In the complex world of personal finance, few acronyms carry as much weight—or cause as much confusion—as APR, or Annual Percentage Rate. Whether you are applying for your first credit card, financing a new vehicle, or navigating the labyrinth of a thirty-year mortgage, the APR is the single most important number you need to understand. It is the “true” price tag of money. While many consumers fixate on the “interest rate,” the APR provides a more holistic view of what a loan actually costs, incorporating fees and other charges that lenders might otherwise obscure.

Understanding APR is not just about academic curiosity; it is a vital skill for financial literacy. In an era of fluctuating inflation and aggressive lending marketing, being able to decipher the APR allows you to compare financial products on an apples-to-apples basis. This guide explores the mechanics of APR, its various applications in the financial markets, and how you can leverage this knowledge to optimize your personal balance sheet.

Decoding the Mechanics: What is APR and How Does it Work?

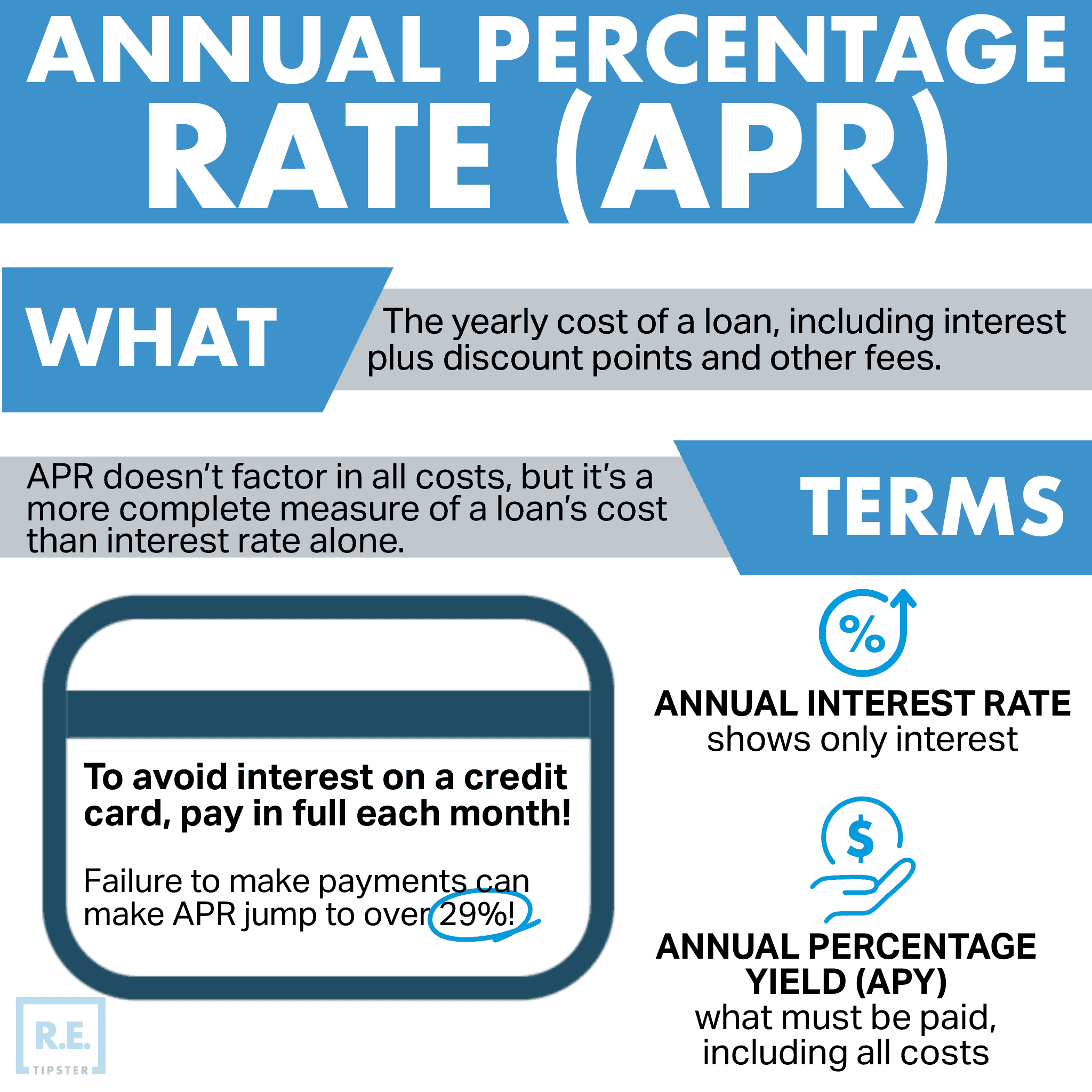

At its most basic level, the Annual Percentage Rate represents the yearly cost of borrowing funds, expressed as a percentage. However, the nuance lies in what is included beyond the base interest.

The Critical Difference Between Interest Rate and APR

It is a common mistake to use “interest rate” and “APR” interchangeably. The interest rate is the percentage of the principal amount charged by the lender for the use of its money. The APR, conversely, is the interest rate plus any additional costs associated with the transaction. These costs can include loan origination fees, mortgage broker fees, private mortgage insurance (PMI), and closing costs.

For example, if you take out a $200,000 mortgage with a 6% interest rate but pay $5,000 in closing fees, your APR will be higher than 6%. This is because the APR reflects the total finance charge relative to the actual amount of credit you received.

How APR is Calculated

Lenders calculate APR by taking the total interest paid over the life of the loan, adding the additional fees, and then averaging that cost over the loan term to produce an annual percentage. The formula generally involves dividing the total finance charges by the loan amount, then dividing by the number of days in the loan term, multiplying by 365, and finally multiplying by 100 to get the percentage. Because this math can get complex, federal law requires lenders to disclose the APR clearly before any contract is signed.

Nominal vs. Effective APR

In the world of investing and high-interest debt, you may also encounter “Effective APR” (often referred to as EAR or Effective Annual Rate). While the nominal APR usually reflects simple interest over a year, the effective rate accounts for the power of intra-year compounding. If a credit card compounds interest daily—which most do—the effective rate you pay is actually slightly higher than the stated APR. Understanding this distinction is crucial for high-balance borrowers who want to avoid the “interest-on-interest” trap.

The Various Faces of APR in Personal Finance

APR is not a monolithic figure; it behaves differently depending on the financial instrument involved. From revolving credit to installment loans, the implications of the rate vary significantly.

Credit Card APRs: A Multitude of Rates

If you look at your credit card statement, you will notice that there isn’t just one APR. Most cards utilize a tiered system:

- Purchase APR: The rate applied to standard transactions.

- Cash Advance APR: Usually significantly higher than the purchase rate, this applies when you withdraw cash using your card.

- Penalty APR: If you miss payments, the lender may hike your rate to 29.99% or higher.

- Introductory APR: A promotional rate (often 0%) designed to attract new customers for a set period.

Because credit cards are revolving debt, the APR is used to calculate your “Daily Periodic Rate.” By dividing your APR by 365, the bank determines how much interest to charge you every single day on your average daily balance.

Mortgage and Auto Loan APRs

In installment loans like mortgages and auto financing, the APR serves as a safeguard for the consumer. Because these loans often involve “points” (prepaid interest) or hefty administrative fees, the APR reveals the true cost of the loan. A mortgage with a 5.5% interest rate and 2 points might actually be more expensive than a 5.75% mortgage with zero points. The APR allows you to see that 5.5% rate is actually a 5.9% APR, making the 5.75% option the smarter financial move.

Fixed vs. Variable APRs

Loans and credit cards also fall into two structural categories. A Fixed APR remains constant throughout the life of the loan or a specific period, providing predictability for your monthly budget. A Variable APR is tied to an index, such as the U.S. Prime Rate. When the Federal Reserve raises or lowers benchmark interest rates, your variable APR will follow suit. This makes variable-rate products riskier in a rising-interest-rate environment.

Why APR is the Ultimate Comparison Tool

The primary utility of the APR is its ability to strip away marketing jargon and reveal the raw economic reality of a financial offer.

Cutting Through Marketing Smoke and Mirrors

Lenders often advertise “low-interest rates” in bold fonts while burying high origination fees in the fine print. By focusing on the APR, you bypass the distraction of the nominal interest rate. If Lender A offers a 4% rate with $4,000 in fees and Lender B offers a 4.2% rate with $500 in fees, the APR will quickly show you that Lender B is offering the more cost-effective deal for most loan terms.

Evaluating the Impact of Loan Terms

APR also helps you understand how the length of a loan affects your cost. On a shorter-term loan, such as a 3-year auto loan, the impact of upfront fees on the APR is much higher than on a 6-year loan. This is because those fixed costs are being “spread out” over fewer payments. Using the APR to compare different terms ensures you aren’t overpaying for the “convenience” of a specific loan duration.

Compounding Frequency and Your Bottom Line

While APR is a standard annual measure, the frequency of compounding (monthly, daily, or quarterly) affects how much you actually pay. A 15% APR compounded daily results in more interest paid than a 15% APR compounded annually. Savvy financial actors look for lenders that compound less frequently or, better yet, use the grace period of credit cards to avoid APR-based charges entirely by paying the statement balance in full every month.

Strategies to Lower Your APR and Save Money

Knowing what APR is is the first step; the second step is actively managing it to reduce your cost of capital.

Improving Your Credit Score

The APR you are offered is a direct reflection of your perceived risk as a borrower. Those with credit scores in the “Exceptional” range (800+) will often receive APRs that are several percentage points lower than those in the “Fair” range. By maintaining a low credit utilization ratio, paying bills on time, and monitoring your credit report for errors, you can qualify for lower APRs, potentially saving tens of thousands of dollars over the life of a mortgage or auto loan.

The Power of Negotiation and Refinancing

Many consumers don’t realize that APRs—especially on credit cards—can be negotiable. If you have been a loyal customer and your credit score has improved, a simple phone call to your issuer can sometimes result in a permanent APR reduction. Similarly, in a declining interest rate environment, refinancing high-APR debt into a lower-APR loan (such as a personal loan or a new mortgage) is a cornerstone of effective wealth management.

Utilizing 0% Intro APR Periods Effectively

One of the most powerful tools in the “Money” niche is the 0% Intro APR balance transfer card. This allows you to move high-interest debt to a new card where you pay no interest for 12 to 21 months. However, the “catch” is often a balance transfer fee (usually 3% to 5%). To determine if this is a good deal, you must calculate the “effective cost” of that fee and ensure you can pay off the balance before the introductory period ends and the standard, high APR kicks in.

Regulatory Oversight and Consumer Protection

Because the math behind lending can be easily manipulated to disadvantage the borrower, various legal frameworks exist to ensure transparency regarding APR.

The Truth in Lending Act (TILA)

In the United States, the Truth in Lending Act of 1968 was a landmark piece of legislation. it requires lenders to provide a written disclosure of the APR and the total finance charge before the consumer becomes obligated on the loan. This standardized the way APR is calculated across the industry, preventing lenders from using proprietary formulas to make their loans appear cheaper than they are.

Reading the Schumer Box

For credit card consumers, the “Schumer Box” is your best friend. Named after Senator Charles Schumer, this is the standardized table included in credit card agreements. It clearly lists the APRs for purchases, transfers, and cash advances, as well as the fees. Before signing up for any new line of credit, reviewing the Schumer Box is an essential step in due diligence.

Conclusion: Mastering the Math of Money

In conclusion, the Annual Percentage Rate is more than just a number on a page; it is the fundamental metric of borrowing. By understanding that the APR incorporates interest and fees, distinguishing between fixed and variable rates, and utilizing the APR to compare lenders, you position yourself as a sophisticated participant in the financial system.

The goal of personal finance is to maximize the value of your assets while minimizing the cost of your liabilities. By mastering the nuances of APR, you gain the clarity needed to avoid predatory lending, reduce unnecessary expenses, and ultimately accelerate your journey toward financial independence. Whether you are buying a home or managing a credit card, always ask: “What is the APR?” The answer will tell you exactly how much your financial choices are costing you.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.