Deciding when to start drawing Social Security benefits is one of the most critical financial decisions you will make in your lifetime. For many Americans, Social Security represents a significant portion of their retirement “three-legged stool,” alongside personal savings and employer-sponsored pensions. However, unlike a fixed savings account, Social Security is a dynamic benefit; the age at which you choose to click the “apply” button can result in a permanent difference of hundreds, or even thousands, of dollars in monthly income.

While the earliest age to claim is 62 and the latest age to see benefit increases is 70, the “right” age is not a one-size-fits-all answer. It requires a deep dive into your personal health, your financial bridge to retirement, and the complex rules set by the Social Security Administration (SSA). This guide explores the mechanics of claiming ages, the financial implications of your timing, and the strategic considerations for long-term wealth preservation.

Understanding the Mechanics: Full Retirement Age and Benefit Adjustments

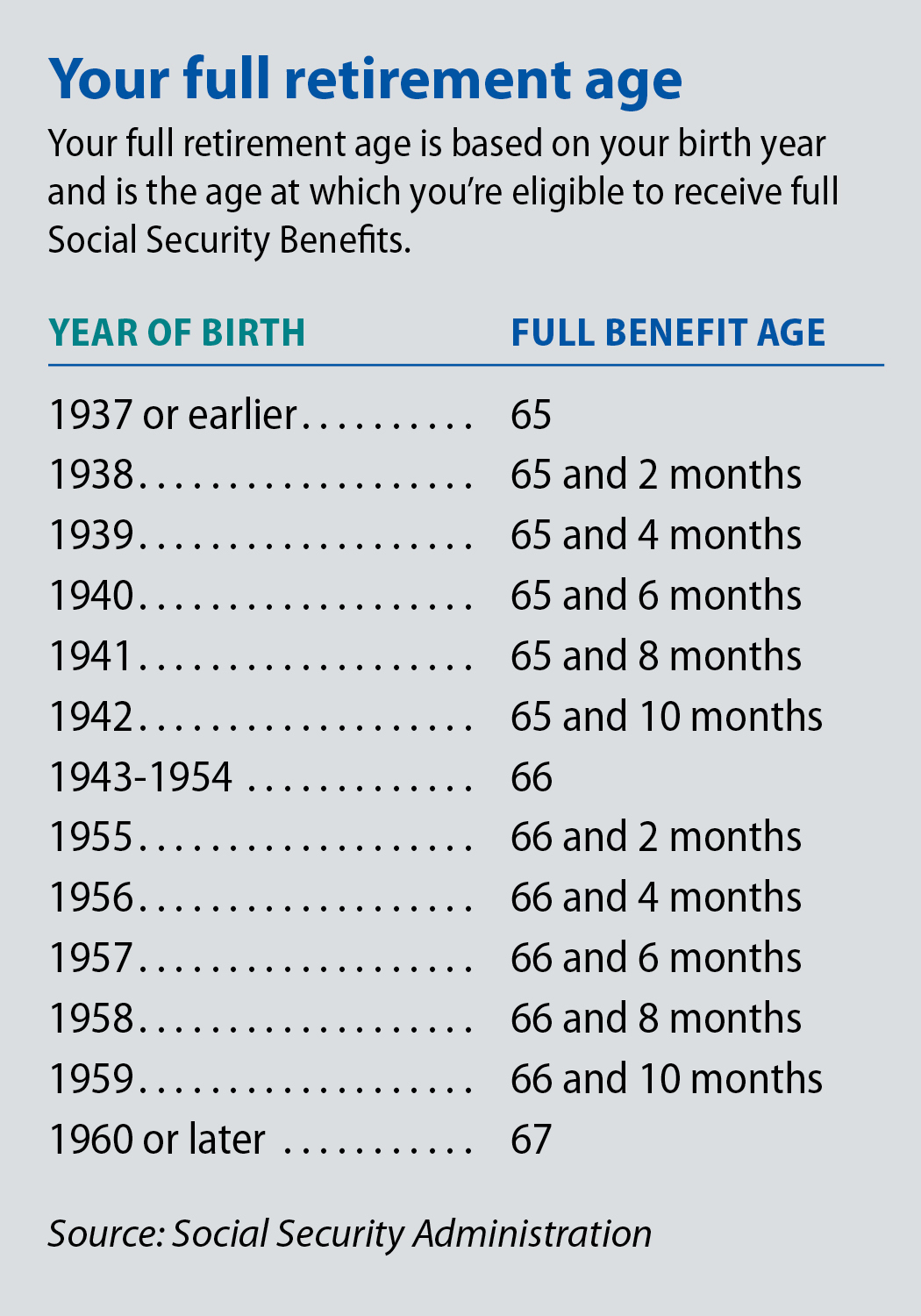

To determine the best age to draw Social Security, you must first identify your Full Retirement Age (FRA). This is the age at which you are entitled to 100% of your primary insurance amount (PIA), which is calculated based on your 35 highest-earning years.

How Birth Year Determines Your FRA

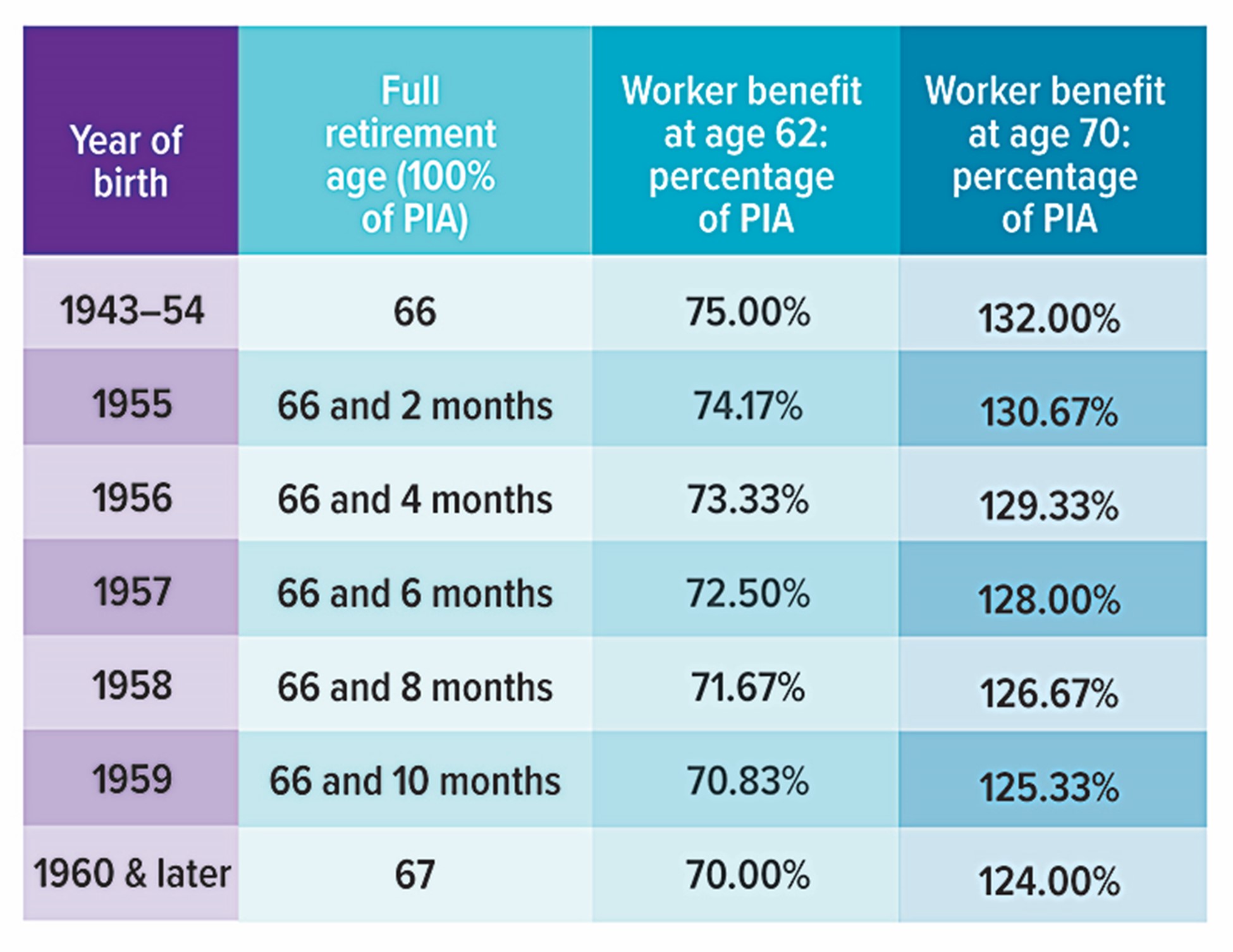

For decades, the FRA was 65. However, due to changes in legislation aimed at ensuring the program’s long-term solvency, the FRA has gradually increased. If you were born between 1943 and 1954, your FRA is 66. If you were born in 1960 or later, your FRA is 67. For those born between 1955 and 1959, the FRA increases in two-month increments for every year. Understanding your specific FRA is the benchmark against which all “early” or “delayed” filing penalties and credits are measured.

The Financial Cost of Filing Early

You can begin drawing benefits as early as age 62, but there is a steep price for doing so. If your FRA is 67 and you claim at 62, your monthly benefit is permanently reduced by 30%. This reduction is calculated monthly: the SSA reduces the benefit by 5/9 of 1% for each month before the FRA, up to 36 months, and then 5/12 of 1% for each additional month. While receiving a check five years early provides immediate liquidity, it significantly lowers your “inflation floor” for the rest of your life.

The Reward for Delayed Retirement Credits

Conversely, for every month you delay claiming past your FRA up until age 70, you earn “Delayed Retirement Credits.” This amounts to an 8% simple interest increase per year. If your FRA is 67 and you wait until age 70, you will receive 124% of your base benefit. This is essentially a guaranteed, government-backed return on your “investment” of waiting—a rate of return that is nearly impossible to find in low-risk financial markets today.

Personal Finance Factors Influencing Your Timing

The mathematical “break-even” point—the age at which the total value of higher monthly payments exceeds the total value of more numerous, smaller payments—is typically between ages 78 and 82. However, personal finance is about more than just a spreadsheet; it is about your specific life circumstances.

Assessing Your Health and Longevity

If you have reason to believe your life expectancy is lower than average due to health issues or family history, claiming early (at 62 or FRA) often makes the most financial sense. You want to maximize the “cumulative lifetime benefit.” On the other hand, if you are in excellent health and have a family history of living into your 90s, delaying until age 70 acts as a form of “longevity insurance,” ensuring that you do not outlive your assets in your final, most expensive years of life.

Cash Flow Needs and the “Retirement Bridge”

Can you afford to wait? This is the most practical question. If you are retired and your 401(k) or IRA balances are insufficient to cover your cost of living, you may be forced to draw Social Security early to avoid high-interest debt. However, savvy investors often use a “retirement bridge” strategy. This involves spending down a portion of their taxable brokerage accounts or traditional IRAs between ages 62 and 70 to allow their Social Security benefit to grow. Because the 8% annual increase in Social Security is guaranteed, it is often more beneficial to draw from a volatile stock market account than to lock in a lower Social Security check.

The Social Security Earnings Test

If you plan to continue working while drawing benefits before you reach your FRA, you must be aware of the “Earnings Test.” For 2024, if you are under FRA, the SSA deducts $1 from your benefits for every $2 you earn above $22,320. While these withheld benefits are eventually added back to your check once you reach FRA, the immediate reduction can disrupt your cash flow and tax planning. Once you hit your FRA, you can earn an unlimited amount of income without any reduction in your Social Security checks.

Strategic Considerations for Couples and Dependents

In a household, the decision of when to draw Social Security should not be made in a vacuum. Spousal and survivor benefits add a layer of complexity that can drastically change the optimal claiming age for the primary earner.

Maximizing the Survivor Benefit

For married couples, the most important consideration is often the survivor benefit. When one spouse passes away, the surviving spouse stops receiving their own benefit and starts receiving the larger of the two benefits the couple was receiving. Therefore, it is often strategically wise for the higher-earning spouse to delay until age 70. This ensures that even after the first spouse dies, the survivor is left with the highest possible monthly payment for the remainder of their life.

Understanding Spousal Benefits

A spouse who has not worked or has a low earnings history can receive a spousal benefit of up to 50% of the worker’s FRA amount. However, you cannot claim a spousal benefit until the primary worker has filed for their own benefit. This creates a coordination challenge: the primary earner may want to delay to age 70 to increase their own benefit, but doing so might delay the lower-earning spouse’s ability to collect a spousal benefit. Balancing these two needs requires a projection of the couple’s total household income over a 30-year retirement horizon.

Tax Implications and Long-Term Wealth Management

One often overlooked aspect of drawing Social Security is how it interacts with the rest of your taxable income. Social Security benefits are not always tax-free; in fact, for many retirees, they can trigger a “tax torpedo.”

Is Your Social Security Taxable?

The IRS uses a metric called “Combined Income” to determine if your benefits are taxable. Combined Income is your Adjusted Gross Income (AGI) + non-taxable interest + half of your Social Security benefits. If this total exceeds $34,000 for individuals or $44,000 for joint filers, up to 85% of your Social Security benefits may be subject to federal income tax.

Managing the Withdrawal Hierarchy

To minimize the tax impact, investors must be strategic about which accounts they tap into first. If you draw Social Security at 62 while also taking Required Minimum Distributions (RMDs) from a traditional IRA later at 73, you could find yourself in a much higher tax bracket than anticipated. By delaying Social Security and performing Roth conversions in the early years of retirement, you can reduce the size of your future RMDs and potentially lower the percentage of your Social Security that is subject to taxation.

Conclusion: Finding Your “Sweet Spot”

There is no universal “perfect age” to draw Social Security, but there is a perfect age for your specific financial plan. If you value immediate liquidity and have concerns about longevity, age 62 or 65 may be appropriate. If you are looking to maximize your guaranteed, inflation-adjusted income and protect a surviving spouse, waiting until age 70 is frequently the superior financial move.

Ultimately, the decision should be based on a comprehensive review of your net worth, your anticipated expenses, and your tax strategy. Social Security is more than a monthly check; it is a flexible tool that, when used correctly, provides a foundation of financial security that allows your other investments to grow and sustain you throughout your golden years. Consult with a financial advisor to run “what-if” scenarios, ensuring that when you finally decide to draw, you are doing so with the confidence that you have maximized your lifetime wealth.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.