Navigating the complexities of retirement savings can often feel like a marathon, with various rules and strategies designed to help individuals secure their financial future. Among the most powerful tools available for those approaching their golden years are 401k catch-up contributions. These provisions offer a unique opportunity for individuals aged 50 and older to supercharge their retirement savings, making up for lost time or simply enhancing their nest egg. For many, they represent a critical final push to ensure a comfortable and secure retirement, leveraging tax advantages and compounding growth during a pivotal stage of their financial lives. Understanding how these contributions work, who qualifies, and their significant benefits is essential for anyone aiming to maximize their retirement readiness.

Understanding Standard 401k Contribution Limits

Before delving into the specifics of catch-up contributions, it’s crucial to grasp the foundation: the standard 401k contribution limits set by the Internal Revenue Service (IRS). These limits define the maximum amount an employee can contribute to their 401k plan from their salary each year.

The Basic Annual Limit

Each year, the IRS establishes a maximum dollar amount that individuals under the age of 50 can contribute to their 401k, 403(b), most 457 plans, and the Thrift Savings Plan (TSP). This limit is subject to annual adjustments, typically increasing to account for inflation and economic changes. For instance, in 2023, the standard employee contribution limit was $22,500, which rose to $23,000 for 2024. These limits apply solely to the employee’s elective deferrals from their paychecks, whether made on a pre-tax basis or as Roth 401k contributions. Exceeding this limit within a single calendar year can lead to tax penalties and administrative complications, underscoring the importance of staying informed about current IRS guidelines.

Employer Contributions and Their Impact

It’s important to distinguish between an employee’s personal contributions and those made by their employer. Employer contributions, which can take the form of matching contributions (e.g., dollar-for-dollar up to a certain percentage of salary) or profit-sharing contributions, are separate from the employee’s individual contribution limit. There is a separate, higher overall limit that combines both employee and employer contributions. For example, in 2024, the total contribution limit (employee + employer) for defined contribution plans is $69,000. This generous combined limit allows for substantial retirement savings, particularly for those whose employers offer robust benefits packages. However, the catch-up contribution specifically pertains to the additional amount an employee can contribute above their standard elective deferral limit.

Why Limits Exist

The existence of contribution limits serves multiple purposes within the U.S. tax code. Primarily, they are designed to balance the incentive for individuals to save for retirement with the government’s need to collect tax revenue. By allowing contributions to grow tax-deferred (or tax-free in the case of Roth accounts), the government provides a powerful incentive for long-term savings. However, without limits, high-income earners could potentially defer an unlimited amount of income from taxation, which would significantly reduce current tax receipts and concentrate tax benefits disproportionately. These limits ensure that the tax advantages of retirement plans are broadly available while also encouraging responsible fiscal planning over a career.

The Mechanics of 401k Catch-Up Contributions

The concept of catch-up contributions is specifically designed to provide a financial boost to older workers, acknowledging that life circumstances, career changes, or delayed financial planning might have prevented them from maximizing their retirement savings earlier on.

Who Qualifies for Catch-Up Contributions?

The primary and most straightforward qualification for making catch-up contributions is age. An individual must be age 50 or older by the end of the calendar year in which they wish to make the contributions. It doesn’t matter if you turn 50 on January 1st or December 31st; as long as you reach that milestone within the year, you are eligible. Beyond the age requirement, the individual must also be participating in a retirement plan that allows such contributions. While most 401k, 403(b), governmental 457(b) plans, and the Thrift Savings Plan (TSP) do permit catch-up contributions, it’s always prudent to confirm with your specific plan administrator or HR department. Self-employed individuals contributing to solo 401k plans are also eligible for these catch-up provisions.

The Additional Annual Limit

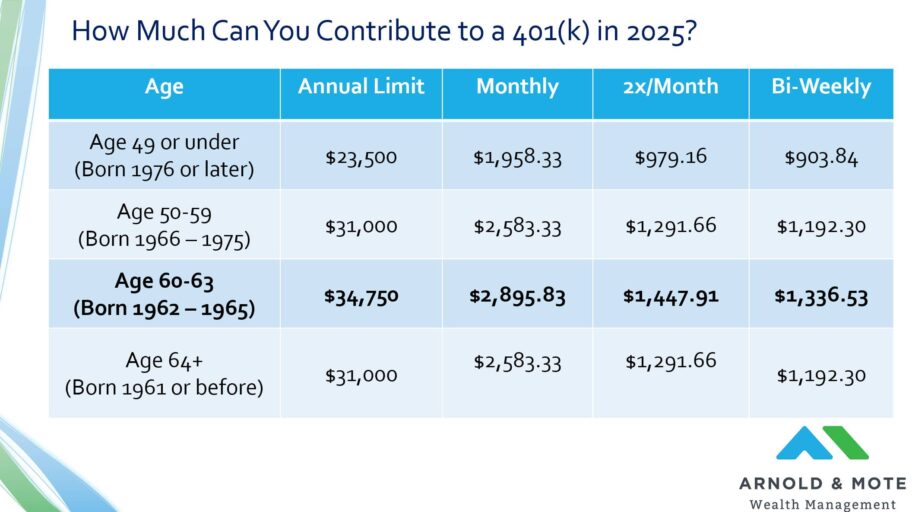

Catch-up contributions are an additional amount that can be contributed above the standard annual elective deferral limit. This amount is also set by the IRS and is subject to annual adjustments. For 2023, the catch-up contribution limit was $7,500, which increased to $7,500 again for 2024 (it remained flat). This means that in 2024, an individual aged 50 or over could contribute the standard $23,000, plus an additional $7,500, for a total of $30,500 from their own salary deferrals. This additional sum significantly boosts the potential for rapid growth in one’s retirement account during these crucial pre-retirement years.

How They Work in Practice

Implementing catch-up contributions is typically a straightforward process. If you are eligible (age 50+) and your plan allows it, you simply instruct your plan administrator or payroll department to increase your deferral rate. Your contributions will first go towards meeting the standard annual limit. Once that limit is reached, any subsequent contributions for the year will then count towards your catch-up limit, up to the maximum allowed amount. For example, if the standard limit is $23,000 and the catch-up limit is $7,500, and you decide to contribute $30,500 in a year, the first $23,000 will be treated as standard contributions, and the next $7,500 will be categorized as catch-up. This process is usually seamless from the participant’s perspective, handled automatically by the plan’s recordkeeper.

Why “Catch-Up”?

The moniker “catch-up” perfectly encapsulates the spirit of these provisions. They are designed to acknowledge and mitigate the challenges many individuals face in consistently saving for retirement throughout their careers. Life happens: job changes, periods of unemployment, raising a family, caring for elderly parents, or simply prioritizing other financial goals (like a mortgage or education expenses) can all derail early retirement savings efforts. Catch-up contributions provide a powerful mechanism for individuals to accelerate their savings trajectory in the years leading up to retirement, effectively “catching up” to their desired savings goals or making up for periods when they couldn’t contribute as much. This recognition of life’s financial realities makes catch-up contributions an equitable and highly effective feature of the U.S. retirement system.

Strategic Benefits of Maximizing Catch-Up Contributions

Leveraging 401k catch-up contributions offers a multitude of strategic advantages, particularly for those in the final stretch of their working careers. These benefits extend beyond simply accumulating more money, encompassing significant tax advantages and enhanced financial security.

Accelerating Retirement Savings

The most direct and immediate benefit of catch-up contributions is the sheer acceleration of retirement savings. By allowing individuals aged 50 and over to contribute thousands of dollars more each year, these provisions enable a substantial increase in the principal amount invested. Over even a few years, this additional capital, combined with the power of compounding returns, can lead to a significantly larger retirement nest egg. For example, contributing an extra $7,500 per year for ten years (from age 50 to 60) would add $75,000 in contributions, which could easily grow to over $100,000 or more with average market returns, making a tangible difference in one’s retirement lifestyle. This extra cushion can mean the difference between merely getting by and living comfortably in retirement.

Enhanced Tax Advantages

Catch-up contributions bring with them the same potent tax advantages as regular 401k contributions, further amplifying their appeal.

- Pre-tax contributions: When you contribute to a traditional 401k on a pre-tax basis, the amount contributed is deducted from your taxable income for that year. This means you pay less in income taxes in the present, freeing up more cash flow to save. For higher-income earners, this immediate tax deduction can be quite substantial.

- Tax-deferred growth: All earnings and growth within the 401k account accrue on a tax-deferred basis. This means you don’t pay taxes on investment gains until you withdraw the money in retirement. This compounding effect, unhindered by annual taxation, allows your money to grow much faster over time.

- Roth 401k catch-up contributions: For those who anticipate being in a higher tax bracket in retirement or prefer tax-free withdrawals, making catch-up contributions to a Roth 401k is an excellent strategy. While these contributions don’t offer an upfront tax deduction, the qualified withdrawals in retirement are entirely tax-free, including all accumulated earnings. This flexibility provides a powerful hedge against future tax rate increases.

Bridging Retirement Savings Gaps

For many people, the path to retirement savings isn’t linear. There might have been periods of lower income, career breaks to raise children or care for family, or simply a delayed start to serious retirement planning. Catch-up contributions are an ideal mechanism to address these “savings gaps.” They provide a concentrated opportunity in the later stages of one’s career to aggressively contribute and make up for previous shortfalls. This can be particularly impactful for women who may have spent time out of the workforce, or for individuals who pivoted careers later in life and are now in a position to save more aggressively. It offers a tangible way to regain confidence in one’s retirement outlook.

Compounding Power (Even Later in Life)

While the idea of compounding interest is often emphasized for young savers, its power should not be underestimated even in the years leading up to retirement. Adding an extra $7,500 annually for 10-15 years, with typical market returns, can generate significant growth. For example, contributing an additional $7,500 annually at an average 7% return for 10 years would result in over $100,000 in additional wealth. Even if you only have 5-7 years until retirement, these additional contributions provide fresh capital that can benefit from market gains, further solidifying your financial foundation and enhancing your ability to weather market fluctuations during your retirement years.

Important Considerations and How to Implement

While 401k catch-up contributions offer compelling advantages, maximizing their benefit requires careful planning and awareness of certain practicalities.

Checking Plan Eligibility

The first and most critical step is to confirm that your specific 401k plan allows catch-up contributions. While most employer-sponsored 401k, 403(b), governmental 457(b) plans, and the Thrift Savings Plan (TSP) do, it is not universally mandated. You should reach out to your HR department or plan administrator to verify this. They can provide details on how to adjust your contribution rate to include catch-up amounts and confirm your eligibility based on age. It’s also wise to understand any specific deadlines or procedures your plan might have for implementing these changes, especially if you’re approaching the end of the calendar year.

Prioritizing Contributions

While maximizing your 401k catch-up contributions is a powerful goal, it should be considered within the broader context of your overall financial strategy. Before funneling every spare dollar into your 401k, ensure you’ve addressed other pressing financial needs.

- High-interest debt: Prioritizing the payoff of high-interest credit card debt or personal loans can often yield a guaranteed “return” that surpasses typical investment gains due to the high interest rates.

- Emergency fund: A robust emergency fund (typically 3-6 months of living expenses) is non-negotiable. It provides a crucial financial safety net, preventing you from having to tap into your retirement savings for unexpected expenses.

- Employer match: Always contribute at least enough to capture any employer matching contributions offered in your 401k. This is essentially free money and represents an immediate 100% return on your investment, making it a top priority before focusing on catch-up contributions.

- Health Savings Account (HSA): If you are enrolled in a high-deductible health plan (HDHP), contributing to an HSA can offer a triple tax advantage (tax-deductible contributions, tax-free growth, tax-free withdrawals for qualified medical expenses) and can serve as an excellent supplemental retirement savings vehicle once healthcare needs are met.

A balanced approach that prioritizes these foundational elements before fully maximizing catch-up contributions is often the most financially sound strategy.

Consulting a Financial Advisor

For many, integrating catch-up contributions into a comprehensive retirement plan can benefit greatly from professional guidance. A qualified financial advisor can help you assess your current financial situation, project your retirement needs, and determine the optimal contribution strategy for your specific circumstances. They can also help you:

- Understand the interplay between your 401k, other retirement accounts (like IRAs or HSAs), and taxable investment accounts.

- Develop a strategy for asset allocation and investment choices within your 401k.

- Provide insights into tax planning, particularly concerning pre-tax vs. Roth catch-up contributions.

- Help you create a sustainable budget that allows for increased savings without compromising other financial stability.

An advisor’s expertise can be invaluable in crafting a tailored strategy that maximizes your retirement savings while minimizing potential pitfalls.

Staying Informed About Limit Changes

Contribution limits for 401k plans and catch-up contributions are not static. The IRS typically reviews and adjusts these limits annually, primarily to account for inflation. It is crucial for savers, especially those making catch-up contributions, to stay informed about these changes. Information on the updated limits is usually released by the IRS in the fall of the preceding year (e.g., limits for 2025 will be announced in late 2024). Subscribing to financial news updates, regularly checking the IRS website, or consulting with your plan administrator or financial advisor are all effective ways to ensure you’re always contributing the maximum allowable amount.

In conclusion, 401k catch-up contributions are an indispensable tool for individuals aged 50 and over looking to bolster their retirement savings. By allowing for substantial additional contributions with attractive tax benefits, they offer a powerful avenue to accelerate wealth accumulation, bridge past savings gaps, and secure a more comfortable financial future. Understanding their mechanics, strategically implementing them, and staying informed about regulatory changes are key steps toward leveraging this vital retirement planning provision to its fullest potential.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.