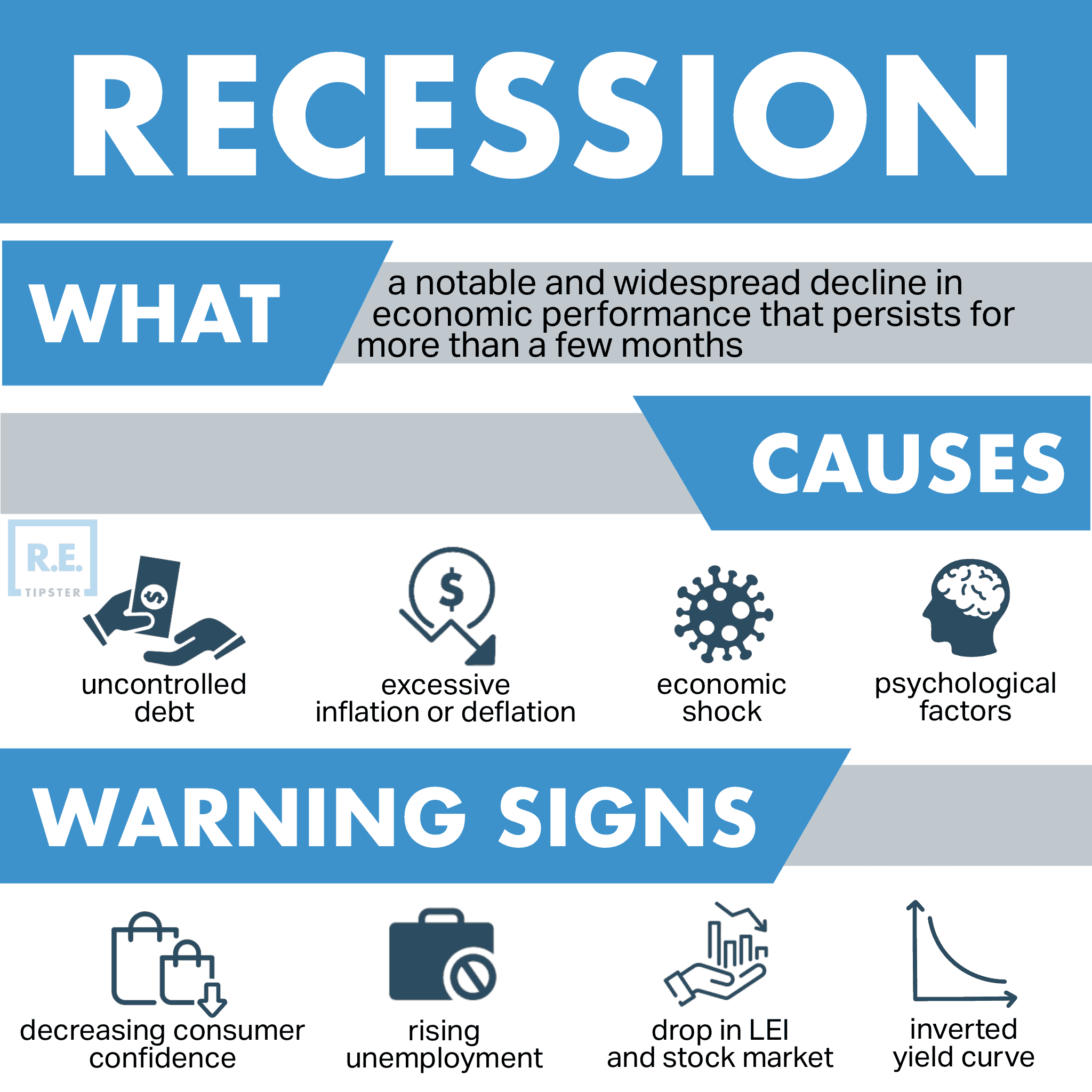

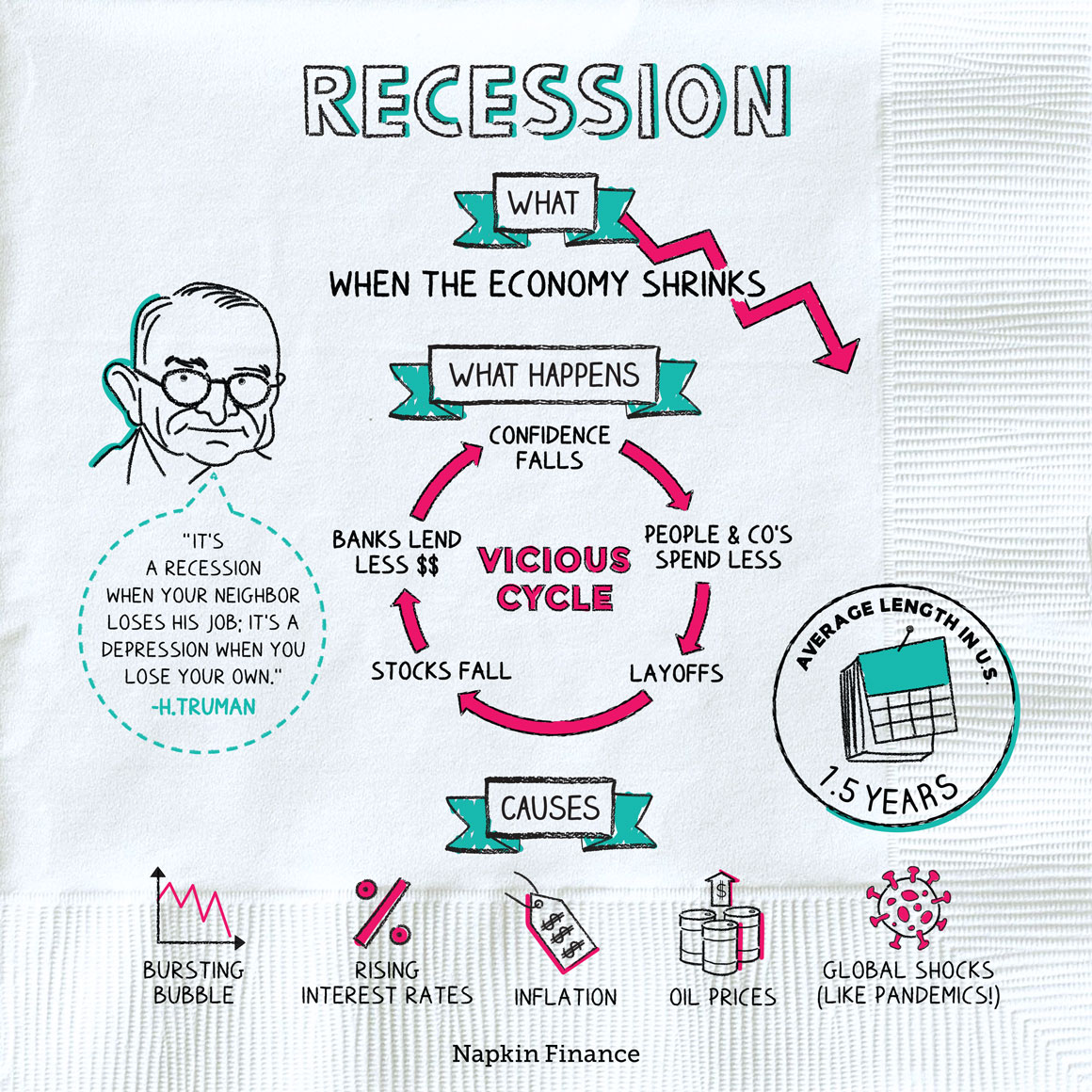

In the complex ecosystem of global finance, a recession is more than just a buzzword found in news headlines; it is a significant period of decline in economic activity, spread across the economy and lasting more than a few months. Traditionally defined by two consecutive quarters of negative Gross Domestic Product (GDP) growth, a recession impacts everything from corporate profit margins to the stability of personal savings accounts. Understanding the mechanics of why an economy contracts is essential for investors, business owners, and individuals looking to safeguard their financial future.

While every economic cycle is unique, recessions are rarely the result of a single isolated event. Instead, they are usually the culmination of several overlapping factors that strain the financial system until it reaches a breaking point. By examining the five primary causes of a recession, we can better understand the warning signs and the structural vulnerabilities inherent in modern market economies.

1. Monetary Policy Overcorrection and Interest Rate Volatility

The relationship between central banks and the broader economy is perhaps the most influential factor in determining the onset of a recession. Central banks, such as the Federal Reserve in the United States, use monetary policy to balance the scales between stimulating growth and controlling inflation.

The Role of the Central Bank in Inflation Management

When an economy “runs hot,” demand for goods and services outpaces supply, leading to inflation. To cool this down, central banks raise interest rates. Higher rates make borrowing more expensive for both businesses and consumers. While this is a necessary tool for maintaining price stability, it is a delicate balancing act. If the central bank raises rates too aggressively or maintains “higher for longer” policies beyond what the market can bear, it can inadvertently choke off economic activity entirely.

The Lag Effect of Tightening

One of the most dangerous aspects of monetary policy is the “lag effect.” Changes in interest rates can take 12 to 18 months to fully manifest in the economy. This delay creates a risk where the central bank continues to tighten policy based on old data, failing to realize they have already slowed the economy sufficiently. By the time the contraction is visible in employment or spending data, the momentum toward a recession may already be unstoppable. This “hard landing” is a classic catalyst for economic downturns, as seen in various cycles throughout the late 20th century.

2. The Bursting of Asset Bubbles and Market Speculation

Recessions are frequently preceded by a period of “irrational exuberance,” a term coined by former Fed Chairman Alan Greenspan. This occurs when the prices of specific assets—such as real estate, stocks, or commodities—rise far above their intrinsic value due to speculative buying rather than fundamental economic strength.

The Wealth Effect in Reverse

During an asset bubble, consumers feel wealthier because the value of their homes or investment portfolios is skyrocketing. This “wealth effect” encourages increased spending and borrowing. However, when the bubble inevitably bursts, the process reverses with a vengeance. As asset prices plummet, net worth evaporates, leading to a sudden and sharp contraction in consumer spending. Because consumer spending typically accounts for a vast majority of GDP in developed nations, this withdrawal is a direct ticket to a recession.

Historical Lessons: Dot-Coms and Housing

History provides stark examples of this phenomenon. The 2001 recession was triggered by the bursting of the tech-heavy Dot-com bubble, where valuations for internet companies were disconnected from actual earnings. More significantly, the 2008 Great Recession was fueled by a collapse in the subprime mortgage market. When the housing bubble burst, it didn’t just affect homeowners; it crippled the global financial institutions that held mortgage-backed securities, leading to a systemic freeze in credit markets that took years to thaw.

3. Sudden Economic Shocks and Supply Chain Disruptions

While many recessions are the result of internal market imbalances, some are triggered by external “Black Swan” events—unpredictable occurrences that have severe and widespread consequences. These shocks can disrupt the supply of essential goods, causing costs to spike and production to stall.

Geopolitical Volatility and Energy Costs

Energy is the lifeblood of the global economy. A sudden, sharp increase in the price of oil or natural gas can act as a massive tax on both businesses and consumers. When energy costs spike—often due to geopolitical conflict or OPEC production shifts—the cost of manufacturing and transporting goods rises. Businesses are then forced to choose between raising prices (contributing to inflation) or cutting staff to maintain margins. Historically, many of the recessions in the 1970s were directly linked to oil embargoes and the resulting energy crises.

The Fragility of Global Interdependence

In the modern era, supply chains are highly optimized but fragile. A disruption in one part of the world—whether due to a pandemic, a regional war, or a natural disaster—can cause a domino effect. When manufacturers cannot get the components they need, production halts. This leads to a decline in output and, eventually, a decline in GDP. The sudden stop of global trade and the subsequent supply chain snarls witnessed in the early 2020s serve as a modern case study in how external shocks can trigger rapid, deep economic contractions.

4. Excessive Debt Accumulation and the Credit Cycle

Debt is a powerful tool for growth, allowing companies to invest and consumers to purchase homes and education. However, when debt levels reach a point of “over-leveraging,” the economy becomes highly sensitive to any fluctuations in income or interest rates.

The Trap of Corporate Over-leveraging

During periods of economic prosperity and low interest rates, companies often take on significant debt to fund expansions or stock buybacks. As long as revenues are growing, this debt is manageable. However, if the economy slows down even slightly, these companies may struggle to meet their interest payments. This leads to a wave of corporate defaults and bankruptcies, which in turn leads to layoffs and a reduction in capital expenditure, further cooling the economy.

The Debt Deflation Spiral

Economist Irving Fisher famously described the “debt-deflation” theory, where the attempt to pay down debt actually makes the economic situation worse. As businesses and individuals rush to liquidate assets to pay off loans, asset prices fall further. This lowers the value of collateral, leading to more margin calls and further liquidation. This vicious cycle can turn a mild slowdown into a severe recession or even a depression, as the financial system’s ability to lend—the “oil” in the economic engine—is completely depleted.

5. Sharp Declines in Consumer Confidence and the Paradox of Thrift

Economics is as much about psychology as it is about mathematics. The health of the economy depends heavily on the “animal spirits”—the confidence and instincts of consumers and business leaders. When this confidence wanes, it can create a self-fulfilling prophecy of economic decline.

The Psychology of Fear and Spending

Consumer spending is the primary engine of growth in most modern economies. If consumers become worried about the future—perhaps due to news of layoffs in other sectors or general political instability—they begin to pull back. They delay purchasing new cars, postpone home renovations, and reduce discretionary spending on travel and dining. When millions of people make this choice simultaneously, the aggregate demand in the economy drops, leading businesses to reduce production and lay off workers, which then confirms the consumers’ initial fears.

The Paradox of Thrift

This leads to what economists call the “Paradox of Thrift.” While saving money is a virtuous and responsible act for an individual during uncertain times, if everyone saves more at the same time, total demand falls. This drop in demand reduces total income in the economy, which ironically makes it harder for everyone to save in the long run. This psychological shift can turn a minor market correction into a full-blown recession, as the circulation of money slows to a crawl.

Conclusion: Navigating the Economic Cycle

Recessions are an inevitable, albeit painful, part of the business cycle. They serve as a period of “creative destruction,” where inefficient companies are weeded out and market imbalances are corrected. However, the human and financial cost of these downturns is significant. By identifying the five major causes—monetary policy errors, asset bubbles, external shocks, excessive debt, and psychological shifts—investors and businesses can better prepare for the lean years.

In the world of personal finance and business strategy, the best defense against a recession is a proactive offense. This includes maintaining healthy liquidity, avoiding excessive leverage during peak market years, and staying informed about the macro-economic indicators that signal a shift in the wind. While we may not be able to prevent the next recession, understanding its origins allows us to navigate the storm with greater resilience and strategic foresight.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.