For decades, the “magic number” for retirees was 70½. This was the age when the Internal Revenue Service (IRS) shifted from being a silent partner in your retirement savings to an active participant, requiring you to begin withdrawing funds from your tax-deferred accounts. However, recent legislative overhauls—specifically the SECURE Act and the SECURE 2.0 Act—have fundamentally altered the retirement landscape.

Understanding what age RMDs (Required Minimum Distributions) are required is no longer a simple matter of looking at a single number. It requires an understanding of your birth year, the type of accounts you hold, and the evolving tax laws that govern American retirement. Navigating these rules is critical, as failure to comply results in some of the steepest penalties in the federal tax code.

Understanding the Landscape of Required Minimum Distributions (RMDs)

At its core, a Required Minimum Distribution is the minimum amount you must withdraw from your retirement accounts each year. These rules apply to employer-sponsored retirement plans, such as 401(k) and 403(b) plans, as well as traditional IRAs and IRA-based plans like SEPs and SIMPLE IRAs.

What is an RMD?

The RMD is not a suggestion; it is a mandate. During your working years, the government allows you to contribute to traditional retirement accounts “pre-tax,” meaning you deduct the contributions from your taxable income. The investments then grow tax-deferred for decades. The RMD is the IRS’s way of ensuring that they eventually collect the deferred income tax on that money. Once you reach a certain age, the government requires you to start bringing that money back into your annual income, where it is taxed at your ordinary income tax rate.

Why Does the IRS Require Them?

The philosophy behind RMDs is rooted in the tax-deferred nature of retirement vehicles. These accounts are designed to provide income during your retirement years, not to serve as perpetual tax-free wealth transfer vehicles for heirs. By forcing distributions, the IRS ensures that the tax benefits provided during the accumulation phase are eventually balanced by tax revenue during the distribution phase.

The Evolution of RMD Ages: From 70½ to 75

The most significant source of confusion for retirees today is the shifting age requirement. In a span of just a few years, the age at which RMDs must begin has moved twice, thanks to bipartisan legislation aimed at helping Americans save longer as life expectancies increase.

The SECURE Act of 2019

Prior to 2020, the RMD age was 70½. This fractional age caused significant confusion for taxpayers and financial planners alike. The Setting Every Community Up for Retirement Enhancement (SECURE) Act of 2019 simplified this by moving the RMD age to 72 for anyone who had not reached age 70½ by the end of 2019. This change provided retirees with an extra year and a half of tax-deferred growth, reflecting the reality that many Americans are working longer.

The SECURE 2.0 Act of 2022

In late 2022, Congress passed the SECURE 2.0 Act, which further extended the RMD age. This legislation recognized that with rising inflation and longer lifespans, many retirees benefit from keeping their assets invested longer. The act created a staggered increase based on the individual’s date of birth.

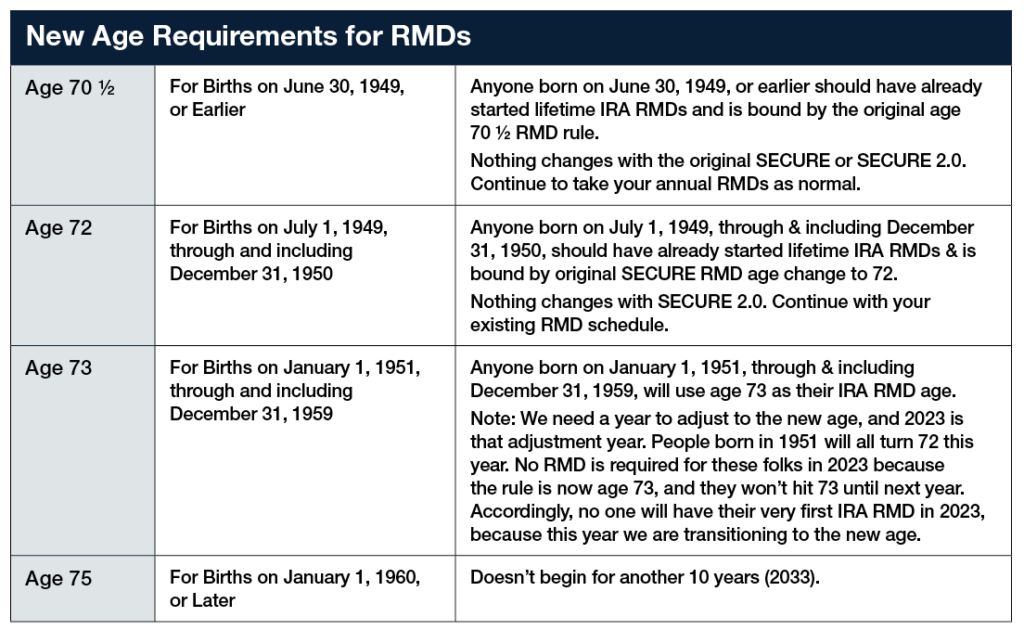

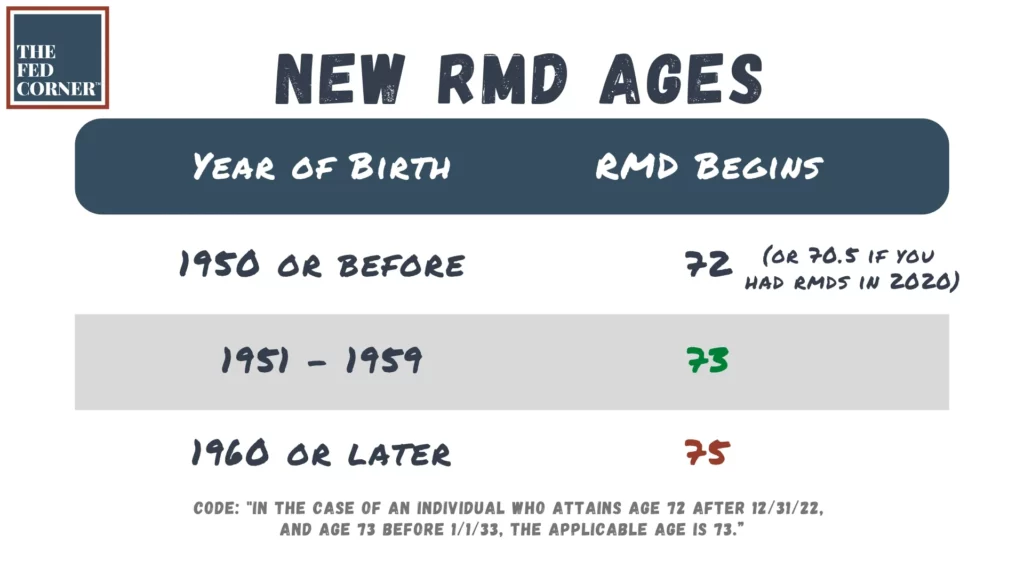

Current Age Requirements for 2024 and Beyond

To determine your specific RMD age, you must look at your birth year:

- If you were born before July 1, 1949: Your RMD age was 70½.

- If you were born between July 1, 1949, and December 31, 1950: Your RMD age was 72.

- If you were born between 1951 and 1959: Your RMD age is 73.

- If you were born in 1960 or later: Your RMD age is 75.

For the majority of people currently approaching retirement, 73 is the operative number. However, those in their early 60s should prepare for the shift to age 75, which will take effect as they approach their distribution window in the coming decade.

Calculating Your Distribution and Managing the Mechanics

Knowing the age is only half the battle; the second half is calculating how much you must actually withdraw. The amount is not a flat percentage; it is a variable figure that changes every year based on your account balance and your statistical life expectancy.

How the IRS Determines Your Payout

The IRS provides “Life Expectancy Tables” to help taxpayers calculate their RMDs. The most commonly used table is the Uniform Lifetime Table. To calculate your RMD for a given year, you take the fair market value of your retirement accounts as of December 31 of the previous year and divide it by the “distribution period” (a number representing life expectancy) that corresponds to your age in the current year.

As you get older, the divisor decreases, which means the percentage of the account you must withdraw increases. For example, at age 73, the divisor is 26.5. If you have $1,000,000 in your IRA, your RMD would be roughly $37,735. By age 90, the divisor drops to 12.2, requiring a much larger percentage of the remaining balance to be withdrawn.

Deadlines You Cannot Afford to Miss

Generally, you must take your RMD by December 31 each year. However, there is a one-time exception for your “First RMD.” You are permitted to delay your very first distribution until April 1 of the year following the year you reach the required age.

Caution is advised here: If you delay your first RMD until April 1, you will still be required to take your second RMD by December 31 of that same year. This results in two taxable distributions in a single calendar year, which can potentially push you into a higher tax bracket and increase your Medicare premiums (due to IRMAA surcharges).

Exceptions to the Rule (The “Still Working” Exception)

There is a notable exception for those who are still employed past the RMD age. If you are still working and do not own more than 5% of the company you work for, you may be able to delay RMDs from your current employer’s 401(k) or 403(b) until you actually retire. Note that this exception typically does not apply to traditional IRAs or retirement plans from previous employers.

Strategic Financial Planning to Mitigate Tax Burdens

RMDs can be a significant tax burden, especially for those who do not need the extra income to cover their living expenses. Because RMDs are taxed as ordinary income, they can impact your Social Security taxation and your overall financial efficiency. Strategic planning can help mitigate these effects.

Qualified Charitable Distributions (QCDs)

For the charitably inclined, the QCD is one of the most powerful tools in the tax code. If you are 70½ or older, you can transfer up to $105,000 (indexed for inflation) directly from your IRA to a qualified 501(c)(3) charity. This transfer counts toward your RMD for the year but is excluded from your adjusted gross income (AGI). By using a QCD, you satisfy your RMD requirement without increasing your taxable income, which can help keep you in a lower tax bracket.

Roth Conversions: The Long-Term Play

Roth IRAs do not have RMDs for the original owner. One of the most effective ways to reduce future RMD burdens is to perform “Roth conversions” in the years leading up to your RMD age. By moving money from a traditional IRA to a Roth IRA, you pay the taxes now (ideally during years when your income is lower) in exchange for tax-free growth and no mandatory withdrawals later. This strategy requires careful analysis of your current versus future tax brackets.

Beneficiary RMDs: The 10-Year Rule

The SECURE Act also changed the rules for those who inherit retirement accounts. Most non-spouse beneficiaries are now required to fully distribute the inherited account within 10 years of the original owner’s death. This “10-year rule” has eliminated the “Stretch IRA” for many, forcing heirs to take large distributions during their own peak earning years, often leading to a significant tax hit.

Penalties and Compliance: Protecting Your Nest Egg

The IRS is very strict about RMD compliance. Because these distributions represent deferred tax revenue, the government does not take kindly to delays.

The Cost of Non-Compliance

Historically, the penalty for failing to take an RMD was a staggering 50% of the amount that should have been withdrawn. SECURE 2.0 reduced this penalty, but it remains substantial. The current penalty is 25% of the RMD amount not taken. However, if the error is corrected in a timely manner (usually within two years), the penalty may be further reduced to 10%.

How to Correct a Missed RMD

If you realize you have missed a distribution, the best course of action is to take the distribution immediately and file IRS Form 5329. In many cases, if the mistake was due to a “reasonable error” and you are taking steps to remedy it, you can request a waiver of the penalty. Professional tax advice is highly recommended in these scenarios to ensure the waiver request is phrased correctly to the IRS.

Conclusion

The question of “what age are RMDs required” is the starting point for a complex journey through retirement tax planning. Whether your number is 73 or 75, the key is to look at your retirement accounts not just as a pool of savings, but as a future tax obligation that must be managed. By understanding the timing, the math, and the strategic options like QCDs and Roth conversions, you can ensure that you meet your legal obligations while keeping as much of your hard-earned wealth as possible. Retirement is about freedom, and a well-executed RMD strategy is essential to maintaining that financial freedom in your later years.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.