In the landscape of modern economics, few demographic groups have been as scrutinized, misunderstood, and eventually as influential as the Millennials. Often defined by their unique relationship with technology and their arrival into adulthood during a period of global economic upheaval, this generation is now entering its peak earning years. To understand the financial trajectory of the current global market, one must first accurately define what age group the Millennials are and explore the specific fiscal pressures and opportunities that define their lives.

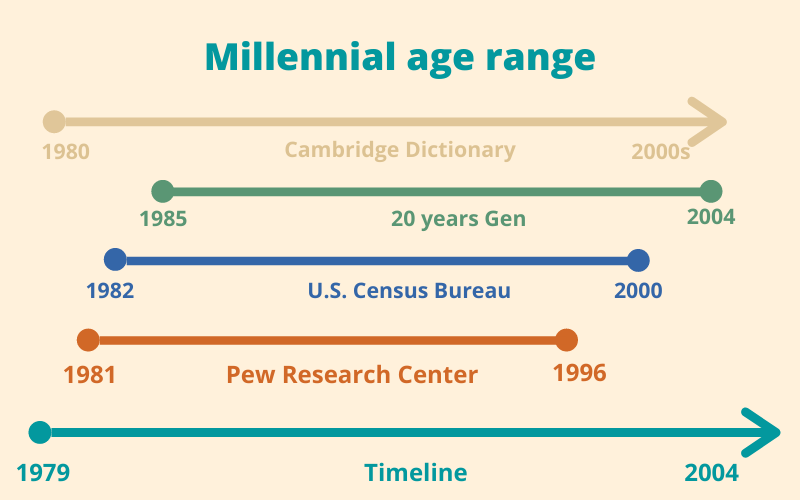

As of 2024, the Millennial generation—also known as Generation Y—is generally defined by the Pew Research Center as those born between 1981 and 1996. This means the cohort currently spans the ages of 28 to 43. This is a critical demographic “sweet spot” for the financial sector; they are no longer the “young kids” of the workforce. Instead, they are the primary drivers of the housing market, the innovators of the gig economy, and the architects of a new, digital-first approach to personal finance.

Defining the Millennial Generation in the Modern Financial Landscape

The birth years of 1981 to 1996 are not merely arbitrary markers. In the world of finance and economics, these years represent a specific set of circumstances that shaped a generation’s view of money, risk, and stability. Millennials are the first “bridge” generation—those who remember a world before the internet but who reached maturity just as the digital revolution became absolute.

The 1981–1996 Timeline: Why These Years Matter for Money

Those born in the early 1980s entered the workforce during the post-9/11 recession or the early 2000s expansion, while the younger end of the spectrum graduated college directly into the teeth of the 2008 Great Recession. This disparity within the group is significant. The “Elder Millennials” had a few years to build home equity before the 2008 crash, whereas “Younger Millennials” faced a stagnant job market and predatory lending environments from the start. This shared exposure to systemic financial fragility has resulted in a generation that is simultaneously more cautious and more open to disruptive financial technologies than their predecessors.

From Recession to Recovery: A Financial Identity Forged in Crisis

The 2008 financial crisis serves as the defining economic event for the Millennial age group. While Baby Boomers saw their retirement accounts dip and Gen X saw their home values plummet, Millennials saw their entry-level opportunities vanish. This created a “scarring effect” on their lifetime earnings. Understanding that the age group currently between 28 and 43 has survived two “once-in-a-lifetime” economic downturns (2008 and the 2020 pandemic) is essential for any financial analysis. It explains their skepticism toward traditional banking institutions and their pivot toward alternative income streams.

The Wealth Gap and the Millennial Financial Reality

Despite their reputation in popular media for spending on ephemeral luxuries, the financial reality of the Millennial age group is dominated by significant structural hurdles. As they navigate their 30s and early 40s, the primary focus has shifted from survival to wealth accumulation, though the path is markedly different from the one taken by Generation X or the Baby Boomers.

Student Debt: The Anchor of a Generation

Perhaps the most significant financial characteristic of the Millennial age group is the burden of education costs. This cohort was told that a university degree was the only path to stability, leading to a massive spike in student loan utilization. Currently, Millennials hold a disproportionate share of the $1.7 trillion in U.S. student loan debt. This “anchor” has delayed traditional milestones. For many in this age bracket, the monthly “mortgage-sized” student loan payment has prevented early entry into the stock market or the purchase of a first home, leading to a slower start in the race for compound interest.

The Delayed Milestones: Real Estate and Marriage

In previous generations, the 28-to-43 age range was the “golden era” for homeownership and family expansion. For Millennials, these milestones have been pushed back by nearly a decade. High debt-to-income ratios, combined with a housing market characterized by low inventory and institutional investors, have forced many Millennials to remain renters longer than they intended. However, as the oldest Millennials move into their mid-40s, we are seeing a surge in “first-time” home buying, albeit at much higher price points. This delay has significant implications for how they manage liquidity and how they view real estate as an investment asset versus a primary residence.

Millennial Investment Strategies and the Shift in Asset Allocation

Millennials have fundamentally changed the way the world invests. Being the first generation to have smartphones integrated into their financial lives, they have moved away from traditional brokerage models in favor of “low-friction” platforms. This shift isn’t just about the tools they use; it’s about a fundamental change in philosophy.

Fintech and the Democratization of Investing

The age group born between 1981 and 1996 is responsible for the explosion of the Fintech sector. From commission-free trading apps to “robo-advisors” that automate diversified portfolios, Millennials prefer algorithmic transparency over the opaque fees of traditional wealth management. This generation has also shown a high affinity for fractional shares, allowing them to invest in high-priced stocks (like Amazon or Alphabet) with as little as five dollars. This democratization has allowed even those burdened by student debt to begin building a portfolio, breaking the “all or nothing” barrier to entry that existed in the 1990s.

Sustainable and ESG Investing: The Values-Driven Portfolio

For Millennials, money is often seen as an extension of their personal values. This has led to the rise of ESG (Environmental, Social, and Governance) investing. Unlike their parents, who often prioritized pure ROI (Return on Investment), a significant portion of the Millennial age group is willing to accept slightly lower returns—or at least higher volatility—if it means their capital is not supporting fossil fuels or unethical labor practices. This shift is forcing corporations to change their financial reporting and operational strategies to attract Millennial capital, which is increasingly becoming the dominant force in the market.

The Great Wealth Transfer: Preparing for the $68 Trillion Shift

While the current financial picture for Millennials may seem fraught with debt and delayed milestones, an unprecedented economic shift is on the horizon. Over the next two decades, it is estimated that approximately $68 trillion will be passed down from Baby Boomers to their Millennial heirs. This “Great Wealth Transfer” will likely be the largest movement of assets in human history.

Inheriting the Future: Estate Planning and Asset Management

As the 1981–1996 cohort begins to inherit this wealth, the financial services industry is undergoing a radical transformation. Millennials do not interact with money the same way their parents did. They are less likely to keep their inheritance in a traditional brick-and-mortar bank and more likely to move it into digital assets, diversified ETFs, or venture capital. Financial planning for this age group now requires a sophisticated understanding of tax mitigation, estate law, and the integration of digital assets like cryptocurrency into a traditional portfolio.

Transitioning from Accumulation to Preservation

As the oldest Millennials turn 43, their focus is shifting from “how do I make money?” to “how do I protect what I have?” We are seeing a rise in Millennial interest in life insurance as an investment vehicle, the use of trusts for generational wealth, and a more conservative approach to the “side hustle.” The “gig economy” which once served as a primary income source for many in their 20s is now being leveraged by 40-year-olds as a way to diversify income streams and hedge against corporate instability.

Conclusion

The question “what age group are the millennials” is the starting point for a much deeper conversation about the future of the global economy. Spanning from 28 to 43, this generation is at a pivotal crossroads. They have been shaped by the digital age and tempered by economic crises, resulting in a demographic that is financially resilient, technologically savvy, and deeply skeptical of traditional structures.

As they move further into their peak earning years and begin to receive the largest wealth transfer in history, their influence on personal finance, investment trends, and the global markets will only intensify. For the modern financial professional or the individual investor, understanding the nuances of the Millennial “Money Identity” is no longer optional—it is the key to navigating the economic landscape of the 21st century. Whether it is through the adoption of Fintech, the prioritization of ESG, or the total reimagining of the “retirement” ideal, Millennials are not just participating in the economy; they are rewriting its rules for the next generation.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.