In the world of finance, the word “asset” is more than just a buzzword; it is the fundamental building block of wealth and economic stability. Whether you are an individual looking to secure your retirement or a business owner aiming to scale your operations, understanding what qualifies as an asset—and how to acquire the right ones—is critical. At its core, an asset is any resource with economic value that an individual, corporation, or country owns or controls with the expectation that it will provide a future benefit.

Assets are the engines that generate cash flow, reduce expenses, or improve sales. While a liability takes money out of your pocket, an asset puts money into it. However, not all assets are created equal. They vary in liquidity, risk, and growth potential. To master your financial life, you must be able to identify different types of assets and understand how they function within a diversified portfolio.

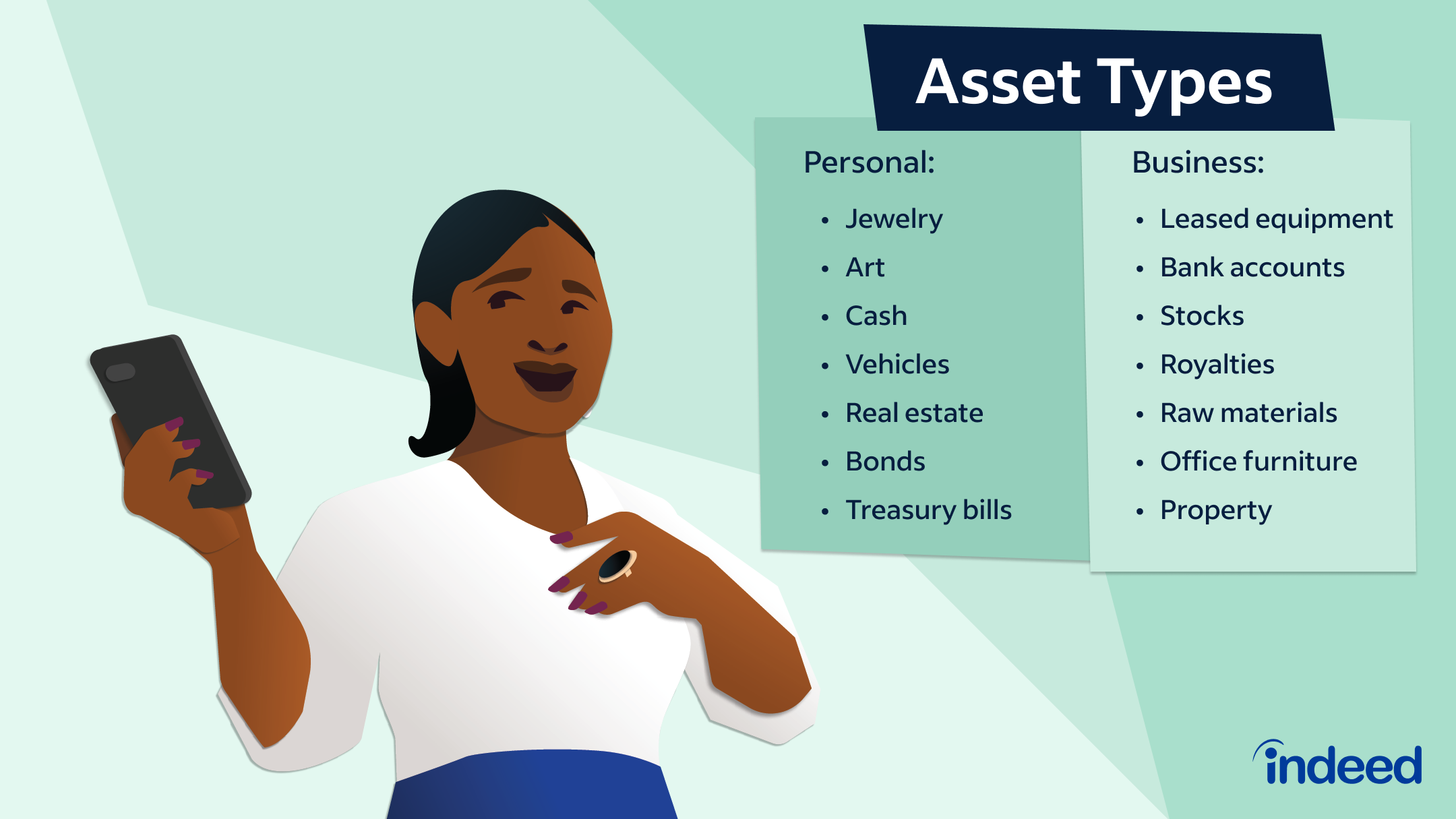

Understanding Personal Assets: Building Your Individual Net Worth

Personal assets are the items of value that an individual or household owns. These are typically calculated to determine a person’s net worth (Assets minus Liabilities). For most individuals, the goal of financial planning is to convert earned income into appreciating or income-generating assets.

Liquid Assets and Cash Equivalents

Liquidity refers to how quickly an asset can be converted into cash without losing significant value. Cash is the most liquid asset. Examples include:

- Checking and Savings Accounts: These are the most accessible forms of capital, used for daily transactions and emergency funds.

- Certificates of Deposit (CDs): While they have a fixed term, they are considered low-risk assets that earn a slightly higher interest rate than standard savings.

- Money Market Funds: These are short-term debt instruments that offer higher yields than savings accounts while maintaining high liquidity.

Investment Assets

Investment assets are purchased with the specific goal of generating a return over time, either through capital appreciation or dividend payments.

- Equities (Stocks): Owning shares in a company allows you to participate in its growth. Historically, stocks have been one of the most effective ways to build long-term wealth.

- Bonds (Fixed Income): When you buy a bond, you are essentially lending money to a government or corporation in exchange for periodic interest payments plus the return of the principal.

- Mutual Funds and ETFs: These are baskets of stocks or bonds that provide instant diversification, allowing investors to own a piece of many different assets through a single vehicle.

Real Estate and Tangible Personal Property

For many, a primary residence is their most significant asset. However, the definition of an asset can be nuanced here; while a home has value, it also incurs costs.

- Investment Real Estate: Property purchased specifically to generate rental income or for resale at a higher price.

- Collectibles and Commodities: This includes gold, silver, fine art, and vintage automobiles. These assets act as a hedge against inflation, though they often lack the liquidity of financial markets.

Business Assets: The Engine of Corporate Growth

In a corporate context, assets are listed on the balance sheet and are used to help the company operate and generate revenue. Businesses categorize assets based on how long they intend to hold them and their physical nature.

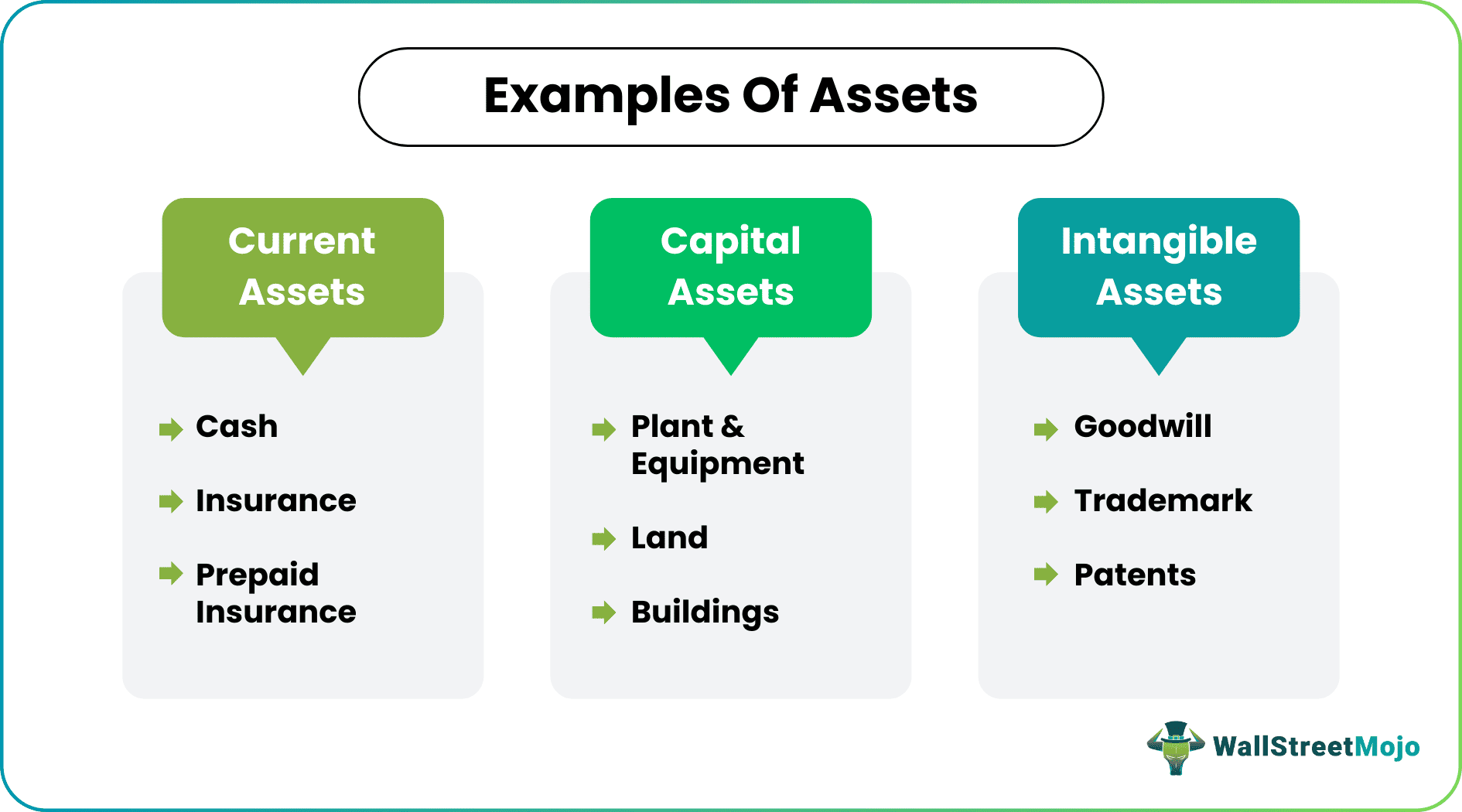

Current Assets

Current assets are expected to be converted into cash or used up within one year. They are vital for maintaining the “working capital” of a business.

- Inventory: The raw materials, work-in-progress goods, and finished products that a company intends to sell to customers.

- Accounts Receivable: This represents money owed to the business by customers who have purchased goods or services on credit.

- Prepaid Expenses: Payments made in advance for services to be received in the future, such as insurance premiums or rent.

Fixed (Long-Term) Assets

Fixed assets, also known as Capital Assets or Property, Plant, and Equipment (PP&E), are long-term investments used in the operation of the business.

- Real Estate and Infrastructure: This includes the land, office buildings, warehouses, and factories owned by the company.

- Machinery and Equipment: The tools and technology required to produce goods, from heavy manufacturing robots to office laptops.

- Vehicles: Trucks, delivery vans, and corporate cars used for business logistics.

Intangible Assets and Intellectual Property

Not all business assets can be touched. In the modern economy, intangible assets are often more valuable than physical ones.

- Brand Equity and Goodwill: The reputation and customer loyalty a company has built over time. When one company acquires another for more than its book value, the excess is recorded as “goodwill.”

- Patents, Trademarks, and Copyrights: Legal protections for inventions, logos, and creative works that prevent competitors from using a company’s unique innovations.

- Proprietary Software and Data: In the age of digital finance, the algorithms and customer data owned by a firm are significant strategic assets.

Classifying Assets: Tangibility, Accessibility, and Usage

To manage a portfolio or a business balance sheet effectively, it is helpful to group assets by their specific characteristics. Financial experts typically use three main methods of classification.

Tangible vs. Intangible Assets

This classification is based on physical existence.

- Tangible Assets: These have a physical form. Examples include land, cash, equipment, and gold. They are generally easier to value because they can be appraised based on physical condition and market demand.

- Intangible Assets: These lack physical substance but hold significant long-term value. Examples include brand recognition, intellectual property, and contractual rights. While harder to value, they often provide the “moat” that protects a business from competition.

Current vs. Non-Current Assets

This classification is based on time and liquidity.

- Current Assets: As mentioned, these are short-term resources (cash, inventory). They are essential for meeting immediate financial obligations.

- Non-Current Assets: These are long-term investments that are not easily converted to cash. This includes long-term investments in other companies, real estate, and heavy machinery. They are intended to provide value for many years.

Operating vs. Non-Operating Assets

This classification is based on the asset’s role in daily business activities.

- Operating Assets: Assets required for the daily functions of a business, such as cash, inventory, and patents.

- Non-Operating Assets: Assets that are not necessary for daily operations but still provide value. Examples include unallocated cash sitting in a high-yield account, vacant land held for future development, or investments in other companies.

Strategic Asset Allocation for Wealth Creation

Simply knowing the examples of assets is not enough; one must understand how to allocate capital across these categories to achieve specific financial goals. Asset allocation is the process of deciding how to distribute your wealth among different asset classes to balance risk and reward.

The Importance of Diversification

The primary rule of investing is “don’t put all your eggs in one basket.” By holding a mix of asset types—such as stocks (growth), bonds (stability), and real estate (tangibility)—you protect yourself from a downturn in any single sector. For example, when the stock market is volatile, gold or real estate may remain stable or even increase in value.

Risk Tolerance and Time Horizon

Your choice of assets should depend on your age and financial objectives.

- Growth Focus: Younger individuals or aggressive businesses may lean toward “equities” and “intangible assets” like startups or high-growth stocks, which offer high potential returns but come with higher risk.

- Preservation Focus: Those nearing retirement or businesses looking for stability often shift toward “fixed-income assets” and “liquid assets” to ensure capital preservation and steady cash flow.

The Role of Digital Assets in the Modern Portfolio

In the last decade, a new category has emerged: digital assets.

- Cryptocurrencies: Digital currencies like Bitcoin are increasingly viewed as “digital gold”—a speculative asset and a potential hedge against fiat currency devaluation.

- NFTs and Digital Goods: While highly speculative, these represent a shift in how ownership and value are perceived in a digital-first economy.

- Digital Real Estate: Domain names and virtual spaces in the metaverse are now being treated as legitimate assets by forward-thinking investors.

Conclusion: Turning Knowledge into Wealth

Understanding the various examples of assets is the first step toward financial literacy. Whether you are managing a household budget or a corporate ledger, your success depends on your ability to acquire assets that appreciate in value or generate consistent income.

From the tangibility of real estate and machinery to the intangible power of a strong brand or a patent, assets are the tools we use to build a secure future. By categorizing your holdings into liquid, fixed, and investment categories, you can better navigate economic shifts and ensure that your money is working as hard for you as you did to earn it. The key to long-term prosperity is not just earning a high income, but consistently converting that income into a diversified portfolio of high-quality assets.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.