In the vast and often confusing landscape of personal finance, understanding the intricacies of credit cards is paramount. For many, the Annual Percentage Rate (APR) stands out as one of the most significant, yet frequently misunderstood, factors. A “good” APR credit card isn’t just about finding the lowest number; it’s about aligning that rate with your spending habits, repayment discipline, and overarching financial goals. This article delves deep into what APR truly signifies, its profound impact on your financial well-being, how to identify and secure favorable rates, and the critical balance between APR and other card features. By the end, you’ll be equipped with the knowledge to make informed decisions that safeguard and enhance your financial health.

Understanding APR: Beyond the Headline Number

The Annual Percentage Rate (APR) is the cost of borrowing money on your credit card, expressed as a yearly rate. It’s a critical metric, but its simplicity on the surface often belies a complex underlying structure. To genuinely understand what constitutes a “good” APR, one must first grasp its fundamental mechanics.

What is APR and How Is It Calculated?

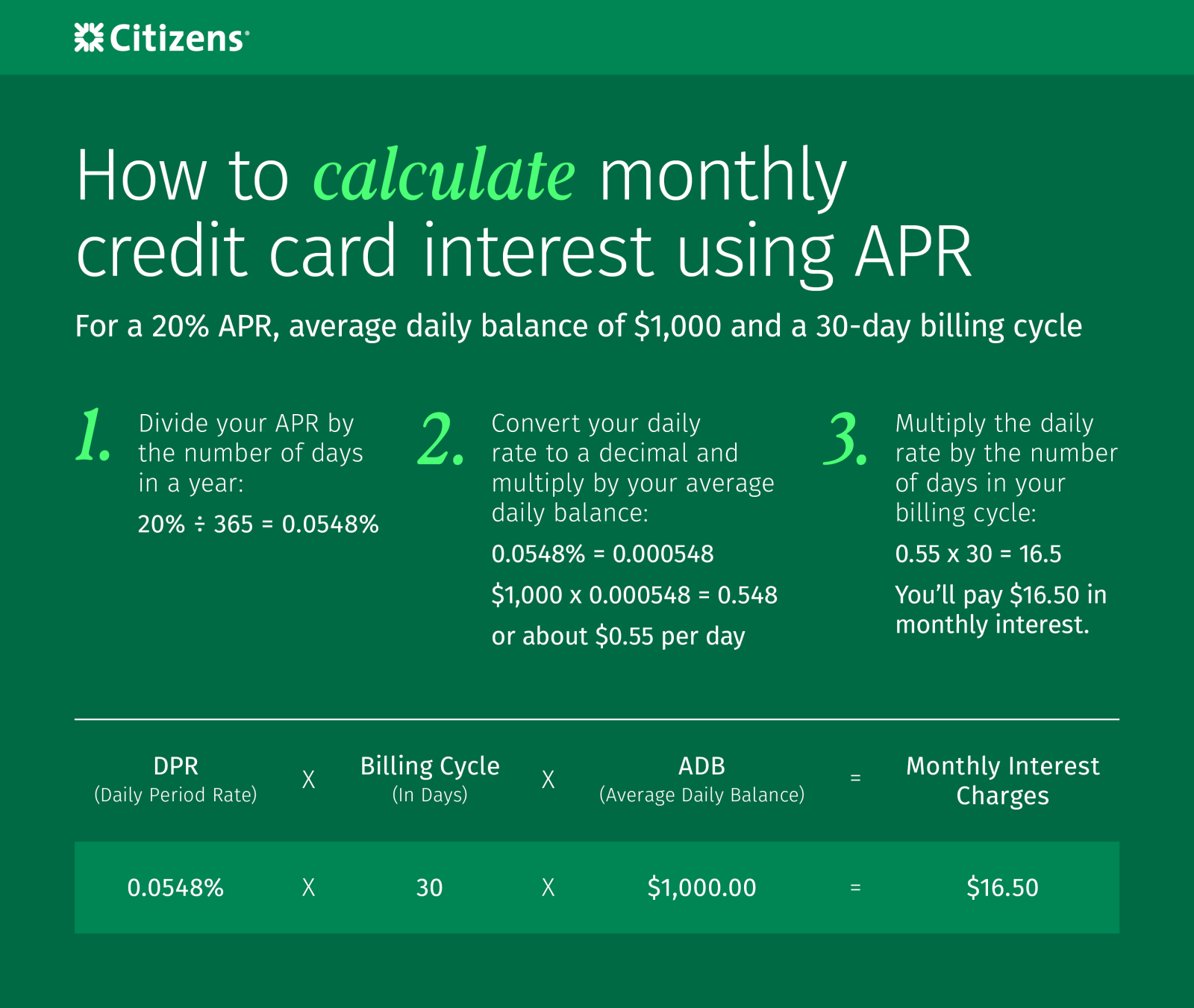

At its core, APR represents the interest rate you’re charged on outstanding balances. However, credit card interest isn’t typically calculated just once a year. Instead, it’s usually applied daily or monthly, based on your “daily periodic rate.” This daily periodic rate is derived by dividing your APR by 365 (or 360 in some cases). For example, if your APR is 18%, your daily periodic rate would be 0.0493%. This rate is then applied to your average daily balance. The compounding effect means that interest can accrue on previously accumulated interest, making understanding these calculations crucial, especially if you carry a balance. A “good” APR essentially minimizes this daily cost, reducing the financial burden of carrying debt.

Different Types of APRs

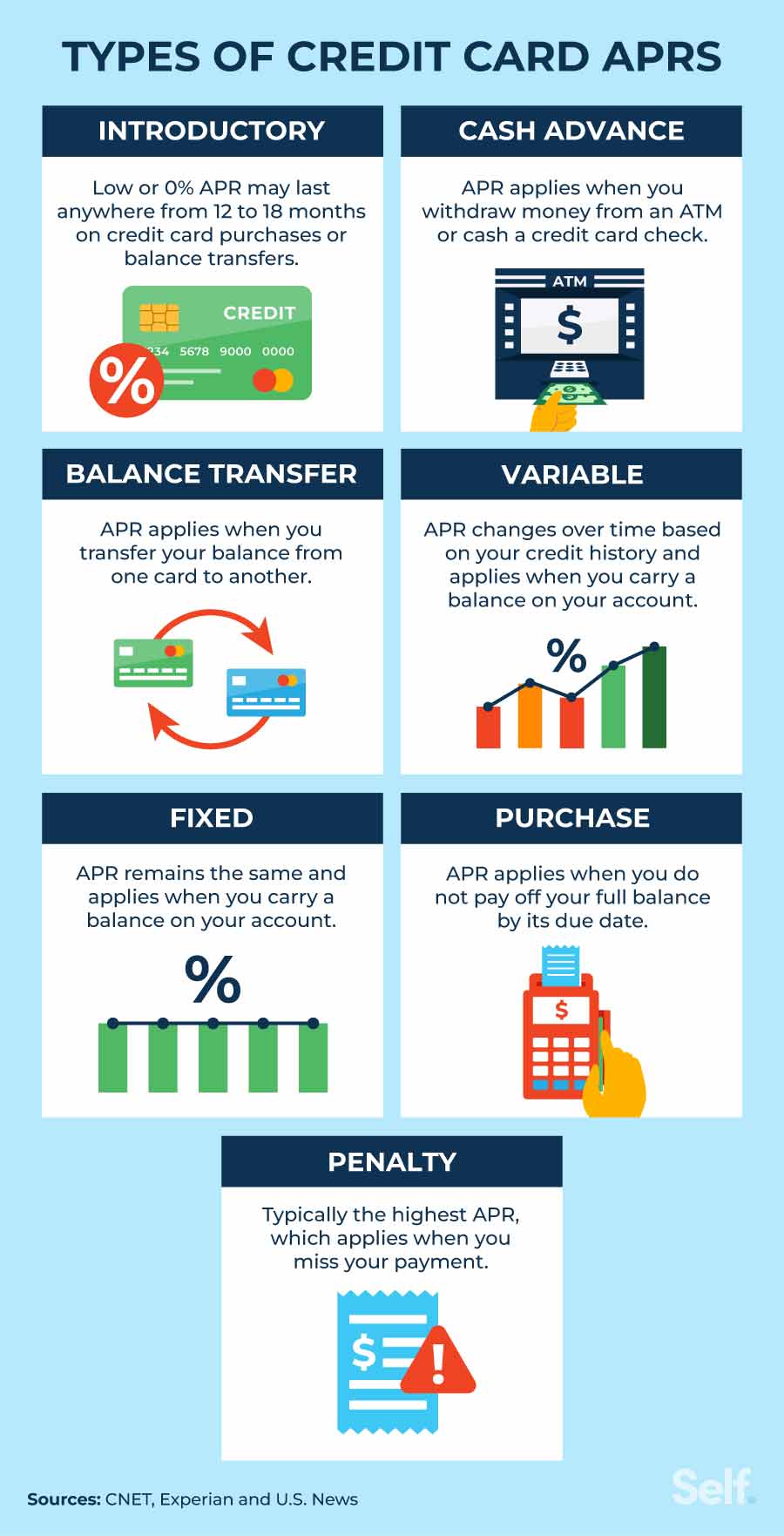

It’s a common misconception that a credit card has a single, universal APR. In reality, credit cards often feature several different APRs, each applicable to specific types of transactions:

- Purchase APR: This is the most common APR, applied to new purchases if you don’t pay your statement balance in full by the due date.

- Balance Transfer APR: This rate applies to balances you transfer from other credit cards to consolidate debt. It’s often lower than the purchase APR, sometimes even 0% for an introductory period, but typically comes with a balance transfer fee.

- Cash Advance APR: This is almost always the highest APR and starts accruing immediately, with no grace period. It’s applied when you withdraw cash using your credit card, and it often comes with a cash advance fee.

- Penalty APR: If you violate the cardholder agreement, such as making a late payment or exceeding your credit limit, your issuer may impose a penalty APR. This rate is significantly higher and can remain in effect for a considerable period, making it a critical one to avoid.

Understanding these distinctions is vital because a card might have a low purchase APR but an exorbitant cash advance APR, fundamentally altering how “good” the overall rate truly is depending on your usage patterns.

Introductory APRs and Their Lure

Many credit cards attract new customers with introductory APRs, often marketed as “0% APR for 12, 18, or even 24 months.” These offers can be incredibly beneficial, allowing you to pay down large purchases or consolidate high-interest debt without accruing interest during the promotional period. However, it’s crucial to read the fine print. Once the introductory period expires, the APR typically reverts to a much higher variable rate, known as the “go-to” rate, which is usually tied to a benchmark like the prime rate plus a margin. If you haven’t paid off your balance by then, you could suddenly face significant interest charges. A “good” introductory APR strategy involves a clear plan to pay down the balance before the promotional period ends, maximizing the savings.

The Impact of APR on Your Credit Card Debt

The APR on your credit card isn’t just a number; it’s a powerful force that can either accelerate your journey to financial freedom or trap you in a cycle of escalating debt. Its impact is most profoundly felt when you carry a balance, making a lower APR a critical tool for prudent financial management.

How High APRs Amplify Debt

When you don’t pay your credit card balance in full each month, the outstanding amount begins to accrue interest at your card’s APR. A high APR means that a larger portion of your minimum monthly payment goes towards interest rather than reducing the principal balance. This dynamic can be incredibly insidious. For instance, a $5,000 balance at a 24% APR will generate significantly more interest over time than the same balance at 12%. This phenomenon, known as the “minimum payment trap,” means that even if you consistently make your minimum payments, your debt can grow or barely shrink, extending the repayment period dramatically and costing you thousands in interest over the life of the loan. High APRs essentially make every purchase you don’t pay off immediately exponentially more expensive.

The Benefit of Low APRs

Conversely, a low APR credit card offers substantial benefits, particularly if you anticipate carrying a balance for any reason. The most obvious advantage is saving money on interest charges. With a lower interest rate, more of your minimum payment is allocated to the principal, allowing you to pay down your debt faster. This accelerates your path to debt freedom, reduces the total amount you pay for purchased goods and services, and frees up funds that would otherwise be consumed by interest for other financial goals like savings or investments. For individuals managing existing debt, consolidating it onto a lower APR card can drastically cut repayment time and overall costs, making the prospect of becoming debt-free a more achievable reality.

When APR Matters Most

It’s important to recognize that the significance of APR varies depending on your credit card habits. For cardholders who consistently pay their statement balance in full every month, the purchase APR is largely irrelevant. Because they pay within the grace period (the time between the end of a billing cycle and the payment due date, during which no interest is charged on new purchases), they effectively utilize their credit card as a convenient payment tool without incurring interest. For these individuals, rewards programs, annual fees, and cardholder benefits often take precedence over APR.

However, for anyone who carries a balance, even occasionally, APR becomes the single most critical factor. Whether it’s due to an emergency, a large purchase, or simply fluctuating income, carrying a balance means you will incur interest charges. In these scenarios, a “good” APR—meaning a low one—can save you hundreds or even thousands of dollars over time, making it the primary determinant of the card’s financial utility. Understanding your own spending and repayment patterns is key to determining how much weight to place on APR when selecting a credit card.

Identifying and Securing a “Good” APR Credit Card

Defining a “good” APR isn’t a one-size-fits-all endeavor. What’s considered good depends heavily on your personal financial profile and market conditions. However, understanding the factors that influence APR and knowing how to position yourself for favorable rates is universally beneficial.

Factors Influencing Your APR

Credit card issuers assess your creditworthiness to determine the APR they offer. Several key factors come into play:

- Credit Score: This is perhaps the most significant determinant. Individuals with excellent credit scores (typically FICO scores above 740-760) are perceived as lower risk and therefore qualify for the lowest advertised APRs. As your score decreases, the risk perception increases, leading to higher APRs.

- Credit History: Lenders look at the length of your credit history, the types of credit accounts you have, and your payment track record. A long history of responsible credit use, characterized by on-time payments and low credit utilization, signals reliability and can help you secure better rates.

- Income and Debt-to-Income Ratio: While not always explicitly stated, your income level and your existing debt burden relative to your income can influence a lender’s risk assessment and, consequently, the APR offered.

- Market Conditions: The prime rate, set by the Federal Reserve, serves as a benchmark for many variable APRs. When the prime rate rises, credit card APRs tend to follow suit.

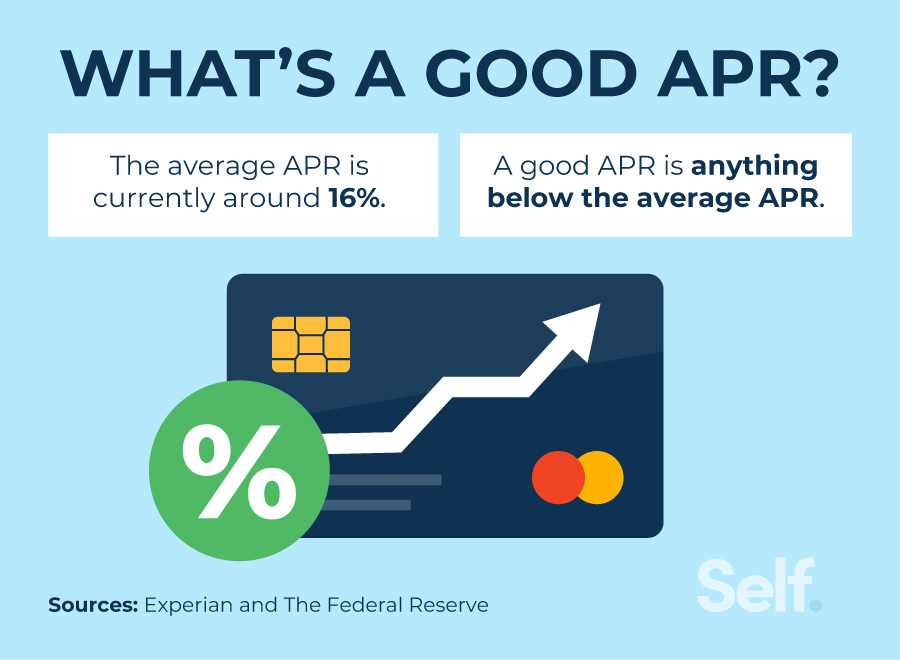

What Constitutes a “Good” APR?

Given the variable nature, what’s a “good” APR? For excellent credit, anything in the low to mid-teens (e.g., 12%–16%) can be considered excellent, especially for general purchase APRs. For those with good credit, rates in the 16%–20% range are typical. If your credit is fair or average, you might see APRs ranging from 20% to 25% or even higher. Intro 0% APR offers, lasting 12 months or more, are almost always considered “good” if used strategically. It’s crucial to compare offers not just against what’s broadly available, but against what you personally qualify for, based on your credit profile. Always consider the highest potential APR you might receive if it’s advertised as a range.

Strategies to Qualify for Lower APRs

If your current APRs are high or you’re looking to apply for a new card with a better rate, there are actionable steps you can take:

- Improve Your Credit Score: This is the most effective long-term strategy. Pay bills on time, keep credit utilization low (ideally below 30% of your available credit), and avoid opening too many new accounts simultaneously. Regularly check your credit report for errors.

- Reduce Existing Debt: A lower debt-to-income ratio signals greater financial stability to lenders. Focus on paying down existing loans and credit card balances.

- Build a Diverse Credit Mix: Having a mix of credit (e.g., a credit card, an auto loan, a mortgage) can demonstrate responsible management of various credit types.

- Negotiate with Your Current Issuer: If you’ve been a long-time customer with a good payment history, call your credit card company and ask for a lower APR. They may be willing to reduce it to retain your business, especially if you have competing offers.

Beyond APR: Other Crucial Credit Card Features

While APR is undeniably critical, especially if you carry a balance, focusing solely on this single metric can lead to overlooking other valuable features that significantly impact the overall cost and utility of a credit card. A truly “good” credit card offers a holistic package that aligns with your financial habits and objectives.

Annual Fees vs. APR

Many premium credit cards come with annual fees, which can range from under $100 to several hundred dollars. It’s a common misconception that annual fees are inherently bad. In reality, a card with an annual fee might be a “good” deal even if its APR is slightly higher than a no-fee card, provided its benefits outweigh the cost. For example, a card with a $95 annual fee might offer robust travel rewards, statement credits for specific purchases (like airline fees or streaming services), travel insurance, or extended warranties that more than compensate for the fee. If you’re a high spender, a frequent traveler, or can fully leverage the perks, the net value might be positive. However, if you rarely use the benefits or carry a balance where the APR cost dwarfs the perks, a no-annual-fee card with a competitive APR would be a better choice.

Rewards Programs

Rewards programs – encompassing cash back, points, and travel miles – are a major draw for credit cards. For consumers who pay their balances in full each month, effectively avoiding APR charges, rewards become the primary incentive. A “good” rewards card maximizes the return on your spending. This could be a flat-rate cash back card (e.g., 1.5% or 2% on all purchases), a tiered rewards card offering higher percentages in specific categories (e.g., 5% on groceries or gas), or a travel card with lucrative mileage bonuses. The value of these rewards should be weighed against any annual fees and, if you occasionally carry a balance, against the card’s APR. A card with an amazing rewards rate but a sky-high APR might be a poor choice if you’re not consistently paying in full, as the interest charges will quickly erase any rewards earned.

Balance Transfer Offers

For individuals grappling with high-interest credit card debt, a balance transfer offer can be a lifesaver. These offers typically provide a low or 0% introductory APR on transferred balances for a set period. While not a permanent solution, they offer a crucial window to pay down debt principal without the burden of interest. A “good” balance transfer card often comes with a reasonable balance transfer fee (usually 3-5% of the transferred amount) and a lengthy 0% intro period. It’s essential to calculate whether the balance transfer fee is less than the interest you’d accrue on your existing card during the promotional period. Always have a concrete plan to pay off the transferred balance before the introductory APR expires to avoid reverting to a potentially high standard APR.

Cardholder Benefits

Beyond APR, fees, and rewards, many credit cards offer a suite of additional benefits that can provide significant value and convenience. These can include:

- Travel Protections: Trip cancellation/interruption insurance, lost luggage reimbursement, car rental insurance.

- Purchase Protections: Extended warranties, purchase protection (against theft or damage), price protection.

- Digital Security Features: Fraud alerts, virtual card numbers, identity theft protection.

- Concierge Services: Assistance with travel bookings, event tickets, and other requests.

The value of these benefits is highly subjective and depends on your lifestyle and needs. For some, these protections provide peace of mind and tangible savings, making a card with a higher APR or annual fee justifiable. For others, they may go unused. A “good” credit card takes all these factors into account, ensuring that the total package delivers genuine value for your specific financial profile and usage patterns.

Managing Your Credit Cards for Optimal Financial Health

Securing a credit card with a good APR is an excellent start, but it’s only one piece of the puzzle. Effective credit card management is an ongoing process that involves discipline, strategic planning, and regular review to ensure these powerful financial tools work for you, not against you.

The Golden Rule: Pay in Full

The single most effective strategy for managing credit card debt and avoiding interest charges altogether is to pay your statement balance in full by the due date every single month. This practice allows you to leverage the convenience and benefits of your credit card without incurring any interest. By consistently paying in full, the APR of your card becomes irrelevant, as you’re operating within the interest-free grace period. This maximizes your financial efficiency, keeps your credit utilization low, and positively impacts your credit score, making you eligible for even better financial products in the future. Embrace this golden rule, and your credit cards will be powerful allies in your financial journey.

Utilizing Balance Transfers Strategically

Balance transfer cards, particularly those with 0% introductory APRs, can be incredibly valuable tools for debt consolidation and accelerated repayment, but only when used strategically. Before initiating a transfer, evaluate:

- The Balance Transfer Fee: Typically 3-5%, ensure this fee is less than the interest you would save over the promotional period on your current, high-interest card.

- The Introductory Period Length: Is the 0% APR period long enough for you to realistically pay down the transferred balance?

- The Post-Introductory APR: Be aware of the “go-to” rate that will apply once the promotional period ends.

- Your Repayment Plan: Develop a strict budget and an aggressive repayment schedule to ensure you pay off the transferred balance before the 0% APR expires.

Without a solid plan, a balance transfer can simply delay the inevitable, potentially leaving you with a new card and a high APR on the remaining balance. Used wisely, however, it can be a significant step toward becoming debt-free.

Regular Review and Negotiation

Your financial circumstances and the credit card market are constantly evolving, so it’s prudent to regularly review your credit card accounts.

- Check Statements: Scrutinize your monthly statements for errors, unauthorized charges, and a clear understanding of your interest accrual.

- Review APRs Annually: Compare your current credit card APRs against market averages and new offers. If your credit score has improved significantly, or if you’ve been a loyal customer, don’t hesitate to call your card issuer and request a lower APR. Many issuers are willing to negotiate to retain good customers.

- Assess Card Value: Annually evaluate if your current cards still align with your spending habits and financial goals. Are you maximizing rewards? Are you paying an annual fee for benefits you no longer use? This periodic assessment can help you decide whether to downgrade, upgrade, or even close certain accounts.

Avoiding Penalty APRs

Penalty APRs are among the highest rates a credit card issuer can charge, often triggered by a single late payment. They can apply not just to new purchases but to your existing balance as well, potentially remaining in effect for months or even permanently. To avoid this costly pitfall:

- Pay On Time, Every Time: Set up automatic payments, calendar reminders, or both. Timely payments are the bedrock of good credit management.

- Stay Within Your Credit Limit: Exceeding your credit limit can also trigger a penalty APR and incur additional fees.

- Understand Terms and Conditions: Familiarize yourself with your card’s specific penalty triggers and the duration for which a penalty APR might apply.

By being diligent and proactive, you can steer clear of penalty APRs, preserving your financial resources and maintaining a healthy relationship with your credit issuer. Responsible credit card management is not just about finding a “good” APR, but about consistently making choices that support your overall financial well-being.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.