essentially a digital version of a paper check. Instead of writing out a physical document, you provide your bank account and routing numbers electronically, often through a secure website or app. The transaction is then processed electronically, similar to an ACH (Automated Clearing House) transfer. E-checks are often used for online bill payments, direct deposits, and recurring subscriptions. They offer the convenience of electronic payment while mimicking the direct debiting from a bank account associated with a check.

- Mobile Check Deposit: Many banking apps now allow users to deposit checks remotely by taking photos of the front and back of the check. This technology has significantly reduced the need for individuals to visit a bank branch to deposit a check, making the process more convenient. The check is still processed through the traditional clearing system, but the user’s interaction with it is modernized.

- Remote Deposit Capture (RDC) for Businesses: Businesses often utilize RDC systems that allow them to scan checks at their location and transmit the images electronically to their bank for processing. This streamlines accounts receivable and reduces trips to the bank.

The Evolving Landscape of Check Usage and Future Outlook

The trend in check usage is undeniably downward. As digital payment solutions become more sophisticated, secure, and widely adopted, the reliance on paper checks diminishes. However, their complete disappearance from the financial landscape is not imminent, and their evolution is an ongoing process.

Declining Transaction Volumes and Shifting Habits

Data consistently shows a decline in the number of checks processed annually. This is a direct reflection of changing consumer and business habits, driven by the ease and speed of electronic transactions. Mobile banking, contactless payments, and instant payment platforms are becoming the norm for everyday transactions.

Regulatory and Banking Trends

Banks and financial institutions are also actively encouraging the shift away from paper checks. The cost associated with processing physical checks, including printing, handling, and clearing, is significantly higher than that of electronic transactions. As such, banks are investing more in digital infrastructure and may even implement fees or reduced services for check-heavy accounts in the future. Regulatory bodies are also increasingly promoting electronic payments for efficiency and security.

The Persistence of Niche Uses and the Role of Transition

Despite the overall decline, certain niche areas will likely see checks persist for a considerable time. As mentioned earlier, specific industries, demographic groups, and transaction types will continue to rely on checks. Furthermore, the transition to a fully digital payment system is a gradual one. For many businesses and individuals, a complete overhaul of their payment infrastructure is a significant undertaking. Checks provide a familiar bridge during this transition.

Innovation in Check-Related Technologies

While the physical check itself may be in decline, the underlying technology and processes associated with it are evolving. Innovations in fraud detection, secure digital transmission of check images, and more efficient clearing mechanisms are still being developed. The concept of a “check” as a form of authorization for payment from a bank account is likely to endure, even if its physical manifestation changes.

In conclusion, while the iconic paper check might seem like a relic of the past to many, its fundamental purpose as a secure and documented method of fund transfer continues to hold relevance. From its intricate components and the detailed process of its clearing to its enduring role in specific financial scenarios and its evolution into digital alternatives, understanding “what are checks” provides valuable insight into the mechanics of financial transactions and the ongoing adaptation of the financial system. As technology advances, the form and frequency of checks will undoubtedly continue to change, but the underlying principles of authorized payment from a bank account are likely to remain a cornerstone of financial operations for years to come.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.