Navigating the complex world of home financing can often feel overwhelming, with a myriad of options, terms, and fluctuating rates. Among the choices available, the 15-year fixed-rate mortgage stands out as a powerful tool for homeowners seeking to pay off their debt faster and save significantly on interest over the long run. While the 30-year fixed-rate mortgage remains the most popular choice due to its lower monthly payments, the 15-year option offers distinct advantages for those who can manage the higher immediate financial commitment. Understanding “what are 15-year mortgage rates” involves not just looking at the numerical percentage but also grasping the mechanics behind this loan type, its benefits, its challenges, and the broader economic factors that influence its ebb and flow. This article delves deep into the intricacies of 15-year mortgage rates, providing a professional and insightful guide for prospective and current homeowners.

Understanding the Mechanics of 15-Year Mortgages

A mortgage is essentially a loan used to purchase or maintain a home, land, or other types of real estate. The borrower agrees to pay the lender over a set period, typically 15 or 30 years, in exchange for the funds. A 15-year mortgage, as its name suggests, is amortized over a decade and a half, leading to a significantly different repayment structure compared to its longer-term counterparts.

How a 15-Year Mortgage Differs from a 30-Year Mortgage

The fundamental difference between a 15-year and a 30-year mortgage lies in their amortization schedules – how the loan principal and interest are paid down over time. With a 15-year mortgage, the principal amount is divided into fewer payments, meaning each monthly payment will be substantially higher. However, because the loan term is halved, you spend less time paying interest. This leads to a dramatic reduction in the total amount of interest paid over the life of the loan. For example, on a $300,000 loan at a 7% interest rate, a 30-year mortgage might accrue over $400,000 in interest, whereas a 15-year mortgage at a slightly lower rate (say, 6.5%) might accrue less than $170,000 in interest. The difference is staggering, translating into hundreds of thousands of dollars in savings.

The Role of Interest Rates

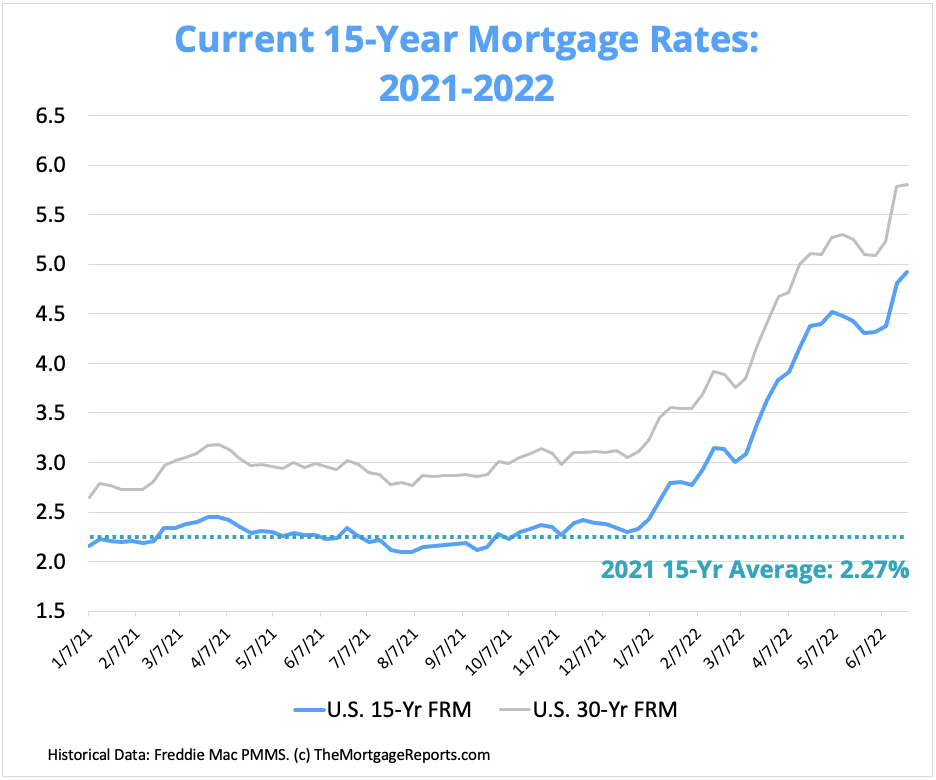

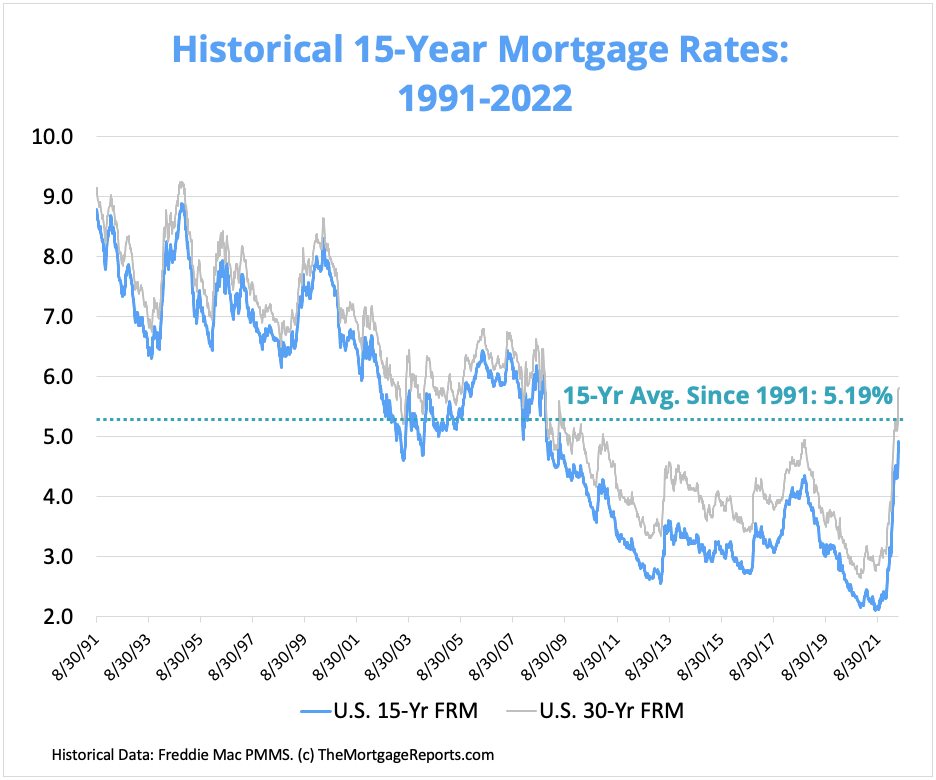

Interest rates are the cost of borrowing money, expressed as a percentage of the loan amount. For a 15-year mortgage, these rates are typically fixed, meaning they remain constant for the entire 15-year term. This provides stability and predictability to your monthly payments, insulating you from market fluctuations. Mortgage rates are influenced by a complex interplay of economic factors, including inflation, the Federal Reserve’s monetary policy, bond market performance (particularly the 10-year Treasury yield), and the overall health of the housing market. Lenders also factor in individual borrower characteristics such as credit score, debt-to-income ratio, and loan-to-value ratio when determining the specific rate offered. Generally, 15-year mortgage rates tend to be slightly lower than 30-year rates because the lender’s risk is perceived to be lower over a shorter period.

Principal vs. Interest: Accelerating Equity Growth

In any amortizing loan, each monthly payment consists of both principal and interest. Early in the loan term, a larger portion of your payment goes towards interest. As the loan matures, more of each payment is allocated to the principal. With a 15-year mortgage, this shift happens much more rapidly. Because your monthly payments are higher, you pay down the principal balance at an accelerated rate from the very beginning. This swift reduction in the principal means you build equity in your home much faster. Equity is the portion of your home that you truly own, calculated as your home’s market value minus the outstanding mortgage balance. Rapid equity growth not only provides financial security but also gives you more financial flexibility down the line, potentially allowing you to tap into that equity through a home equity loan or line of credit if needed.

The Benefits of Opting for a 15-Year Mortgage

Choosing a 15-year mortgage isn’t just about faster repayment; it unlocks a host of financial advantages that can significantly impact your long-term wealth and peace of mind.

Significant Interest Savings

As highlighted earlier, the most compelling benefit of a 15-year mortgage is the colossal savings on interest. By compressing the repayment period, you drastically reduce the total amount of interest paid over the life of the loan. This can amount to hundreds of thousands of dollars saved, depending on the loan amount and interest rate. These savings aren’t just theoretical; they are real dollars that remain in your pocket, available for other investments, retirement savings, or simply enhancing your quality of life. The compounding effect of paying less interest over a shorter period is a powerful wealth-building mechanism.

Faster Equity Build-Up

Beyond interest savings, the accelerated principal reduction translates directly into faster equity build-up. Owning a larger share of your home sooner means your net worth grows more rapidly. This increased equity serves as a substantial financial asset, providing a buffer against economic downturns and potentially allowing you to leverage it for future financial goals, such as funding a child’s education, starting a business, or investing in other assets. Should you decide to sell your home, a higher equity stake means a larger profit (assuming market conditions are favorable).

Long-Term Financial Security

Imagine being completely mortgage-free by the time you’re in your 40s or 50s. For many, this is a dream scenario that a 15-year mortgage can make a reality. Being free of one of life’s largest monthly expenses significantly reduces financial stress and offers unparalleled security, especially as you approach retirement. With no mortgage payments, your fixed expenses decrease dramatically, freeing up substantial cash flow for retirement savings, travel, or simply enjoying your later years without the burden of housing debt. This early financial liberation can redefine your retirement planning.

Potential for Lower Interest Rates

Another appealing aspect is that 15-year fixed mortgage rates are almost always lower than 30-year fixed rates. Lenders view shorter loan terms as less risky because there’s less time for economic conditions to change adversely, and the borrower demonstrates a stronger financial position by committing to higher monthly payments. While the difference might seem small—often a quarter to half a percentage point—this seemingly minor reduction can compound into significant interest savings over the loan’s life, further enhancing the financial benefits of this mortgage type.

The Challenges and Considerations

While the benefits of a 15-year mortgage are substantial, it’s not a suitable option for everyone. It comes with its own set of challenges and requires careful financial planning.

Higher Monthly Payments

The most significant hurdle for many borrowers is the higher monthly payment. To pay off the same principal amount in half the time, each installment must be considerably larger. This can put a strain on monthly budgets, especially for those who are already stretching to afford a home. Before committing to a 15-year term, it’s crucial to perform a thorough budget analysis to ensure that these higher payments are comfortably affordable without compromising other essential expenses or savings goals.

Impact on Cash Flow and Financial Flexibility

Committing to a higher monthly mortgage payment inevitably impacts your cash flow. Less disposable income means less flexibility for other financial endeavors, such as investing in the stock market, saving for emergencies, or funding discretionary spending. While paying off your mortgage faster is a laudable goal, it shouldn’t come at the expense of building an emergency fund (typically 3-6 months of living expenses) or contributing to retirement accounts. A balanced approach is key. If the higher payment severely restricts your ability to save or invest elsewhere, a 30-year mortgage with extra principal payments might be a more flexible strategy.

Qualification Requirements

Due to the larger monthly payments, lenders often impose stricter qualification requirements for 15-year mortgages. Borrowers typically need a higher income, a lower debt-to-income (DTI) ratio, and a stronger credit score to demonstrate their ability to consistently meet the more demanding payment schedule. If your financial profile is borderline, you might qualify for a 30-year mortgage but not a 15-year one. It’s essential to understand that while 15-year rates are lower, the total cost of ownership per month is higher.

Opportunity Cost

Choosing to put more money towards your mortgage principal each month also means those funds are not available for other investments. This is known as opportunity cost. In certain economic environments, investing extra cash in the stock market or other assets might yield a higher return than the interest rate you’re saving on your mortgage. For financially savvy individuals, this means weighing the guaranteed savings from a lower mortgage interest rate against the potential (but not guaranteed) higher returns from other investments. This is a personal financial decision that often depends on risk tolerance and overall financial strategy.

Factors Influencing 15-Year Mortgage Rates Today

Mortgage rates are dynamic, fluctuating in response to a complex interplay of global and domestic economic forces. Understanding these factors is crucial for anyone trying to gauge “what are 15-year mortgage rates” at any given moment.

Economic Indicators

Broader economic indicators play a significant role. Strong economic growth, low unemployment, and rising inflation typically push interest rates higher as lenders anticipate a greater return on their money and to combat the eroding power of inflation. Conversely, signs of a weakening economy often lead to lower rates as the Federal Reserve might cut rates to stimulate growth, and investors seek safer assets like bonds.

Federal Reserve Policy

While the Federal Reserve does not directly set mortgage rates, its monetary policy decisions have a profound indirect impact. When the Fed raises or lowers the federal funds rate, it influences the cost of borrowing for banks, which then passes those costs on to consumers in various forms, including mortgage rates. The Fed’s rhetoric and actions on quantitative easing or tightening also ripple through the financial markets, affecting bond yields and, consequently, mortgage rates.

Bond Market Performance

Mortgage rates are closely tied to the bond market, particularly the yield on the 10-year Treasury note. Mortgage-backed securities (MBS), which are packaged loans bought and sold by investors, compete with U.S. Treasury bonds. When Treasury yields rise, MBS yields usually follow suit to remain competitive, leading to higher mortgage rates. Changes in investor demand for these securities, driven by economic outlooks and risk perceptions, can cause daily fluctuations in mortgage rates.

Lender-Specific Factors

Beyond macroeconomic forces, individual lenders apply their own criteria to determine the rate offered to a specific borrower. Your personal credit score, debt-to-income ratio, loan-to-value (LTV) ratio (the amount you borrow compared to the home’s value), and even the loan amount itself can influence the final rate you receive. A higher credit score and a larger down payment generally translate into a lower, more favorable interest rate, as they signify lower risk to the lender.

Is a 15-Year Mortgage Right for You?

Deciding whether a 15-year mortgage is the right financial move requires a thorough assessment of your personal financial situation and long-term goals. It’s not a one-size-fits-all solution.

Assessing Your Financial Health

The primary question revolves around your ability to comfortably afford the higher monthly payments. Do you have a stable income, ideally with room for growth? Have you built a robust emergency fund that can cover unexpected expenses without jeopardizing your mortgage payments? Do you have significant high-interest debts that should be prioritized before taking on a larger mortgage payment? A solid financial foundation is paramount. Your income stability, existing debt load, and savings buffer are critical indicators of your readiness for this commitment.

Long-Term Financial Goals

Consider your broader financial aspirations. Is early mortgage payoff a top priority for you, perhaps linked to retirement planning or a desire for complete financial independence? Or are you focused on maximizing investment returns elsewhere, even if it means carrying mortgage debt longer? For those who prioritize debt elimination and a secure, debt-free retirement, the 15-year mortgage aligns perfectly with these goals.

Comparing with Other Options

It’s always wise to compare the 15-year option against other mortgage types, particularly the 30-year fixed. While the 30-year has lower monthly payments, you’ll pay significantly more in interest over time. However, the flexibility of lower payments might allow you to invest the difference, potentially yielding greater returns if managed wisely. Another option is a 30-year mortgage with the intention of making extra principal payments to accelerate payoff without the rigid commitment of a 15-year term. This hybrid approach offers flexibility, allowing you to scale back extra payments in lean months.

The Power of Refinancing

For current homeowners with a 30-year mortgage, refinancing into a 15-year term can be a highly effective strategy. If your income has increased, or interest rates have dropped since you originally purchased your home, refinancing can unlock substantial interest savings and shorten your payoff period. However, refinancing involves closing costs, so it’s essential to calculate the break-even point to ensure the savings outweigh the upfront expenses.

In conclusion, “what are 15-year mortgage rates” is more than just a number; it represents a strategic financial decision with profound implications for your long-term wealth and stability. While it demands a higher monthly commitment, the benefits of significant interest savings, rapid equity growth, and eventual financial freedom make it an incredibly attractive option for financially stable individuals. Before making a decision, carefully weigh the pros and cons, assess your financial health, and consider consulting with a qualified financial advisor to ensure the 15-year mortgage aligns perfectly with your unique financial circumstances and aspirations.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.