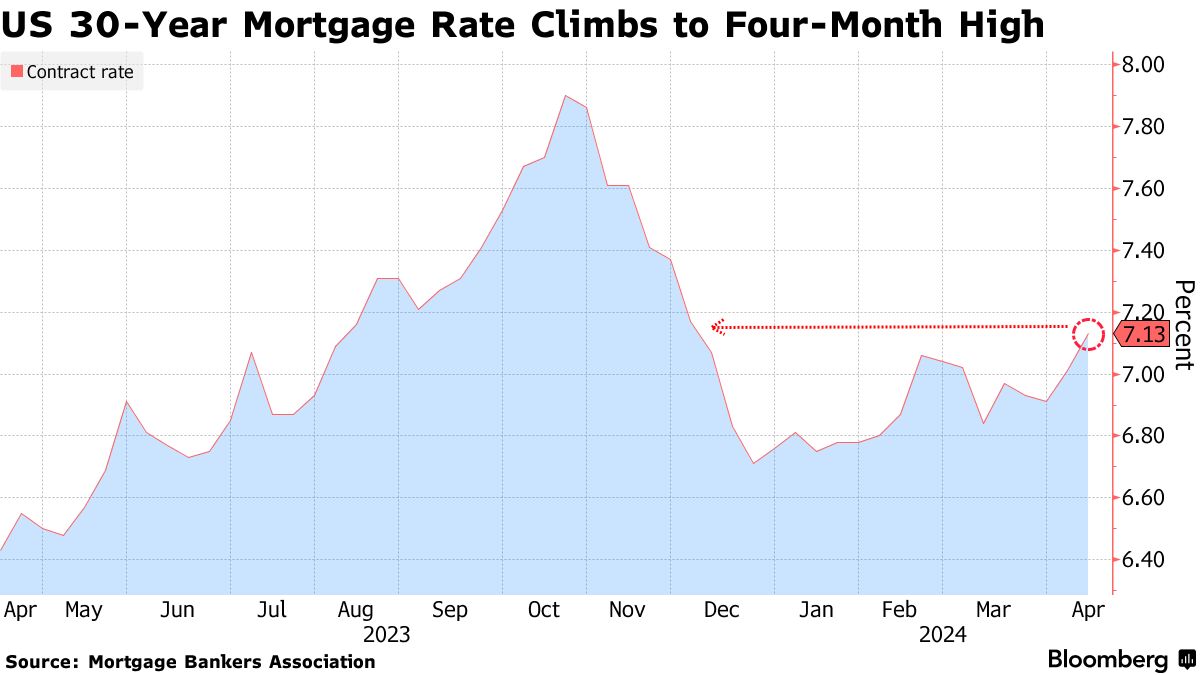

Navigating the landscape of mortgage rates can often feel like deciphering a complex financial puzzle, particularly for one of the most popular loan products: the 30-year fixed-rate mortgage. For prospective homebuyers and current homeowners looking to refinance, understanding “what are 30-year mortgage rates today” is not merely a question of curiosity but a critical step in making sound financial decisions. These rates dictate the affordability of homeownership, influence monthly budgets, and significantly impact the total cost of a home over its lifetime. In a dynamic economic environment, rates are in constant flux, shaped by a myriad of macroeconomic forces, central bank policies, and individual borrower profiles. This article delves into the current state of 30-year mortgage rates, the factors that drive their movements, how to find the most accurate figures, and strategies for securing the best possible rate in today’s market.

Understanding the 30-Year Fixed-Rate Mortgage

The 30-year fixed-rate mortgage stands as the bedrock of home financing in the United States, favored by a vast majority of homebuyers for its stability and predictable payment structure. This loan product offers a long repayment period and an interest rate that remains constant throughout the life of the loan, providing unparalleled peace of mind in an otherwise volatile financial world.

Why the 30-Year Fixed is Popular

The enduring popularity of the 30-year fixed mortgage stems from several key advantages. Firstly, the extended repayment period translates into lower monthly payments compared to shorter-term loans like a 15-year fixed mortgage. This increased affordability makes homeownership accessible to a wider demographic, allowing borrowers to manage their cash flow more effectively and allocate funds to other financial goals or necessities. For many, the lower monthly obligation is a significant factor in qualifying for a loan and fitting it comfortably within their household budget.

Secondly, the fixed nature of the interest rate is a powerful hedge against inflation and rising interest rates. Once the loan is secured, the principal and interest portion of the monthly payment never changes, regardless of market fluctuations. This predictability is a huge advantage, particularly for families planning long-term budgets, knowing that their largest monthly expense will remain consistent for three decades.

Key Characteristics and Benefits

A 30-year fixed-rate mortgage is characterized by its amortization schedule, which stretches the repayment of the loan over 360 monthly installments. In the initial years, a larger portion of each payment goes towards interest, while later payments contribute more significantly to reducing the principal balance. This structure provides flexibility, as borrowers can always choose to make additional principal payments if they wish to pay off the loan faster, without being locked into a higher mandatory payment.

The primary benefit is financial stability. Homeowners are insulated from interest rate hikes, which means their housing costs remain stable even if the Federal Reserve raises rates or if the overall economic environment becomes less favorable. This stability allows for better long-term financial planning, reduces stress, and provides a clear path to eventual debt-free homeownership.

How Fixed Rates Protect You

The protection offered by a fixed rate is invaluable. Imagine securing a 30-year mortgage at 6.5% today. If, five years from now, prevailing mortgage rates soar to 9%, your payment remains based on the original 6.5%. Conversely, if rates drop significantly, you have the option to refinance into a new, lower rate, thereby taking advantage of improved market conditions. This “win-win” scenario—protection against rising rates and the option to benefit from falling rates—is a cornerstone of its appeal. It allows homeowners to budget with certainty and navigate economic cycles with greater confidence regarding their housing expenses.

Factors Influencing Today’s Mortgage Rates

Mortgage rates do not exist in a vacuum; they are a direct reflection of a complex interplay of domestic and global economic forces. Understanding these influencing factors is crucial for anyone trying to interpret “what are 30-year mortgage rates today” and anticipate future movements.

The Federal Reserve and Monetary Policy

While the Federal Reserve does not directly set mortgage rates, its monetary policy decisions have a profound indirect impact. The Fed primarily influences short-term interest rates through the federal funds rate, which affects banks’ borrowing costs. Changes in the federal funds rate trickle down to various financial products, including the yield on U.S. Treasury bonds. Mortgage rates are closely tied to the yield on the 10-year Treasury note, as mortgage-backed securities (MBS) often track the performance of these government bonds. When the Fed signals a hawkish stance (e.g., raising rates to combat inflation), it generally pushes Treasury yields—and subsequently mortgage rates—higher. Conversely, a dovish stance (e.g., cutting rates to stimulate the economy) tends to lead to lower mortgage rates.

Inflation Expectations

Inflation is arguably one of the most significant drivers of long-term interest rates, including mortgages. Lenders need to ensure that the return on their loans outpaces the erosion of purchasing power due to inflation. If lenders anticipate higher inflation in the future, they will demand a higher interest rate on their loans to compensate for the reduced value of money they will receive back over 30 years. Therefore, strong inflation reports or expectations of future price increases almost always lead to an uptick in mortgage rates. The market reacts swiftly to economic data that suggests inflationary pressures are either growing or subsiding.

Economic Indicators (Jobs, GDP, Housing Market)

The overall health of the economy, as measured by key economic indicators, plays a critical role. A robust economy, characterized by strong job growth (low unemployment), rising Gross Domestic Product (GDP), and a resilient housing market, often leads to higher mortgage rates. A strong economy can fuel inflation and prompt the Fed to tighten monetary policy, both of which push rates up. Conversely, signs of economic weakness—such as high unemployment, contracting GDP, or a slowing housing market—often suggest a weaker demand for credit and potential disinflationary pressures, which can lead to lower mortgage rates as investors seek safer havens like government bonds.

Global Events and Market Sentiment

Geopolitical developments, international trade relations, and global economic stability can also influence domestic mortgage rates. During periods of global uncertainty or crisis, investors often flock to the relative safety of U.S. Treasury bonds, driving up demand and pushing down their yields. Since mortgage rates are tied to these yields, global instability can sometimes paradoxically lead to lower mortgage rates in the U.S. Conversely, a period of sustained global economic growth and stability might lead to higher rates as investment opportunities elsewhere become more attractive. Market sentiment, driven by news cycles and investor confidence, can also cause short-term fluctuations.

Lender-Specific Factors (Credit Score, Down Payment)

Beyond these macroeconomic factors, individual borrower characteristics significantly influence the rate offered by a specific lender. Your credit score is paramount; a higher score (typically 740+) signals lower risk to lenders, often resulting in access to the lowest available rates. A lower score indicates higher risk, leading to higher interest rates to compensate the lender. Your down payment also matters. A larger down payment (e.g., 20% or more) reduces the loan-to-value (LTV) ratio, making the loan less risky for the lender and potentially qualifying you for a better rate. Debt-to-income (DTI) ratio, loan type (e.g., FHA, VA, Conventional), and even the property’s location can also subtly impact the final rate you’re offered.

How to Find the Most Accurate Rates Today

Given the constant fluctuations and the myriad of influencing factors, identifying the most accurate 30-year mortgage rates today requires a systematic approach. Relying on a single source or a generic rate can be misleading; personalized, up-to-the-minute information is essential.

Online Mortgage Rate Comparison Tools

The internet has revolutionized the way consumers shop for financial products, and mortgages are no exception. Numerous reputable online platforms provide real-time mortgage rate data from multiple lenders. Websites like Bankrate, Zillow Mortgages, LendingTree, and Credit Karma allow you to input basic information (zip code, credit score range, down payment percentage, loan amount) and receive tailored rate quotes. These tools are excellent starting points for understanding the general range of rates available and identifying potential lenders. However, it’s important to remember that these are often “advertised” or “pre-qualified” rates and may not be the exact rate you ultimately receive without a full application.

Consulting with Mortgage Lenders and Brokers

While online tools offer a broad overview, direct engagement with mortgage professionals is indispensable for obtaining accurate, personalized quotes.

- Direct Lenders: Banks, credit unions, and dedicated mortgage companies offer their own specific rates and loan products. Contacting several of these institutions directly allows you to compare their specific offerings, understand their underwriting requirements, and negotiate terms.

- Mortgage Brokers: A mortgage broker acts as an intermediary, working with multiple lenders to find you the best possible rate and terms. They can be particularly useful for borrowers with unique financial situations or those who want to simplify the comparison shopping process. Brokers often have access to wholesale rates that may not be directly available to consumers.

When contacting lenders, be prepared to provide detailed financial information, as a true rate quote requires a soft or hard credit pull and a review of your income and assets.

Understanding APR vs. Interest Rate

When comparing mortgage offers, it’s crucial to distinguish between the interest rate and the Annual Percentage Rate (APR).

- Interest Rate: This is the percentage charged on the principal amount of the loan, used to calculate your monthly principal and interest payment.

- APR: This represents the total cost of the loan over its term, expressed as an annual percentage. It includes the interest rate plus other costs associated with the loan, such as origination fees, discount points, mortgage insurance, and other lender charges.

The APR provides a more comprehensive picture of the true cost of borrowing. When comparing offers, always look at the APR, as a lower interest rate might come with higher fees, making the overall cost (and APR) less attractive than an offer with a slightly higher interest rate but lower fees.

Gathering Personalized Quotes

The most effective strategy is to gather personalized, written quotes from at least three to five different lenders within a short timeframe (e.g., 24-48 hours). Mortgage rates can change daily, sometimes multiple times a day, so comparing quotes from different days can be misleading. Request a Loan Estimate document from each lender, which is a standardized form that clearly outlines the interest rate, APR, fees, and other terms. This allows for an “apples-to-apples” comparison and empowers you to make an informed decision based on your specific financial profile and the current market conditions.

The Impact of Current Rates on Your Homeownership Journey

The prevailing 30-year mortgage rates today have a profound and direct impact on various aspects of a homeownership journey, from initial affordability to long-term financial planning. Understanding this impact is key to making strategic decisions.

Affordability and Monthly Payments

The most immediate effect of current rates is on your monthly mortgage payment and, by extension, the overall affordability of a home. Even a seemingly small change of 0.25% or 0.50% in the interest rate can translate into significant differences in monthly payments over 30 years, especially on a large loan amount. Higher rates mean higher monthly payments for the same loan size, potentially reducing the amount of home you can afford or straining your budget. Conversely, lower rates increase your purchasing power or free up more cash flow for other expenses or savings. For instance, on a $400,000 loan, a rate of 6.5% yields a principal and interest payment of approximately $2,528, while a rate of 7.0% pushes it to $2,661—a difference of $133 per month, or nearly $48,000 over the life of the loan.

Refinancing Considerations

For existing homeowners, current 30-year mortgage rates are a primary driver for refinancing decisions. If today’s rates are significantly lower than the rate on your existing mortgage, refinancing could lead to substantial savings on monthly payments and total interest paid over the life of the loan. It could also provide an opportunity to convert an adjustable-rate mortgage (ARM) into a stable fixed rate. However, refinancing involves closing costs, so it’s essential to calculate the break-even point to determine if the savings outweigh the expenses. Conversely, if current rates are higher than your existing rate, refinancing generally isn’t advisable unless you’re looking to tap into home equity through a cash-out refinance or change loan terms for other strategic reasons.

First-Time Homebuyer Strategies

First-time homebuyers are particularly sensitive to current mortgage rates. Higher rates can make the leap into homeownership more challenging by increasing the barrier to entry through higher monthly costs. This might require them to adjust their expectations regarding home size, location, or amenities, or to save a larger down payment to reduce the loan amount. Understanding current rates also helps first-timers set realistic budgets and explore various loan programs (e.g., FHA, VA, USDA loans) which might offer more flexible qualification criteria or lower upfront costs, even if their interest rates are sometimes slightly different than conventional loans.

Market Timing and Long-Term Financial Planning

While timing the market perfectly is nearly impossible, understanding current rate trends can inform your long-term financial planning. If rates are historically low, it might be an opportune time to buy or refinance, locking in decades of savings. If rates are high, it might prompt some to postpone a purchase, save more aggressively, or consider alternative strategies like renting longer. Beyond the immediate impact, the chosen mortgage rate will influence your wealth accumulation over 30 years. Lower rates mean more of your monthly payment goes toward principal reduction and less towards interest, accelerating equity build-up and freeing up capital for other investments or retirement savings. This long-term perspective highlights why diligently seeking the best rate today is paramount.

Strategies for Securing a Favorable 30-Year Rate

Securing the most favorable 30-year mortgage rate today requires more than just passively observing market movements; it demands proactive engagement with your personal finances and the lending process. Even in a fluctuating rate environment, several key strategies can help you lock in a competitive rate.

Improving Your Credit Score

Your credit score is arguably the most influential factor in determining the interest rate you’ll be offered. Lenders use it as a primary indicator of your creditworthiness and risk. Borrowers with excellent credit scores (generally 740 and above) consistently qualify for the lowest rates. To improve your score:

- Pay bills on time: Payment history is the most significant factor.

- Reduce outstanding debt: Especially on credit cards, aim for a credit utilization ratio below 30%.

- Avoid opening new credit accounts: This can temporarily lower your score.

- Check your credit report for errors: Dispute any inaccuracies that could be negatively impacting your score.

Beginning this process months before applying for a mortgage can significantly enhance your borrowing power.

Increasing Your Down Payment

A larger down payment reduces the lender’s risk, as you have more equity in the property from day one. This often translates into a lower interest rate. A down payment of 20% or more also typically allows you to avoid private mortgage insurance (PMI), which adds to your monthly housing costs. Even if you can’t hit 20%, every additional percentage point you can put down strengthens your application and can positively influence the rate offered. Lenders view borrowers with substantial equity as more committed and less likely to default.

Shopping Around for Lenders

This cannot be stressed enough: do not settle for the first quote you receive. Mortgage rates can vary significantly between different lenders, even on the same day for the same borrower. As discussed, contact multiple banks, credit unions, and mortgage brokers. Use the Loan Estimate forms to compare offers side-by-side, focusing on the APR, total closing costs, and interest rate. Some lenders might offer slightly higher rates but with fewer fees, while others might entice with a lower rate but higher upfront costs. Diligent shopping around, particularly within a short comparison window, can save you tens of thousands of dollars over the life of your 30-year mortgage.

Considering Mortgage Points

Mortgage points, also known as discount points, are essentially prepaid interest that you pay at closing in exchange for a lower interest rate over the life of the loan. One point typically costs 1% of the loan amount and can reduce your interest rate by a certain fraction (e.g., 0.25%). This strategy is most beneficial if you plan to stay in the home for many years, allowing you to “break even” on the cost of the points and then enjoy the long-term savings from the reduced interest rate. You’ll need to calculate the break-even point (how long it takes for the monthly savings to equal the cost of the points) to determine if buying down the rate is a financially sound decision for your specific situation.

In conclusion, understanding “what are 30-year mortgage rates today” is a dynamic process that intertwines global economics with personal financial health. By staying informed about market influences, diligently shopping for the best terms, and proactively managing your credit and finances, you can position yourself to secure a favorable rate that supports your homeownership goals for decades to come.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.